Key Takeaways

- Automation, new store expansion, and robotics are expected to drive significant efficiency gains and create opportunities for accelerated growth beyond current market expectations.

- Enhanced digital platforms and loyalty programs could structurally increase order frequency, average basket size, and solidify long-term market leadership against pressured competitors.

- Shifting health trends, regulatory pressures, and rising costs threaten demand, franchisee stability, and profit margins, especially given over-reliance on mature regional markets.

Catalysts

About Domino's Pizza Group- Owns, operates, and franchises Domino’s Pizza stores in the United Kingdom and Ireland.

- Analysts broadly agree that supply chain automation and investment in new facilities will bring margin expansion; however, the accelerating rollout of robotics and digitized logistics is likely to unlock even greater efficiencies, potentially supporting a step-change in EBITDA and freeing capacity for much more aggressive store expansion than consensus estimates reflect.

- Analyst consensus expects digital and loyalty investments to incrementally boost customer frequency, but the bullish case is that a maturing, data-driven CRM platform and full national rollout of the loyalty program could drive a structural uplift in both order frequency and average basket size, with rapid migration of customers into the digital ecosystem permanently raising revenue per customer.

- The unprecedented acceleration of store openings in underserved small towns and rural locations, where initial stores are exhibiting up to six times the national average sales, reveals a vast, previously uncaptured profit pool, suggesting revenue growth and margin expansion from these territories is poised to materially exceed market expectations.

- As competitors are forced to close stores and exit markets under consumer and cost pressures, Domino's is uniquely positioned to capture share and consolidate its market leadership, resulting in accelerated system sales growth and long-term pricing power that will outpace industry peers.

- Rapid shifts in consumer preference toward digital, value-oriented, and ultra-convenient meal solutions, amplified by ongoing inflationary pressures, are likely to disproportionately benefit Domino's accessible delivery and collection model, driving sustained growth in both customer base and topline revenue as higher-frequency, digital-native cohorts increasingly dominate the market.

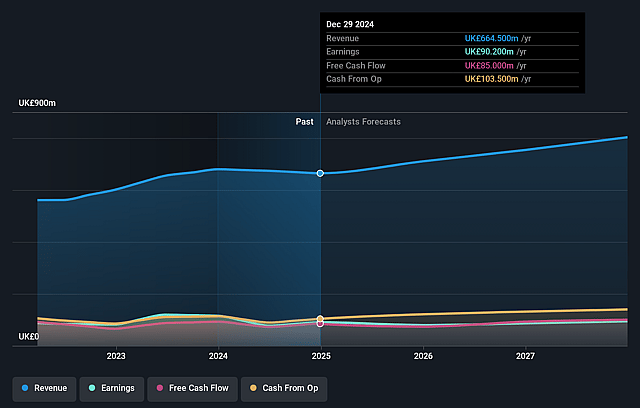

Domino's Pizza Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Domino's Pizza Group compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Domino's Pizza Group's revenue will grow by 7.5% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 11.6% today to 9.9% in 3 years time.

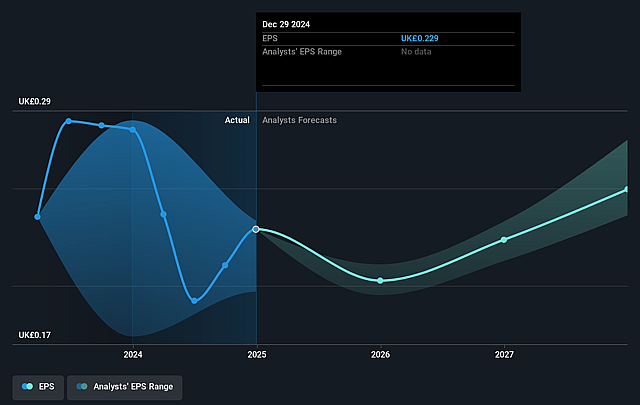

- The bullish analysts expect earnings to reach £82.4 million (and earnings per share of £0.22) by about September 2028, up from £77.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 28.7x on those 2028 earnings, up from 10.2x today. This future PE is greater than the current PE for the GB Hospitality industry at 16.3x.

- Analysts expect the number of shares outstanding to decline by 0.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.85%, as per the Simply Wall St company report.

Domino's Pizza Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The persistent shift towards health and wellness in consumer behavior, along with increased public attention on obesity and unhealthy eating, could reduce demand for Domino's core high-calorie pizza offerings and limit long-term volume growth, negatively affecting revenue.

- Ongoing and potential future government regulation and taxation targeting unhealthy foods, such as high-fat or high-sugar products, risk raising compliance costs and eroding net margins, as the company may be forced to change recipes or absorb higher taxes.

- Rising delivery and logistics expenses, driven by labor cost inflation, fuel price volatility, and stricter urban traffic regulations, threaten to increase Domino's operational expenses and compress earnings, especially as the company relies heavily on its delivery model.

- Franchisee profitability is expected to decline further in the current environment due to wage pressures, increased national insurance costs, and lower volumes, risking franchisee dissatisfaction, potential store closures, and slowing network expansion, which could drag on total system revenue and net margins.

- With a heavy reliance on the mature and potentially saturated UK and Irish markets, Domino's faces risks from local economic downturns or stagnant consumer spending, which may limit sustained top-line growth and make the company more vulnerable to regional shocks.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Domino's Pizza Group is £4.5, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Domino's Pizza Group's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £4.5, and the most bearish reporting a price target of just £1.95.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be £831.5 million, earnings will come to £82.4 million, and it would be trading on a PE ratio of 28.7x, assuming you use a discount rate of 10.9%.

- Given the current share price of £2.05, the bullish analyst price target of £4.5 is 54.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.