Key Takeaways

- Strategic mining and exploration developments, including new methods and investments, aim to optimize revenue, extend mine life, and diversify resource streams.

- Operational efficiency through solar power and resource acquisitions enhances stability, potentially boosting earnings and improving net margins.

- Transitioning challenges, exploration risks, declining production, currency impacts, and aggressive M&A strategies threaten Central Asia Metals' production, revenues, and financial stability.

Catalysts

About Central Asia Metals- Operates as a base metals producer.

- The transition to more selective mining methods at Sasa, including cut and fill and long-holed stoping, along with the introduction of paste backfill, aims to extend the mine life to 2039 and improve ore recovery, potentially increasing future revenue and stabilizing net margins.

- Exploration opportunities through CAML X in Kazakhstan and investment in Aberdeen Minerals are opening possibilities for new copper and nickel resources, potentially impacting future earnings by providing new revenue streams.

- The continuation of operations beyond 2025 at the Kounrad copper leach facility due to outperforming leach curves provides a stable basis for future revenue, potentially delaying the anticipated production decline.

- The strategic focus on acquiring new cash-flowing assets or overlooked development projects with existing resources can enhance earnings significantly if acquisitions are accretive and add to the company's EBITDA.

- The operation of the solar power plant at Kounrad, supplying 14% of the power at lower costs than grid electricity, supports cost efficiencies that can positively affect net margins over time.

Central Asia Metals Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Central Asia Metals's revenue will decrease by 0.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 23.8% today to 21.0% in 3 years time.

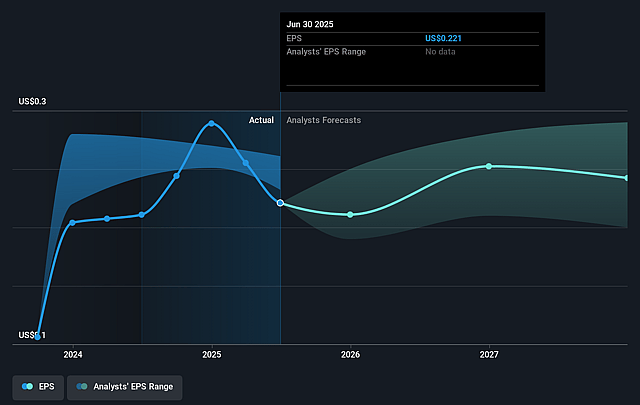

- Analysts expect earnings to reach $45.6 million (and earnings per share of $0.25) by about September 2028, down from $51.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $53.3 million in earnings, and the most bearish expecting $38 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.5x on those 2028 earnings, up from 8.0x today. This future PE is greater than the current PE for the GB Metals and Mining industry at 11.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.38%, as per the Simply Wall St company report.

Central Asia Metals Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The disruption and challenges associated with transitioning to new mining methods at Sasa, such as cut and fill and long-holed stoping, have already resulted in slightly missing production targets, which may continue to pressure production volumes and thus adversely impact revenues.

- The company’s reliance on ongoing exploration and the uncertain success of future discoveries, particularly in the context of their early-stage projects in Kazakhstan and Aberdeen, presents a risk of insufficient future resource base development that could affect long-term revenue and growth prospects.

- The potential for future production tailing off at Kounrad due to maturing copper dumps presents a risk to maintaining current production levels and could impact revenues unless new resources are developed or existing resources are extended successfully.

- Foreign exchange fluctuations and the weakening of the U.S. dollar against local currencies and the pound can increase administrative costs and dividend disbursement expenses, potentially affecting net margins and earnings negatively.

- The significant focus on merger and acquisition activities, with the potential for high leverage or cash outlays, might not yield timely or successful outcomes, potentially impacting cash reserves or leading to financial strain without the assurance of accretive earnings contributions.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £1.964 for Central Asia Metals based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £2.17, and the most bearish reporting a price target of just £1.78.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $217.2 million, earnings will come to $45.6 million, and it would be trading on a PE ratio of 12.5x, assuming you use a discount rate of 7.4%.

- Given the current share price of £1.75, the analyst price target of £1.96 is 10.9% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Central Asia Metals?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.