Key Takeaways

- Elevated capital and operating expenses from ship purchases and regulatory compliance could strain cash flow and compress net margins, affecting near-term earnings.

- Restructuring, terminal integrations, and substantial vessel investments pose risks to market share and EBIT growth, challenging future earnings sustainability.

- Strong demand, operational improvements, and strategic initiatives like the Gemini network and dual-fuel ships are driving revenue and supporting steady and improved profit margins.

Catalysts

About Hapag-Lloyd- Operates as a liner shipping company worldwide.

- The announcement of new ship purchases to replace aging ships and expand capacity could lead to increased capital expenditure and pressure on cash flow in the short term, potentially impacting net margins.

- The Gemini network restructuring involves costs related to the transition and potential risks of market share loss during implementation, which might affect revenue stability in the short-term.

- Increased operating costs from environmental regulations, rerouting around the Cape of Good Hope, and higher fuel expenses could compress net margins further, affecting earnings in the near future.

- The company anticipates intensified ramp-up costs associated with new terminal business integration, leading to potential profitability fluctuations, impacting EBIT growth projections.

- A high order book of 24 new vessels, which will require substantial future capital investment, potentially diluting returns on invested capital, could impact future earnings sustainability.

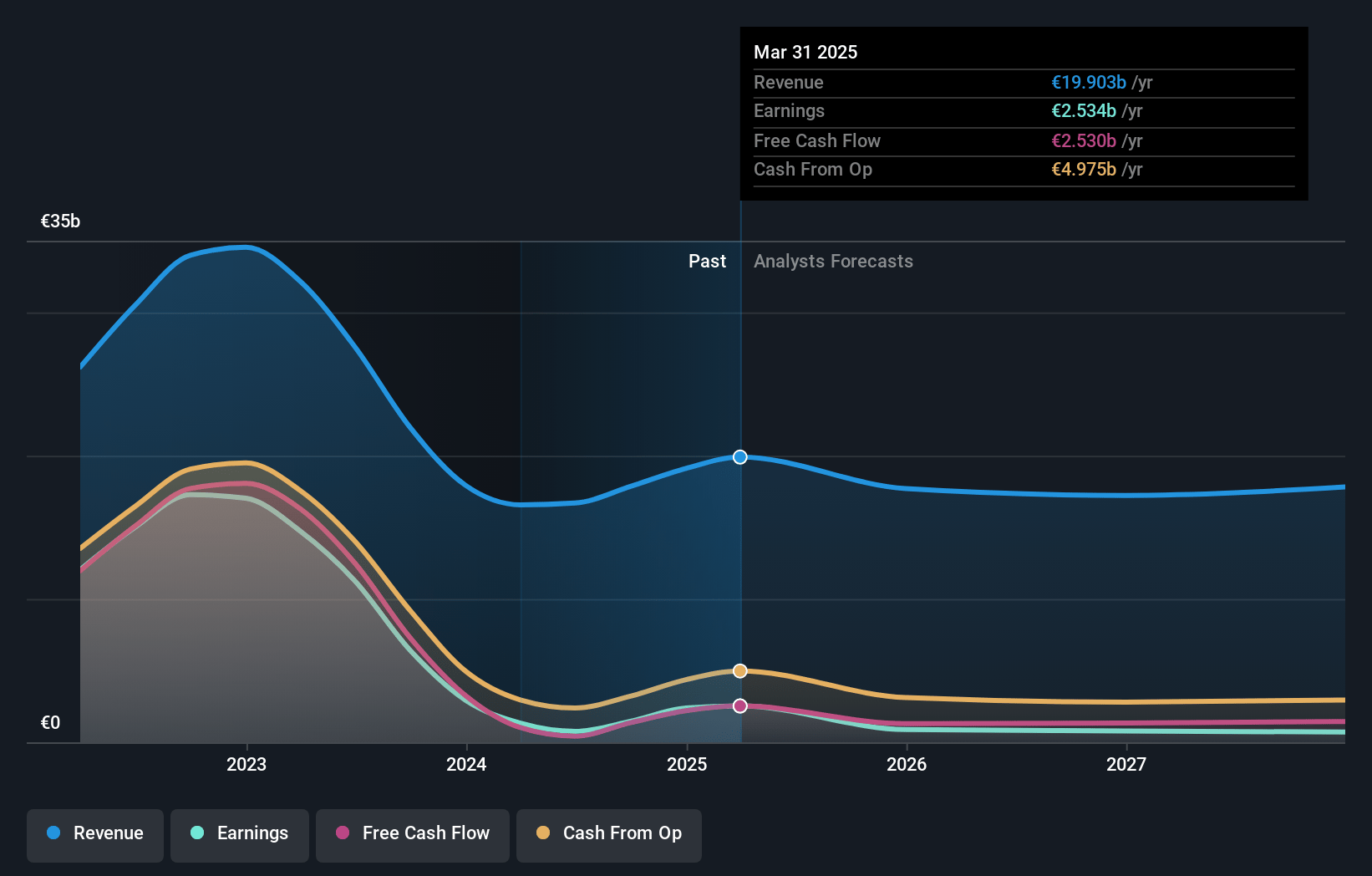

Hapag-Lloyd Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Hapag-Lloyd's revenue will decrease by 0.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 8.2% today to 6.4% in 3 years time.

