Key Takeaways

- Expanded focus on energy transition and emerging markets aims to capitalize on global demand for cleaner fuels and generate stable, long-term recurring revenues.

- Portfolio optimization, digitalization, and operational efficiency initiatives are expected to drive higher margins, predictable cash flows, and improved returns for shareholders.

- Underutilized assets, weak global markets, project delays, operational incidents, and currency volatility are significant threats to stable revenue and long-term profitability.

Catalysts

About Koninklijke Vopak- An independent tank storage company, stores and handles liquid chemicals, gases, and oil products to the energy and manufacturing markets worldwide.

- Vopak is ramping up investments in infrastructure for new energy carriers-such as LNG, hydrogen, ammonia, and biofuels-supported by €1 billion in equity contributions targeted at the energy transition by 2030; this positions the company to benefit from the global demand shift toward cleaner fuels, likely boosting occupancy rates and driving revenue and margin growth as these projects come online.

- The company's strategic expansions in high-growth markets (India, China, Western Canada) and industrial terminals via JVs are directly tied to industrialization and demographic growth in Asia and other emerging economies, which stands to generate stable, long-term, recurring revenues supported by high utilization and long-term contracts.

- Proactive portfolio optimization through divestment of non-core assets and significant capital reallocation into industrial, gas, and energy transition terminals is expected to improve group ROCE and expand net margins as higher-growth, higher-return assets begin to represent a larger share of earnings.

- Vopak's robust order book of growth projects (e.g. REEF terminal in Canada, ammonia storage in India, biofuels expansion in Malaysia, and the FEED phase for ammonia in Antwerp) directly aligns with rising international trade in chemicals and essential commodities; these capacity additions are likely to support proportional EBITDA growth and enhanced cash flow returns over the coming years.

- Investment in automation, digitalization, and operational efficiency, coupled with a pipeline of long-term customer contracts in resilient sectors (LNG, industrial, new energies), reinforces predictability of cash flows and is poised to further support margin expansion, reduced earnings volatility, and improved long-term shareholder returns.

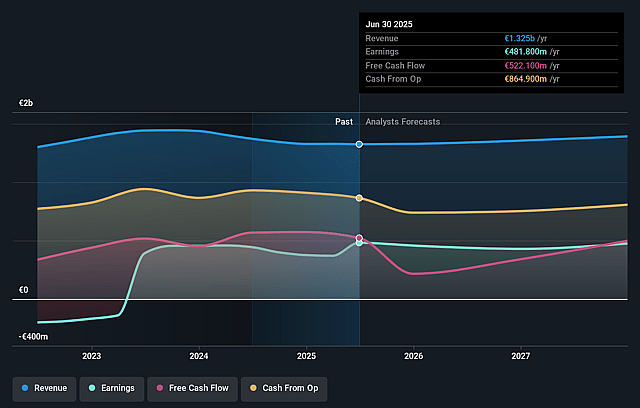

Koninklijke Vopak Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Koninklijke Vopak's revenue will grow by 1.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 36.4% today to 31.9% in 3 years time.

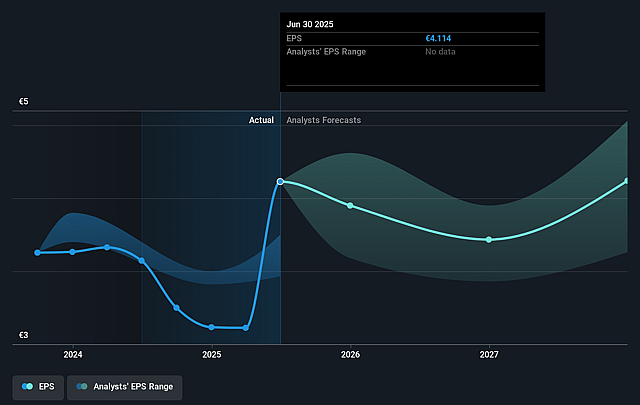

- Analysts expect earnings to reach €447.8 million (and earnings per share of €4.12) by about September 2028, down from €481.8 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as €525 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.0x on those 2028 earnings, up from 9.8x today. This future PE is greater than the current PE for the GB Oil and Gas industry at 9.8x.

- Analysts expect the number of shares outstanding to decline by 3.89% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.79%, as per the Simply Wall St company report.

Koninklijke Vopak Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Vopak's legacy assets in Veracruz are currently underutilized due to the loss of long-term fuel distribution contracts, with minimal contribution expected for the foreseeable future and significant regulatory delays before repurposing can drive new revenues, potentially pressuring overall revenue growth and asset utilization rates.

- Weakness and overcapacity in the global chemicals market, especially in key hub and distribution locations, is already leading to lower occupancy and throughput levels at some terminals, reducing revenue stability and creating long-term risk of margin compression if chemical demand does not recover.

- Delays or uncertainty in final investment decisions (FID) for major energy transition projects (such as ammonia terminals in Antwerp and Japan) could hinder Vopak's ability to timely pivot to new energy carriers; execution risks and permitting requirements may result in lost market share or delayed earnings contribution, negatively impacting long-term top line growth.

- Ongoing environmental, technical, and safety incidents (evidenced by jetty collisions in Belgium and Singapore, and deteriorating personal safety performance) could lead to higher insurance premiums, capex, or regulatory compliance costs, eroding margins and threatening profitability if not better managed.

- High sensitivity to foreign exchange fluctuations-with over 70% of proportional EBITDA generated in non-euro currencies-means persistent currency volatility could offset operational gains, directly impacting reported earnings and net margins even if core business performance remains solid.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €51.75 for Koninklijke Vopak based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €59.0, and the most bearish reporting a price target of just €40.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €1.4 billion, earnings will come to €447.8 million, and it would be trading on a PE ratio of 14.0x, assuming you use a discount rate of 5.8%.

- Given the current share price of €41.08, the analyst price target of €51.75 is 20.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Koninklijke Vopak?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.