Key Takeaways

- Strategic investments in green-fuel fleets, digital transformation, and infrastructure are positioning the company for structurally higher margins and sustained net income outperformance.

- Industry consolidation and rising entry barriers are enhancing the company's pricing power and earnings resilience beyond current analyst expectations.

- Rising regulatory pressure, volatile markets, aging fleet costs, and global trade shifts threaten profitability, revenue stability, and long-term competitiveness for Mitsui O.S.K. Lines.

Catalysts

About Mitsui O.S.K. Lines- Engages in the marine transportation business worldwide.

- Analyst consensus broadly expects stable revenue from MOL's exposure to emerging markets and global trade, but this actually understates the company's long-term growth: as supply chain diversification accelerates and manufacturing continues shifting to Southeast Asia and beyond, MOL's diversified multi-modal fleet stands to benefit disproportionately through higher volume growth and asset utilization, likely increasing both revenue and operating leverage above current forecasts.

- Analyst consensus sees decarbonization as a chance for incremental profitability through regulatory compliance and some premium rates, while the reality is that MOL's early leadership in green-fuel vessels and LNG shipping positions it to capture structural market share and secure premium, long-dated contracts well ahead of peers, which will materially boost net margins and annuity-like earnings stability.

- The company's ongoing portfolio shift-via recent acquisitions and expansion into high-return energy infrastructure, wind, and terminals-creates a more resilient earnings base and opens avenues for recurring, higher-margin cash flows, which are not yet fully reflected in projected valuation or earnings multiples.

- Advancements in digital transformation, automation, and AI-powered logistics within MOL's operations are poised to meaningfully reduce cost per unit shipped, providing a structural uplift to operating margins and potentially supporting sustainable outperformance on net income versus traditional shipping peers.

- The industry's rising barriers to entry and capital intensity, coupled with consolidation tailwinds, will allow well-capitalized incumbents like MOL to exert increased pricing power and secure utilization, supporting both top line growth and further dividend enhancement.

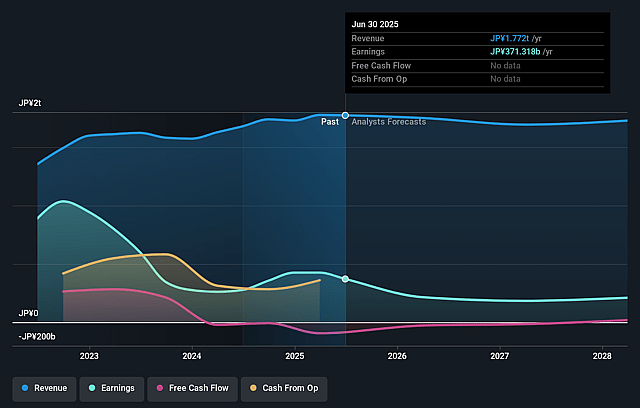

Mitsui O.S.K. Lines Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Mitsui O.S.K. Lines compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Mitsui O.S.K. Lines's revenue will grow by 1.7% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 21.0% today to 13.4% in 3 years time.

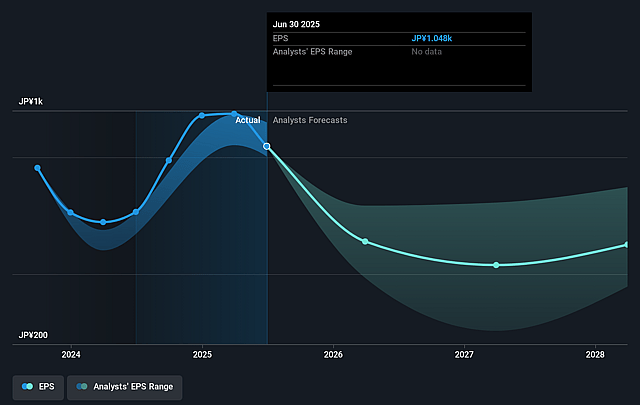

- The bullish analysts expect earnings to reach ¥248.9 billion (and earnings per share of ¥755.61) by about September 2028, down from ¥371.3 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 10.3x on those 2028 earnings, up from 4.5x today. This future PE is greater than the current PE for the JP Shipping industry at 6.9x.

- Analysts expect the number of shares outstanding to decline by 4.7% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.71%, as per the Simply Wall St company report.

Mitsui O.S.K. Lines Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Mitsui O.S.K. Lines faces persistent headwinds from decarbonization and tightening emissions regulations, which will require significant investment in cleaner ships and alternative fuels, driving up both operating and capital expenditures and ultimately pressuring net earnings over the long term.

- The company's heavy reliance on cyclical and volatile shipping segments, especially dry bulk and container shipping, exposes it to unpredictable swings in freight rates and demand

- as already evidenced by substantial year-on-year profit declines in these areas

- creating sustained risks to both revenue stability and net margins.

- The ongoing shift in global manufacturing patterns and the rise of nearshoring, together with the company's Asia-centric shipping routes, threatens long-term core volumes and could reduce future revenues as global trade flows recalibrate away from East Asia.

- A high proportion of aging vessels, coupled with the need for major retrofits or replacements to comply with future regulations and remain competitive, will require substantial ongoing capital expenditures that may constrain free cash flow and elevate depreciation charges, ultimately weighing on net earnings.

- Industry-wide vessel oversupply, automation-driven pricing pressure, and the rise of mega-carriers are all likely to erode profitability, compressing Mitsui O.S.K. Lines' margins and threatening its ability to maintain pricing power and healthy returns on equity in the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Mitsui O.S.K. Lines is ¥6941.11, which represents two standard deviations above the consensus price target of ¥5510.91. This valuation is based on what can be assumed as the expectations of Mitsui O.S.K. Lines's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥7000.0, and the most bearish reporting a price target of just ¥3920.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be ¥1864.1 billion, earnings will come to ¥248.9 billion, and it would be trading on a PE ratio of 10.3x, assuming you use a discount rate of 7.7%.

- Given the current share price of ¥4878.0, the bullish analyst price target of ¥6941.11 is 29.7% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.