Last Update18 Sep 25Fair value Increased 6.40%

AMG Critical Materials’ consensus price target has been raised to €27.37 as analysts cite strengthened earnings confidence and strategic exposure to critical materials, though higher valuation and a mixed outlook on near-term upside temper further upgrades.

Analyst Commentary

- Bullish analysts highlight AMG's combination of resilient industrial cash flow and exposure to strategic raw materials as key growth drivers.

- Upward price target revisions reflect improved confidence in future earnings and sector momentum.

- Continued Buy ratings are based on the company's positioning within the critical materials supply chain and anticipated long-term demand.

- Bearish analysts point to increased valuation as a reason to temper rating upgrades despite constructive price target adjustments.

- Some analysts shift to a Hold stance as share prices approach or exceed their recent price targets, suggesting limited short-term upside.

Valuation Changes

Summary of Valuation Changes for AMG Critical Materials

- The Consensus Analyst Price Target has risen from €25.72 to €27.37.

- The Consensus Revenue Growth forecasts for AMG Critical Materials has significantly risen from 3.9% per annum to 7.0% per annum.

- The Net Profit Margin for AMG Critical Materials has significantly fallen from 8.46% to 6.93%.

Key Takeaways

- Expanded lithium capacity and new agreements strengthen AMG's regional leadership, supporting revenue stability, margin gains, and greater supply chain resilience.

- Strategic recycling initiatives and geographic diversification increase access to raw materials, positioning AMG for improved profitability and lower cost volatility.

- Continued exposure to commodity price swings, high capital spending, and operational challenges threaten cash flow, limit financial flexibility, and could prolong earnings volatility.

Catalysts

About AMG Critical Materials- Develops, produces, and sells energy storage materials.

- The ramp-up of AMG's expanded lithium production capacities in Brazil and Germany, combined with progress on resolving temporary equipment issues, positions the company to capture rising demand from the EV and energy storage sectors; this is likely to support accelerated revenue and EBITDA growth once full capacity is restored and as pricing recovers.

- The commissioning and demand coverage (contracted utilization) of the Bitterfeld lithium refining facility, as well as new feedstock agreements in Europe, are set to solidify AMG's position as a key regional supplier-likely leading to greater revenue stability and the potential for premium pricing, supporting both top-line growth and margin enhancement.

- Strategic investments in recycling and circular economy initiatives, particularly in vanadium catalyst and battery materials, are increasing AMG's access to critical secondary raw materials and improving supply chain resilience, which should drive higher net margins and reduce input cost volatility relative to competitors.

- AMG's expanding presence in North America and the Middle East (notably through the chrome metal plant in Pennsylvania and joint ventures in Saudi Arabia), aligned with Western government support for domestic critical materials supply chains, could yield long-term volume and pricing upside as national security policies drive contract stability and elevated demand-positively impacting future revenue and EBITDA.

- The recent high profitability in the Antimony segment, underpinned by favorable market conditions, persistent order backlog in AMG Technologies, and anticipated normalization of working capital, suggest that earnings and cash flow are poised for improvement in the medium term as market conditions recover and operational bottlenecks are addressed.

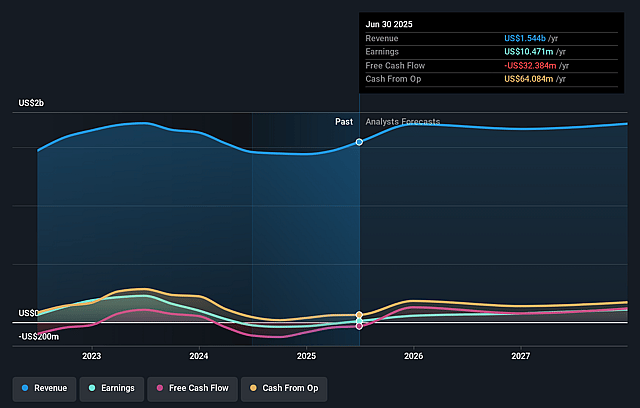

AMG Critical Materials Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AMG Critical Materials's revenue will grow by 3.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.7% today to 8.5% in 3 years time.

- Analysts expect earnings to reach $146.4 million (and earnings per share of $3.15) by about September 2028, up from $10.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 7.5x on those 2028 earnings, down from 99.0x today. This future PE is lower than the current PE for the GB Metals and Mining industry at 9.9x.

- Analysts expect the number of shares outstanding to decline by 1.6% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.88%, as per the Simply Wall St company report.

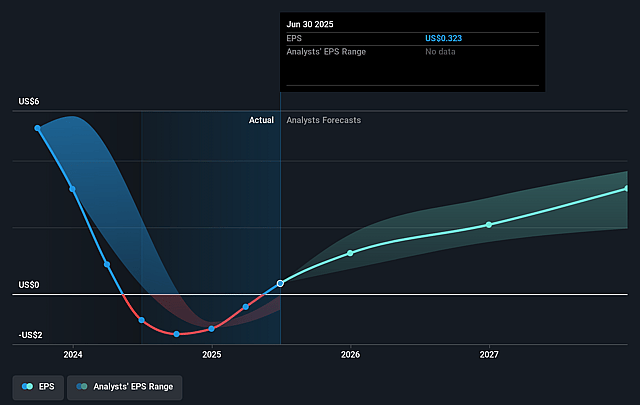

AMG Critical Materials Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistent volatility and price declines in key products such as lithium and vanadium, as evidenced by recent revenue and EBITDA declines in those segments, highlight exposure to commodity cycles and may continue to depress revenue and net income if market prices do not recover sustainably.

- Ongoing high levels of capital expenditure for facility expansions, technological upgrades, and environmental compliance (as noted, $75–100 million expected in 2025) may constrain free cash flow and limit dividend growth or debt reduction, impacting net earnings and financial flexibility.

- Elevated inventories and working capital tied up in raw material bidding (notably vanadium and antimony) have already negatively affected operating cash flow; if market demand or pricing fails to absorb inventories at expected rates, future earnings and cash flow generation may suffer.

- The company's profitability in the AMG Antimony segment this quarter was boosted by a one-off tailwind from low-cost inventory sales at higher market prices-an effect management explicitly described as temporary-raising the risk of lower future segment margins and more volatile earnings once this effect dissipates.

- Operational risks related to ramping new capacity, equipment failures (e.g., the lithium expansion issue in Brazil), and customer qualification processes could prolong underutilization of assets, delay production volume increases, and dampen revenue growth or EBITDA contribution in key new investments over the long-term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €25.72 for AMG Critical Materials based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €32.06, and the most bearish reporting a price target of just €20.22.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.7 billion, earnings will come to $146.4 million, and it would be trading on a PE ratio of 7.5x, assuming you use a discount rate of 6.9%.

- Given the current share price of €27.54, the analyst price target of €25.72 is 7.1% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.