Last Update08 Oct 25Fair value Decreased 1.00%

Unilever's analyst price target has been slightly reduced from $50.35 to $49.85, as analysts cite moderating revenue growth prospects, balanced by steady profit margins and ongoing international expansion efforts.

Analyst Commentary

Analyst sentiment on Unilever reflects a mix of growth optimism and areas of caution, leading to a nuanced outlook for the company’s future performance and share valuation.

Bullish Takeaways

- Bullish analysts have set higher price targets and cite confidence in Unilever’s long-term international expansion strategies, particularly its focus on growth markets such as India, Indonesia, and China.

- The company’s profitability profile remains solid. Steady margins support a resilient valuation even as headline growth moderates.

- Recent initiations at favorable ratings highlight confidence in Unilever’s ability to execute its transformation and sustain shareholder returns.

- Unilever continues to attract coverage with buy and outperform recommendations, which suggests positive expectations for both its earnings trajectory and market positioning.

Bearish Takeaways

- Bearish analysts warn that U.S. growth is likely to slow, increasing reliance on emerging markets for incremental revenue gains.

- The company could face challenges if international expansion does not fully offset potential softness in established regions.

- There is skepticism that recent margin stability can persist if inflationary or competitive pressures resurface.

What's in the News

- Unilever CEO Fernando Fernandez plans to replace approximately a quarter of the company's top 200 managers after reviewing leadership roles individually. This move aims to address what he called "pockets of mediocrity" within the firm (Financial Times).

- Jefferies analyst David Hayes raised Unilever’s price target to 3,900 GBp from 3,800 GBp. He is maintaining an underperform rating and notes reliance on growth in India, Indonesia, and China to support the business as U.S. growth slows (Jefferies).

- Unilever announced the appointment of Srinivas Phatak as Chief Financial Officer, following both internal and external searches. His appointment will take effect from September 16, 2025.

- The company has scheduled a Special/Extraordinary Shareholders Meeting for October 21, 2025, at its London office.

Valuation Changes

- Consensus Analyst Price Target has decreased slightly from $50.35 to $49.85. This reflects a modest decline in fair value estimates.

- Discount Rate has edged down fractionally from 8.38% to 8.37%, indicating only a minimal change in risk assumptions.

- Revenue Growth Expectations have fallen from 2.74% to 2.34%. This suggests tempered projections for Unilever's top-line expansion.

- Net Profit Margin is projected to rise from 12.45% to 12.60%. This implies a small improvement in profitability outlook.

- Future P/E Ratio has declined from 22.13x to 21.57x, pointing to a slight reduction in anticipated market valuation multiples.

Key Takeaways

- Shifting focus to premium, science-led products and divesting non-core brands is streamlining operations, boosting margins, and enhancing long-term profitability.

- Emphasis on digital expansion, emerging markets, and brand investment is fueling sustained revenue growth and stronger competitive positioning.

- Intensifying competition, regional underperformance, input cost pressures, portfolio streamlining, and elevated regulatory scrutiny threaten sustainable revenue growth, margin expansion, and brand stability.

Catalysts

About Unilever- Operates as a fast-moving consumer goods company in the Asia Pacific, Africa, the Americas, and Europe.

- Acceleration of volume growth in key emerging markets (India, China, Indonesia), supported by rising disposable incomes, urbanization, and rapid expansion in digital/e-commerce channels, is expected to drive sustained top-line revenue growth as these markets recover and Unilever gains market share.

- Portfolio transformation with a sharper focus on premium and science-led Personal Care and Beauty & Wellbeing products, coupled with bolt-on acquisitions of fast-growing digitally native brands, is increasing exposure to higher-margin categories and supporting long-term margin and earnings expansion.

- Strategic divestitures, including the demerger of Ice Cream and continued disposal of non-core food brands, are simplifying the business model and structurally raising the gross and operating margin profile of the remaining company, directly improving profitability and ROIC.

- Improved productivity via supply chain digitization, procurement efficiencies, and disciplined cost management (targeted cost savings of €650 million in 2025) are enhancing gross margins, providing additional fuel for competitive brand investment, and supporting higher sustainable earnings growth.

- Increased investment in brand marketing (15–16% of revenue, notably in Power Brands and digital commerce) is driving innovation, strengthening brand equity, and enabling Unilever to better capture evolving consumer demand in wellness, health, and premiumization, likely resulting in higher revenue growth and maintained or expanded market share.

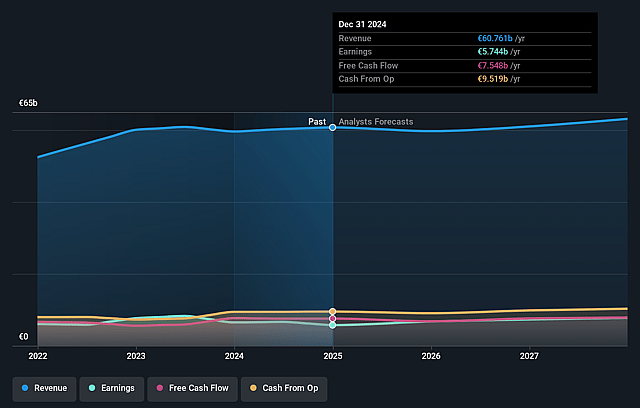

Unilever Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Unilever's revenue will grow by 2.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.3% today to 12.5% in 3 years time.

- Analysts expect earnings to reach €8.1 billion (and earnings per share of €3.27) by about September 2028, up from €5.6 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.1x on those 2028 earnings, down from 24.6x today. This future PE is greater than the current PE for the US Personal Products industry at 18.7x.

- Analysts expect the number of shares outstanding to decline by 0.96% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.38%, as per the Simply Wall St company report.

Unilever Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Intensifying competition from private label and local/niche brands-especially in personal care and food-in key markets like the US and Europe threatens Unilever's long-term pricing power and could erode market share, undermining revenue growth and margin expansion.

- Weak emerging market performance, particularly chronic volume declines in Latin America and flat or negative trends in China and Indonesia, exposes the company to ongoing regional underperformance, creating persistent drag on group revenue and structural headwinds for growth.

- Ongoing input cost inflation (commodities, packaging, transport) and adverse currency movements, especially pronounced in 2025, have pressured operating margins and led to reliance on price increases that may not be sustainable, risking future profitability and earnings.

- The company's continuing portfolio rationalization-including divestitures like the Ice Cream unit and underperforming food brands-could reduce overall scale benefits and increase business concentration, potentially leading to revenue volatility, reduced diversification, and uneven margin trajectory if not offset by sufficient growth in premium categories.

- Heightened regulatory, environmental, and consumer scrutiny around sustainability, ingredient transparency, and global tax regimes-increasing compliance costs and reputational risks-may constrain long-term margin improvement and require ongoing heavy investment to maintain brand equity and customer trust.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £50.35 for Unilever based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £59.26, and the most bearish reporting a price target of just £38.97.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €64.8 billion, earnings will come to €8.1 billion, and it would be trading on a PE ratio of 22.1x, assuming you use a discount rate of 8.4%.

- Given the current share price of £47.62, the analyst price target of £50.35 is 5.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.