Key Takeaways

- Global regulatory pressures, green chemistry trends, and intense Asian competition threaten export growth, pricing power, and margins for traditional specialty chemicals.

- Heavy dependence on a handful of key customers and volatile input costs amplify earnings risks and undermine the stability of long-term profit levels.

- Strong international client relationships, supply chain advantages, and expansion into higher-value segments position the company for sustained growth, improved margins, and earnings visibility.

Catalysts

About Anupam Rasayan India- Engages in the custom synthesis and manufacturing of specialty chemicals in India, Europe, Japan, Singapore, China, North America, and internationally.

- The increasing global regulatory scrutiny and threat of trade barriers on chemical exports, as highlighted by new 25% US tariffs, could meaningfully restrict Anupam Rasayan's future export growth and introduce cost inefficiencies, putting top-line revenue at risk even though current exposure to these tariffs is limited.

- Persistent global momentum towards green chemistry and sustainable alternatives may structurally weaken demand for traditional specialty molecules in agrochemicals and polymers, directly undermining long-term revenue growth and eroding the pricing power that supports current margins.

- With 79% of revenue derived from just the top ten customers, any move by a key client to diversify suppliers or pursue backward integration could significantly reduce revenue visibility and sharply increase earnings volatility, given such heavy customer concentration.

- Ongoing volatility in raw material and feedstock costs, especially amid supply chain disruptions and crude oil fluctuations, is likely to continue compressing margins for the specialty chemicals sector, obstructing Anupam Rasayan's ability to sustain recent profit levels even with targeted working capital improvements.

- Heightened competition from Chinese and Asian peers with greater economies of scale and lower production costs may trigger industry-wide price pressure, leaving Anupam Rasayan exposed to declining net margins and compromised return on capital-especially as secular demand trends shift towards more sustainable chemistry and bio-based alternatives.

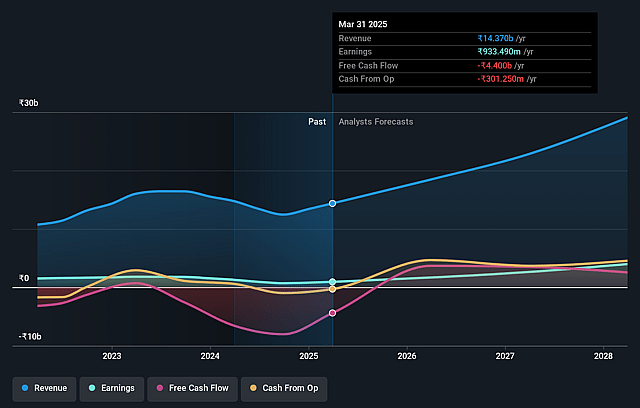

Anupam Rasayan India Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Anupam Rasayan India compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Anupam Rasayan India's revenue will grow by 12.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 7.4% today to 10.9% in 3 years time.

- The bearish analysts expect earnings to reach ₹2.6 billion (and earnings per share of ₹23.82) by about September 2028, up from ₹1.2 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 32.4x on those 2028 earnings, down from 102.0x today. This future PE is greater than the current PE for the IN Chemicals industry at 26.8x.

- Analysts expect the number of shares outstanding to decline by 0.56% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.76%, as per the Simply Wall St company report.

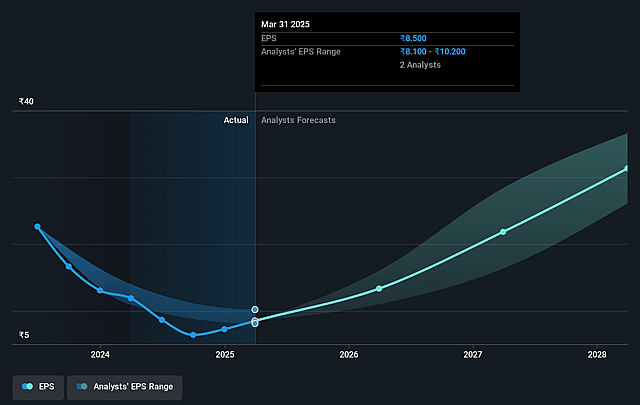

Anupam Rasayan India Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The robust year-on-year revenue growth of 89 percent, driven by both existing and new segments like Pharma and Performance Materials, suggests strong secular demand tailwinds and positions Anupam Rasayan to expand top-line growth over the long term.

- Anupam Rasayan has deepened its client relationships with significant long-term contracts, such as the master purchase agreement with a major Japanese conglomerate and new agreements with US

- and Europe-based multinationals, ensuring strong revenue visibility and reducing earnings volatility for future years.

- The company is capitalizing on the global shift in chemical supply chains, with exports making up 58 percent of revenue and a growing order book, allowing it to benefit from the China plus one trend and India's rising role as a preferred specialty chemical exporter, which will likely support sustained revenue growth and margin resilience.

- Capacity expansion and efficient working capital management, including a reduction in net working capital days and being net term-debt-free, provide a solid foundation for margin improvement, scalable operations, and a stronger balance sheet, which bodes well for future earnings and profitability.

- Growth in the company's high-value segments-such as custom synthesis, advanced polymers, and ramp-up in new molecules for the pharma segment-enhances operating leverage and net profit margins, with incremental margin guidance maintained at 25 to 27 percent, indicating the potential for rising net margins and return on capital employed in the medium to long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Anupam Rasayan India is ₹520.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Anupam Rasayan India's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹1305.0, and the most bearish reporting a price target of just ₹520.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ₹24.0 billion, earnings will come to ₹2.6 billion, and it would be trading on a PE ratio of 32.4x, assuming you use a discount rate of 13.8%.

- Given the current share price of ₹1105.8, the bearish analyst price target of ₹520.0 is 112.7% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.