Key Takeaways

- Strength in accelerated drug approvals and strong global uptake is set to expand revenue faster than forecasts, reinforced by proprietary platform and clinical advances.

- Increased commercialization, strategic flexibility, and demographic trends in core markets position the company for sustained sales growth and improved profitability.

- Rising competition, regulatory hurdles, and geopolitical risks threaten HUTCHMED's profitability, with dependence on a narrow drug pipeline heightening vulnerability to setbacks and shareholder dilution.

Catalysts

About HUTCHMED (China)- HUTCHMED (China) Limited, together with its subsidiaries, discovers, develops, and commercializes targeted therapeutics and immunotherapies to treat cancer and immunological diseases in Hong Kong, the United States, and internationally.

- While analyst consensus expects incremental growth from new indications and NDA submissions, the late-stage pipeline is advancing faster than anticipated and early robust clinical data suggest savolitinib and fruquintinib could see significantly accelerated multi-indication approvals, dramatically enlarging the revenue base beyond current projections.

- Analysts broadly agree that FRUZAQLA's global expansion will support top-line growth, but recent sales outperformance-particularly in Japan and early traction with international reimbursement-signals uptake could rapidly surpass forecasts, delivering outsized revenue and gross profit acceleration as global launches compound.

- HUTCHMED's proprietary ATTC platform is attracting global interest and, with IND submissions and clinical entry imminent, the company is well-positioned to become a first mover in a new therapeutic class, potentially enabling high-value licensing deals or partnerships and boosting non-dilutive income and net margins.

- Growing demand for innovative oncology therapeutics driven by an aging population and rising middle-class wealth, especially in China and other emerging markets, is likely to fuel sustained long-term sales growth and market share gains for HUTCHMED's broad pipeline, providing durable, above-industry-average revenue expansion.

- The company's strategic shift to a more commercial-stage profile, bolstered by a substantial $1.3 billion+ cash reserve and operational focus post-sales team transition, unlocks flexibility to execute opportunistic M&A or in-licensing, accelerating pipeline depth and enhancing future operating leverage, which supports strong multi-year earnings growth.

HUTCHMED (China) Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on HUTCHMED (China) compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

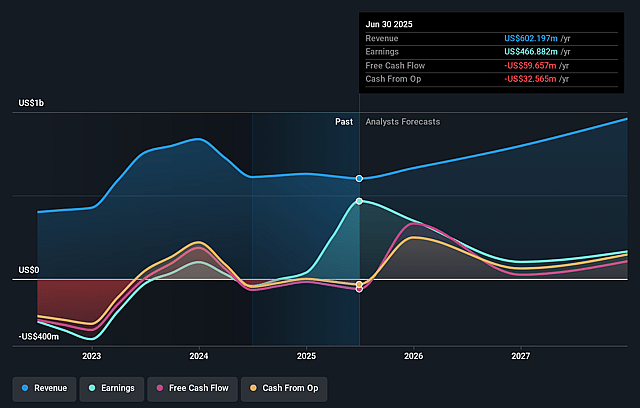

- The bullish analysts are assuming HUTCHMED (China)'s revenue will grow by 24.4% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 77.5% today to 9.6% in 3 years time.

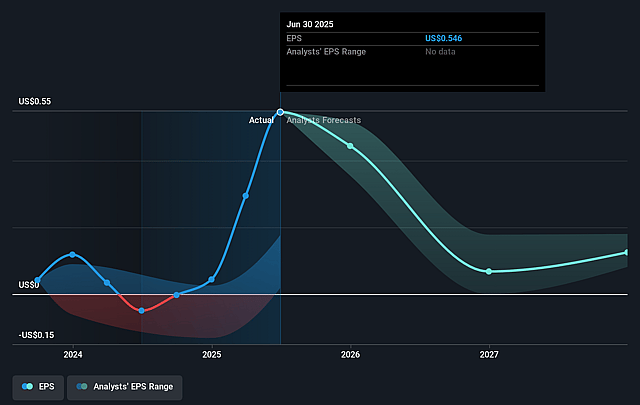

- The bullish analysts expect earnings to reach $111.3 million (and earnings per share of $0.1) by about September 2028, down from $466.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 71.3x on those 2028 earnings, up from 5.8x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 22.3x.

- Analysts expect the number of shares outstanding to grow by 0.52% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.82%, as per the Simply Wall St company report.

HUTCHMED (China) Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces increasing competition in China from generics and new market entrants, especially in colorectal cancer and the MET TKI space, which is putting pressure on market share and will likely impact revenues and net margins negatively in the long term.

- HUTCHMED remains highly dependent on the success of a relatively narrow pipeline, particularly fruquintinib and savolitinib, making the company vulnerable to clinical or commercial setbacks in these key products, which would directly affect revenue growth and could lead to R&D write-offs impacting future earnings.

- Stricter regulatory environments, both in China (such as the NRDL renegotiation and anti-corruption campaigns causing practice changes) and globally (with increased requirements for clinical data and real-world evidence), are leading to disrupted commercialization and higher compliance costs, which can delay approvals and put downward pressure on earnings.

- Rising geopolitical tensions and the potential for increased tariffs or export restrictions, especially on China-manufactured drugs, could limit HUTCHMED's ability to expand internationally and will likely result in higher costs or restricted revenue growth outside China, thereby capping long-term profitability and net margins.

- The ongoing need for substantial R&D and commercialization investment is resulting in periods of negative operating cash flow, and with declining or uncertain sales growth, future fundraising may dilute current shareholders and suppress growth in earnings per share and overall shareholder value.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for HUTCHMED (China) is £5.5, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of HUTCHMED (China)'s future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £5.5, and the most bearish reporting a price target of just £2.05.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $1.2 billion, earnings will come to $111.3 million, and it would be trading on a PE ratio of 71.3x, assuming you use a discount rate of 6.8%.

- Given the current share price of £2.31, the bullish analyst price target of £5.5 is 58.0% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on HUTCHMED (China)?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.