Last Update08 Oct 25Fair value Decreased 22%

Fugro's analyst price target has been reduced from €13.00 to €10.08 as analysts express concerns over declining revenue growth and challenges in achieving previously forecast profit margins.

Analyst Commentary

Recent shifts in analyst ratings for Fugro reflect divergent perspectives on the company’s growth prospects, profitability targets, and valuation. While some analysts point to encouraging trends that may drive positive share price momentum, others highlight notable headwinds and risks to execution.

Bullish Takeaways

- Bullish analysts see ongoing sales growth and disciplined cost management as key drivers that can support a continued rerating of the stock.

- They express confidence that operational improvements could pave the way for margin expansion, especially if cost-cutting initiatives yield expected results.

- The recent upgrade notes a higher price target and suggests that upside potential exists if revenue momentum and cost discipline are sustained.

Bearish Takeaways

- Bearish analysts point to lower revenue growth and challenges in reaching prior profit margin forecasts, driving a reduction in price targets.

- Skepticism remains over the optimism embedded in profitability targets for 2025, with concerns that these may be difficult to achieve given current trends.

- The prevailing consensus downgrade reflects tempered expectations around near-term execution and the likelihood that valuation could remain pressured until financial performance stabilizes.

What's in the News

- Fugro downgraded to Underperform from Hold at Jefferies, with a price target lowered to EUR 10 from EUR 12.50. Jefferies considers profitability targets for the second half of 2025 to be "relatively optimistic." (Jefferies)

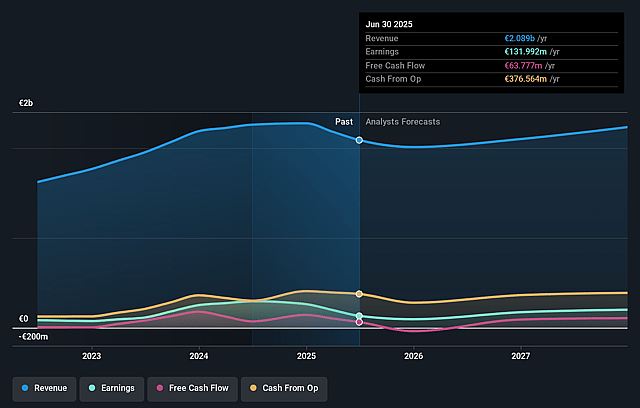

- Fugro has withdrawn its financial guidance for the full year 2025 following significant recent market changes, stating that the previously forecast 20% revenue growth is no longer considered realistic. (Company)

- The company has also withdrawn its EBIT margin guidance for the year, which was previously set at 8% to 11%. Fugro now indicates an expectation of margins below 8%. (Company)

Valuation Changes

- Consensus analyst price target has decreased significantly from €13.00 to €10.08.

- Discount rate has risen slightly, moving from 7.48% to 7.51%.

- Revenue growth assumptions have shifted from a projected increase of 2.6% to a decline of -1.12%.

- Net profit margin forecasts have fallen from 8.63% to 7.40%.

- Future P/E ratio expectations have increased from 8.62x to 9.22x.

Key Takeaways

- Accelerating demand for renewable energy, climate services, and expanded project backlog is driving recurring revenue and improving resilience against sector volatility.

- Adoption of autonomous technologies and disciplined cost controls are set to enhance operational efficiency, drive margin expansion, and support strategic growth flexibility.

- Weakness in renewables, volatile infrastructure demand, heavy investment costs, restructuring risks, and a shift to lower-margin projects threaten Fugro's growth, margins, and earnings stability.

Catalysts

About Fugro- Provides geo-data services for the infrastructure, energy, and water industries in Europe, Africa, the Americas, the Asia Pacific, the Middle East, and India.

- The accelerated build-out of renewable energy and offshore wind globally continues to expand Fugro's long-term addressable market, even as the sector recalibrates in the near term; as projects delayed in H1 are now being mobilized and activity recovers, this is expected to drive higher revenue growth and strengthen order backlog in the coming years.

- Heightened need for coastline monitoring, climate risk mitigation, and subsea infrastructure security (spurred by rising climate risks and regulatory pressures) is establishing recurring, mission-critical project demand for Fugro's geospatial and geotechnical services, supporting both revenue resilience and longer-term earnings visibility.

