Key Takeaways

- Structural reliance on legacy policies and demographic headwinds threaten sustained revenue growth, as new business is insufficient to offset the decline in mature markets.

- Rising costs from financial leverage, digital disruption, and regulatory compliance pressure margins, constraining investment capacity and long-term profitability.

- Structural market trends, strategic business pivots, and successful integrations are driving sustainable profit growth, stronger cash flows, and long-term revenue resilience for Phoenix.

Catalysts

About Phoenix Group Holdings- Operates in the long-term savings and retirement business in Europe.

- Persistently low or declining interest rates, combined with a shrinking working-age population in core UK and European markets, threaten the long-term profitability and growth potential of Phoenix Group's retirement and pension products, reducing investment returns on assets and leading to slower growth in new policyholders and top-line revenues.

- Heavy reliance on closed books and legacy business means that, even with recent efforts to grow the open book, Phoenix faces a structural long-term run-off in revenues as older policies mature and lapse, while new business growth is unlikely to fully offset this decline, putting sustained pressure on recurring fee income and earnings growth beyond the next few years.

- High financial leverage-currently at 36% on a regulatory basis and materially higher on a pure shareholder basis-amplifies downside risk, especially if rising credit spreads or refinancing costs emerge, threatening to erode net margins and constrain Phoenix's ability to invest in future business expansion or support its progressive dividend policy.

- The increasing pace of digital disruption and the entrance of fintech and insurtech rivals risk undermining Phoenix Group's ability to acquire and retain customers, while driving up required technology investments and compressing operating margins over time as traditional providers lose market share to more agile digital-first competitors.

- Escalating climate change legislation and ESG-related compliance demands will continue to add significant ongoing costs and require material shifts in investment portfolios, creating potential headwinds for capital generation, depressing long-term returns, and undermining Phoenix's ability to maintain current levels of operating profit and dividend growth.

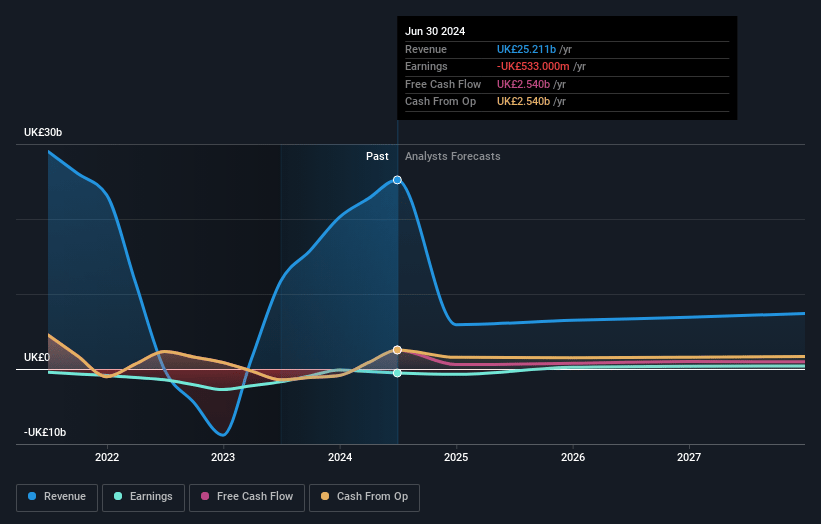

Phoenix Group Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Phoenix Group Holdings compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Phoenix Group Holdings's revenue will decrease by 36.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -5.2% today to 14.2% in 3 years time.

- The bearish analysts expect earnings to reach £789.5 million (and earnings per share of £0.53) by about July 2028, up from £-1.1 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 8.7x on those 2028 earnings, up from -5.8x today. This future PE is lower than the current PE for the GB Insurance industry at 13.1x.

- Analysts expect the number of shares outstanding to decline by 0.27% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.85%, as per the Simply Wall St company report.

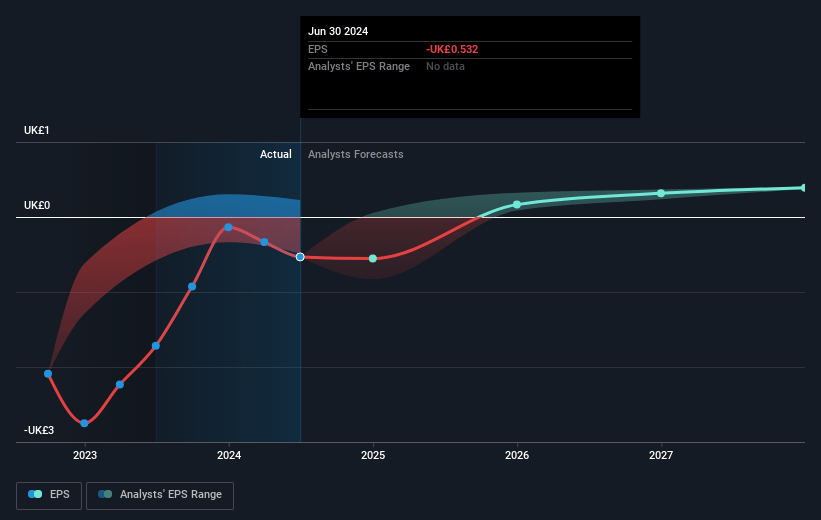

Phoenix Group Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The UK and European ageing population trends, along with a growing focus on retirement products, are rapidly expanding Phoenix's addressable market, which underpins recurring revenue growth, supports strong net inflows, and provides structural tailwinds that may propel long-term revenues and earnings higher.

- Phoenix has executed a significant operational pivot into growth markets like workplace pensions, retail retirement solutions, and bulk purchase annuities, with mid-single-digit operating cash generation growth targeted, supported by robust new business inflows and innovative digital offerings, likely to lift revenues and net margins.

- Successful integration of major acquisitions including Standard Life and ReAssure, combined with £250 million expected cost savings, is driving both ongoing expense efficiency and margin expansion, translating into improved operating profit and strong free cash generation that supports future earnings.

- Portfolio optimization, capital-light business growth, and recurring management actions in asset management have materially enhanced both the quality and sustainability of the company's profits and free cash flows, strengthening capital generation and supporting dividend sustainability and shareholder equity.

- Industry-level structural trends such as market consolidation, workplace pension auto-enrollment, upcoming regulatory relief (Solvency II reform), and advances in technology position Phoenix as a leading beneficiary, suggesting durable revenue growth, improved pricing power, and the potential for stronger net margins and cash flow over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Phoenix Group Holdings is £5.5, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Phoenix Group Holdings's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £8.5, and the most bearish reporting a price target of just £5.5.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be £5.5 billion, earnings will come to £789.5 million, and it would be trading on a PE ratio of 8.7x, assuming you use a discount rate of 7.8%.

- Given the current share price of £6.46, the bearish analyst price target of £5.5 is 17.5% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.