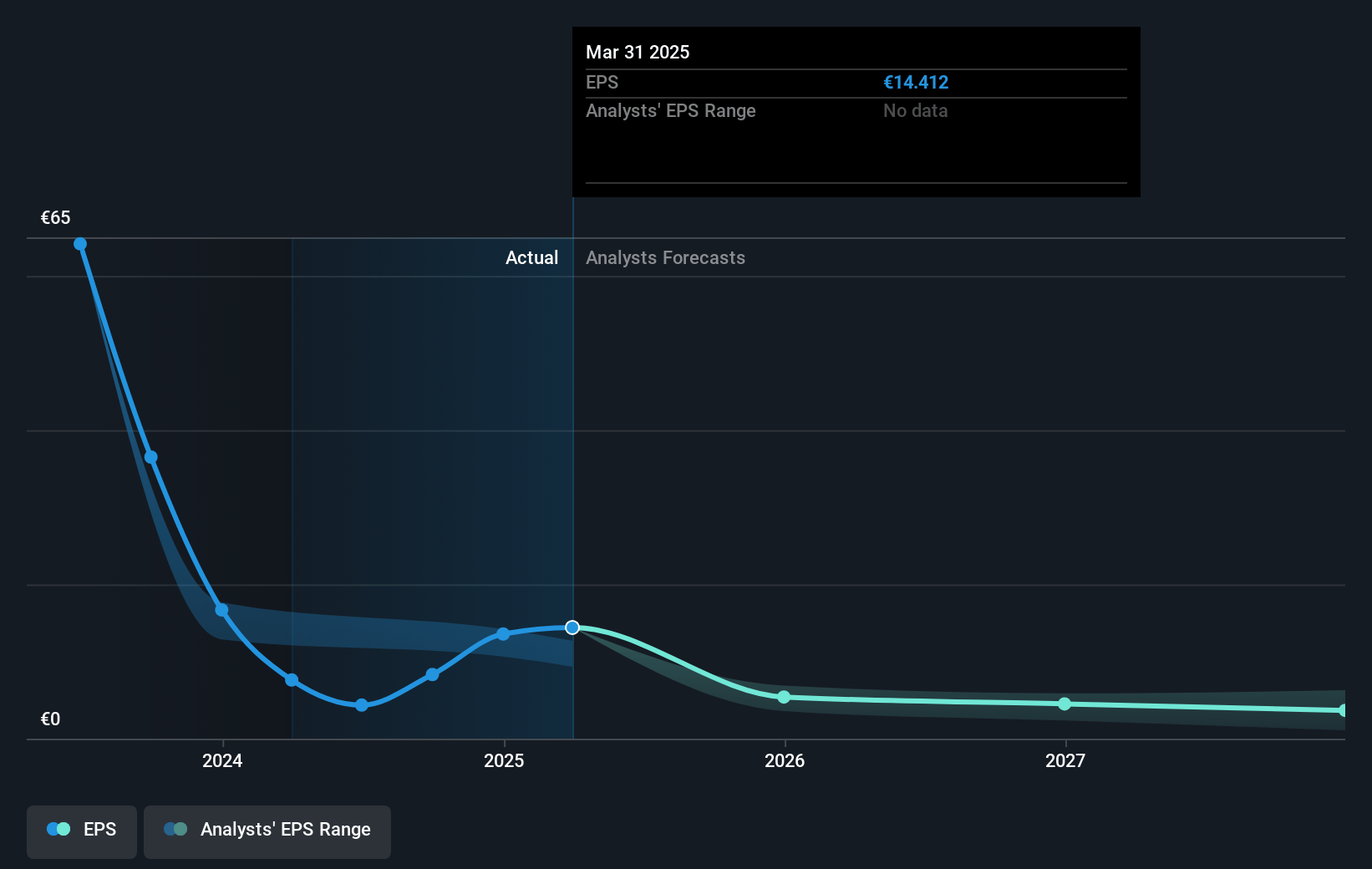

- Analysts expect earnings to reach €1.2 billion (and earnings per share of €6.55) by about January 2028, down from €1.5 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €1.4 billion in earnings, and the most bearish expecting €648.6 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.2x on those 2028 earnings, up from 16.3x today. This future PE is greater than the current PE for the GB Shipping industry at 10.2x.

- Analysts expect the number of shares outstanding to grow by 0.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.95%, as per the Simply Wall St company report.

Hapag-Lloyd Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Strong demand has been observed, leading to higher-than-expected short-term rates, particularly out of Asia, which could positively impact revenue and earnings.

- The launch of the Gemini network aims to provide higher schedule reliability and better service, possibly attracting more customers or facilitating premium pricing, positively influencing revenue and net margins.

- The new ships ordered are dual fuel with improved fuel efficiency, potentially reducing future operating costs and helping maintain or improve profit margins.

- The global container volume is experiencing healthy growth, with significant demand on Transpacific routes, which could lead to sustained revenue growth and stable earnings.

- The firm has seen high asset utilization and operational improvements, driving earnings growth and providing a buffer against cost fluctuations, supporting steady net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €120.75 for Hapag-Lloyd based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €169.0, and the most bearish reporting a price target of just €80.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €18.1 billion, earnings will come to €1.2 billion, and it would be trading on a PE ratio of 21.2x, assuming you use a discount rate of 5.0%.

- Given the current share price of €135.6, the analyst's price target of €120.75 is 12.3% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives