Last Update 15 Jul 26

Fair value Decreased 2.24%GLEN: Copper Mix And Lithium Offtake Will Support Future Rerating Potential

Glencore's analyst price target has been lowered to around £5.90 to £6.35 per share from prior levels closer to £6.10 to £6.60, as analysts factor in higher required returns, updated views on commodity mix and earnings potential, and a moderation in assumed future P/E multiples, despite slightly stronger revenue growth and margin inputs.

Analyst Commentary

Recent research on Glencore shows a mix of optimism and caution, with several bullish analysts still highlighting upside potential around earnings power, commodity exposure and current valuation, even as headline price targets edge lower in some cases.

On the positive side, a number of large firms continue to see Glencore as well positioned within global miners, pointing to factors such as copper exposure, earnings optionality and current P/E assumptions that they view as supportive of the stock over their investment horizon.

At the same time, there is also a more neutral or reserved camp, where analysts are trimming targets or stepping back from prior Buy calls, often citing shifts in commodity leadership, changing risk premia and a more measured stance on future multiples.

Taken together, the latest moves suggest investors are weighing Glencore against both company specific drivers and broader sector themes, with upside cases still present but more tightly framed around valuation discipline and execution on the commodity mix.

Bullish Takeaways

- Bullish analysts continue to attach Buy or Overweight ratings to Glencore alongside price targets around 590 GBp to 635 GBp, indicating they see room for upside relative to current levels based on their assessment of earnings potential and P/E support.

- Goldman Sachs upgraded Glencore to Buy and set a price target of 630 GBp, highlighting what it views as an attractive mix of commodity leverage, earnings upside and valuation support, which together frame a constructive risk reward profile.

- Some large banks, including Deutsche Bank and Barclays, recently set or reaffirmed price targets in the 610 GBp to 635 GBp range, which reflects confidence in Glencore's ability to execute against its commodity portfolio and translate that into cash flow and earnings.

- Across the bullish camp, the common thread is that current valuation multiples are seen as leaving headroom if Glencore can deliver on its earnings and margin assumptions embedded in these research models.

What’s in the News for Glencore

- T5 Smackover Partners signed a binding offtake agreement with Glencore Ltd. for 100% of Phase 1 lithium carbonate production from its East Texas operations, estimated at about 5,000 metric tons per year over 5 years, supporting U.S. domestic lithium supply chain development. (Source: T5 Smackover Partners client announcement)

- At its AGM on 28 May 2026, Glencore plc shareholders approved the reappointment of Deloitte LLP as the company’s auditor. (Source: Glencore AGM client announcement)

- Glencore plc announced a special dividend of US$0.035 per share, with an effective date of 7 May 2026. (Source: Glencore corporate action announcement)

- Glencore reaffirmed its 2026 production guidance, including copper of 810 kt to 870 kt, zinc of 700 kt to 740 kt, nickel of 70 kt to 80 kt, steelmaking coal of 30 mt to 34 mt, and energy coal of 95 mt to 100 mt. (Source: Glencore corporate guidance)

- Glencore reported first quarter 2026 production results, including copper of 199.6 kt, cobalt of 5.8 kt, zinc of 176.9 kt, lead of 41.2 kt, nickel of 17.2 kt, gold of 68 koz, silver of 4,869 koz, chrome ore of 830 kt, steelmaking coal of 6.5 mt, energy coal of 22.9 mt, and ferrochrome of 13 kt. (Source: Glencore operating results announcement)

Valuation Changes for Glencore

- Fair Value: reduced from £7.82 to £7.65, a small reduction of about 2.2% in the modelled estimate.

- Discount Rate: increased from 9.52% to 9.59%, a slight rise of around 0.7% that raises the required return in the valuation work.

- Revenue Growth: increased from 8.57% to 10.62%, a higher assumed growth rate of roughly 2.0 percentage points in future revenue forecasts.

- Net Profit Margin: increased from 2.83% to 3.46%, reflecting a modest uplift of about 0.6 percentage points in projected profitability.

- Future P/E: reduced from 17.00x to 13.14x, a sizeable reduction of close to 22.7% in the assumed earnings multiple applied to Glencore.

Catalysts

About Glencore

Glencore is a diversified natural resources group that produces and markets metals, energy products and related commodities worldwide.

What are the underlying business or industry changes driving this perspective?

- Significant second half copper production uplift, underpinned by ore access and mine sequencing rather than selective mining, positions the copper division to move toward a 1 million tonne profile by 2028. This supports higher EBITDA and cash flow from improved volumes and unit costs.

- Large scale, long life Argentinian copper growth options at MARA and El Pachon, combined with supportive policy initiatives such as RIGI, provide a pathway to roughly 1 million tonnes of additional copper equivalent capacity over time. This may materially enhance future revenue and earnings visibility.

- The marketing range has been reset higher to 2.3 billion to 3.5 billion dollars, driven by structurally tighter copper and zinc markets and increasing trade dislocations from tariffs. This signals a sustained uplift in higher return marketing EBIT and more resilient group margins.

- EVR’s multi decade, low cost Tier 1 steelmaking coal position, together with emerging supply discipline and rationalisation in China and the United States, may enhance pricing power and portfolio mix. This could lift met coal margins and support stronger industrial EBITDA through the cycle.

- Roughly 1 billion dollars of recurring annualised cost savings, heavily weighted to core copper, coal and zinc nickel assets, is expected to more than offset inflation and embed structurally lower operating costs. This may support higher net margins and incremental free cash flow from 2026 onward.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Glencore compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Glencore's revenue will grow by 10.6% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 0.1% today to 3.5% in 3 years time.

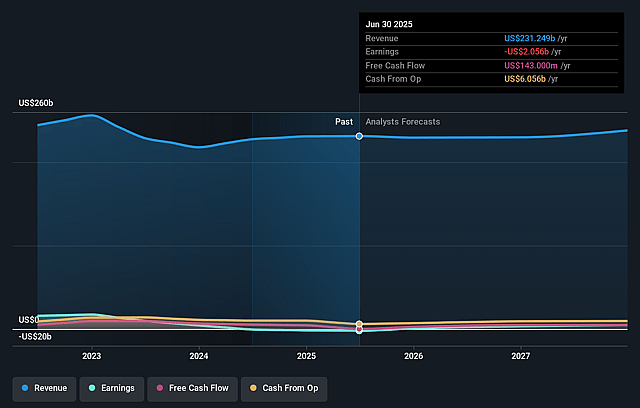

- The bullish analysts expect earnings to reach $11.6 billion (and earnings per share of $0.99) by about July 2029, up from $363.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $4.6 billion.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 13.1x on those 2029 earnings, down from 226.1x today. This future PE is lower than the current PE for the GB Metals and Mining industry at 15.5x.

- The bullish analysts expect the number of shares outstanding to decline by 1.57% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.59%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Glencore’s earnings remain heavily exposed to volatile coal and steelmaking coal markets, and while management expects recent price weakness to reverse, prolonged oversupply or structurally lower demand from decarbonisation and Chinese steel export normalization could keep benchmark prices and quality premia depressed, limiting any recovery in revenue and constraining industrial EBITDA growth.

- The bullish case depends on a sharp second half copper volume uplift and a path back to 1 million tonnes by 2028. This requires flawless execution on mine sequencing, geotechnical remediation and land access at assets like KCC, Collahuasi and Antamina. Any delay, operational setback or inability to sustain nameplate throughput would undermine copper volumes, push up unit costs and cap the anticipated margin expansion and earnings growth.

- A key pillar of the narrative is roughly $1 billion of recurring cost savings by 2026, but these gains may be eroded over time by inflation in energy, consumables, contractors and royalties or by the need to reinstate resources if reliability suffers. This would blunt the intended structural reduction in operating costs and limit improvements in net margins and free cash flow.

- Long dated copper growth options in Argentina and Peru, such as MARA, El Pachon and Coroccohuayco, rely on favourable fiscal regimes, successful RIGI approvals and supportive commodity prices. Political risk, permitting delays or weaker long term copper demand could defer final investment decisions and lower project returns, reducing the future production base that underpins the higher revenue and earnings assumed for the late 2020s.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Glencore is £7.65, which represents up to two standard deviations above the consensus price target of £6.22. This valuation is based on what can be assumed as the expectations of Glencore's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £7.65, and the most bearish reporting a price target of just £4.79.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $335.1 billion, earnings will come to $11.6 billion, and it would be trading on a PE ratio of 13.1x, assuming you use a discount rate of 9.6%.

- Given the current share price of £5.17, the analyst price target of £7.65 is 32.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Glencore?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.