- Fugro's rapid adoption and rollout of autonomous and remote survey technologies (such as USVs and advanced seabed drills) is poised to structurally improve operational efficiency and vessel utilization rates; this, combined with a comprehensive cost reduction program, should lift net margins and boost earnings as asset downtime decreases and more high-value, lower-cost services are delivered.

- Ongoing expansion and diversification of the order backlog-with a shift from volatile wind to include large, multi-year projects in oil & gas, infrastructure, and defense-reduces revenue cyclicality and provides enhanced earnings predictability, supporting a quicker recovery from recent revenue shortfalls.

- A disciplined capital expenditure program, vessel investment now largely complete, and ongoing balance sheet strengthening position Fugro to capitalize on industry upturns and pursue strategic growth opportunities without overleveraging; this improved financial flexibility is a catalyst for future net earnings expansion as markets recover.

Fugro Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Fugro's revenue will grow by 2.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.3% today to 8.7% in 3 years time.

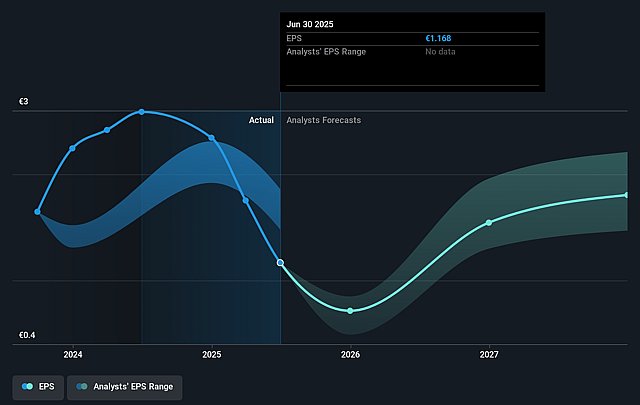

- Analysts expect earnings to reach €198.1 million (and earnings per share of €1.79) by about September 2028, up from €132.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €241.1 million in earnings, and the most bearish expecting €136 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 8.9x on those 2028 earnings, down from 9.6x today. This future PE is lower than the current PE for the GB Construction industry at 13.4x.

- Analysts expect the number of shares outstanding to decline by 1.79% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.27%, as per the Simply Wall St company report.

Fugro Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Prolonged weakness and recalibration in the offshore wind market, with significant drops in renewables backlog and ongoing uncertainties from changing regulations, high interest rates, and grid connection complexities in key regions like Europe and the U.S., continue to reduce revenue visibility and growth prospects in one of Fugro's largest addressable markets.

- Persistent macroeconomic instability, high inflation, and slow infrastructure activity across regions (notably the Middle East, Hong Kong, and Europe-Africa), combined with seasonality, are already causing delays and scope reductions in both land and marine revenues, making earnings and future revenue streams more volatile.

- Heavy capital expenditures on vessel conversion and USV fleet expansion, following a front-loaded capex profile and rising net debt (from €96 million to €437 million), introduce financial risk-especially as returns from these investments depend on winning projects in increasingly competitive, and sometimes shrinking, markets, placing future net margins and free cash flow under pressure.

- Fugro's ongoing cost reduction program, including significant global layoffs (750 FTE) and renegotiations with suppliers, underscores structural cost and operational challenges, and while intended to stabilize margins, it risks negatively impacting execution capability, increasing restructuring charges, and limiting growth capacity during any market upturns.

- The replacement of higher-margin long-term wind contracts with a larger number of shorter-duration oil & gas and infrastructure projects increases risk, given the cyclical nature of oil & gas-and with limited near-term evidence of recovery in wind or sustained infrastructure growth, this shift may put pressure on margins and expose the company to sectoral downturns, reducing overall earnings resilience.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €13.667 for Fugro based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €15.0, and the most bearish reporting a price target of just €10.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €2.3 billion, earnings will come to €198.1 million, and it would be trading on a PE ratio of 8.9x, assuming you use a discount rate of 7.3%.

- Given the current share price of €11.49, the analyst price target of €13.67 is 15.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.