Catalysts

About Microlise Group

Microlise Group provides Software as a Service and related hardware and services that help transport and logistics customers run fleets more efficiently.

What are the underlying business or industry changes driving this perspective?

- Although the push for efficiency in transport and logistics supports demand for Microlise’s fleet performance and planning tools, delays in large customer rollouts due to cyber incidents at clients can hold back the conversion of contracted work into recognised recurring revenue and services income.

- While tighter integration with third party telematics, handhelds and cameras reduces barriers to adoption and should tilt mix toward higher margin software, a slowdown or pause in hardware refresh cycles at customers could restrain total revenue growth and limit the pace of gross margin improvement.

- Although international localisation work in Australia and France, including support for TCA, EWD and eCMR, broadens Microlise’s addressable markets, ongoing skills shortages and the need for additional in-country engineering resource may keep operating expenses elevated and temper any uplift in net margins.

- While ongoing AI and machine learning features that use Microlise’s large data sets can deepen product usage, heavy and recurring investment in internally generated software and hosting infrastructure, including delayed data centre projects, may weigh on free cash flow and earnings if customers adopt new modules more slowly than expected.

- Although consolidation among large logistics operators such as DHL and Evri can increase the scale of existing customers and create wider upsell opportunities, flat volume expectations from major OEM clients and project delays linked to wider automotive sector disruption could limit growth in OEM related revenue and EBITDA.

Assumptions

This narrative explores a more pessimistic perspective on Microlise Group compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

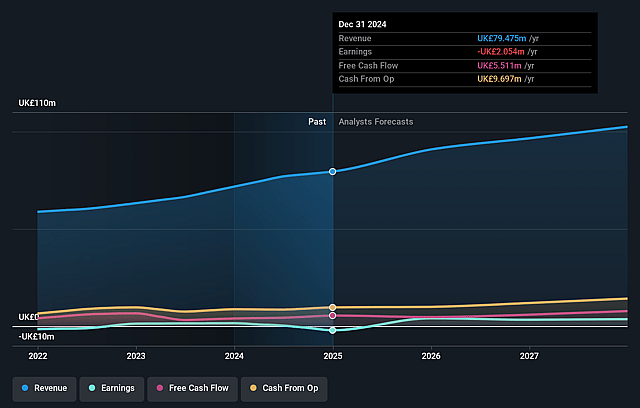

- The bearish analysts are assuming Microlise Group's revenue will grow by 4.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -0.9% today to 4.4% in 3 years time.

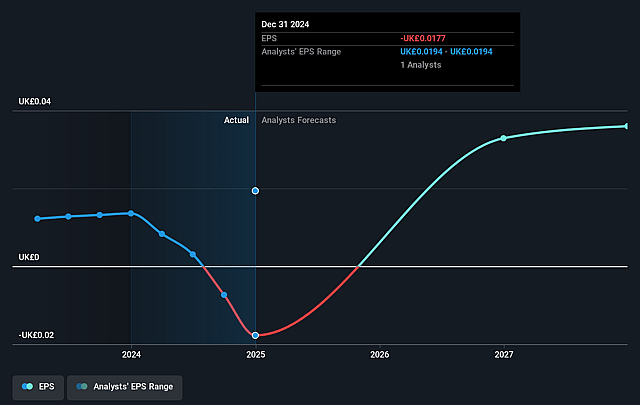

- The bearish analysts expect earnings to reach £4.2 million (and earnings per share of £0.03) by about January 2029, up from £-787.0 thousand today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as £5.6 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 42.8x on those 2029 earnings, up from -140.7x today. This future PE is greater than the current PE for the GB Software industry at 33.2x.

- The bearish analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.75%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Customer projects can be delayed for reasons outside Microlise Group's control, such as cyber incidents at large clients and disruption at automotive customers like M&S or JLR. This could slow the conversion of the order book into recognised revenue and keep earnings growth below your expectations.

- Growth in high volume OEM channels is currently expected to be flat and there is a stated shift in focus toward mid market and direct customers. If this mix change does not offset softer OEM volumes, total revenue and recurring revenue could both fall short of what a rising share price would typically need.

- Ongoing investment in cybersecurity, hosting, internal software development, business systems and international engineering teams, together with skills shortages and higher employment and IT costs, could keep operating expenses high and limit any improvement in EBITDA margin and net margins.

- The international growth and M&A plan depends on successfully integrating new products and geographies while avoiding loss making acquisitions. If suitable targets are limited or integrations are slower or more expensive than planned, this could restrict long term expansion of recurring revenue and earnings.

- Delays in data centre projects due to IT hardware lead times, as well as reliance on third party hardware supply and partner integrations, could slow the planned hosting cost savings and hardware margin gains. This may hold back improvements in gross margin and free cash flow.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Microlise Group is £1.2, which represents up to two standard deviations below the consensus price target of £1.51. This valuation is based on what can be assumed as the expectations of Microlise Group's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £1.91, and the most bearish reporting a price target of just £1.2.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be £95.7 million, earnings will come to £4.2 million, and it would be trading on a PE ratio of 42.8x, assuming you use a discount rate of 8.8%.

- Given the current share price of £0.95, the analyst price target of £1.2 is 20.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Microlise Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.