Key Takeaways

- Growing global protectionism and regulatory pressures threaten export revenue, raise compliance costs, and compress margins.

- Heavy reliance on cyclical polysilicon, commoditization by competitors, and high capital needs constrain profitability and the capacity for innovation.

- Strategic innovation and expansion in specialty chemicals, semiconductors, and biosolutions position the company for enhanced margins, resilience, and growth aligned with global megatrends.

Catalysts

About Wacker Chemie- Provides chemical products worldwide.

- Increasing global trade protectionism and the rise of regionalization are poised to erect higher barriers for German exporters; for Wacker Chemie, this could sharply restrict export-driven revenue growth, especially as ongoing U.S. tariff volatility injects persistent uncertainty into global supply chains and order flows.

- Intensifying regulatory scrutiny on environmental impact and ESG compliance is expected to significantly elevate compliance costs, forcing Wacker Chemie to devote more capital to emissions controls and operational changes, likely compressing net margins over time.

- Wacker's high dependence on cyclical polysilicon markets, particularly solar-grade polysilicon, exposes the company to volatile demand swings; if global supply chains continue to shift and protectionist trade measures accelerate, revenue and earnings could remain suppressed or become increasingly unpredictable.

- Persistent overcapacity and price pressure driven by Asian competitors will continue to commoditize standard product lines; alongside Wacker's still-notable volume in non-specialty chemicals and underwhelming margins in standard silicones, this may limit the company's ability to sustainably lift profitability from specialty growth initiatives.

- Large, recurring capital expenditure requirements-both to stay compliant with tightening regulations and to keep up with technological shifts-will constrain free cash flow, restrict investment in innovation, and ultimately weigh on long-term earnings and shareholder returns.

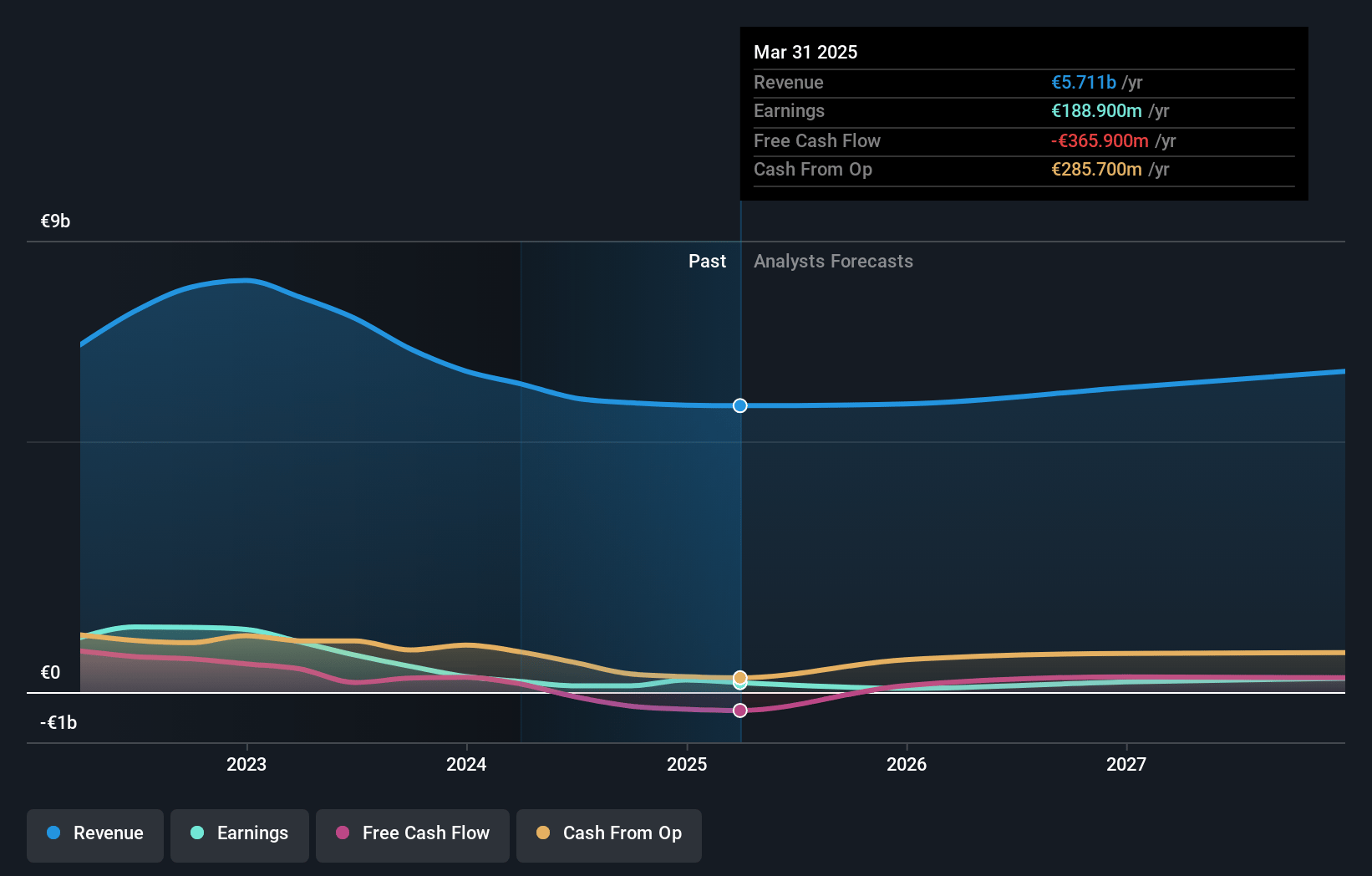

Wacker Chemie Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Wacker Chemie compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Wacker Chemie's revenue will decrease by 0.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 3.3% today to 3.6% in 3 years time.

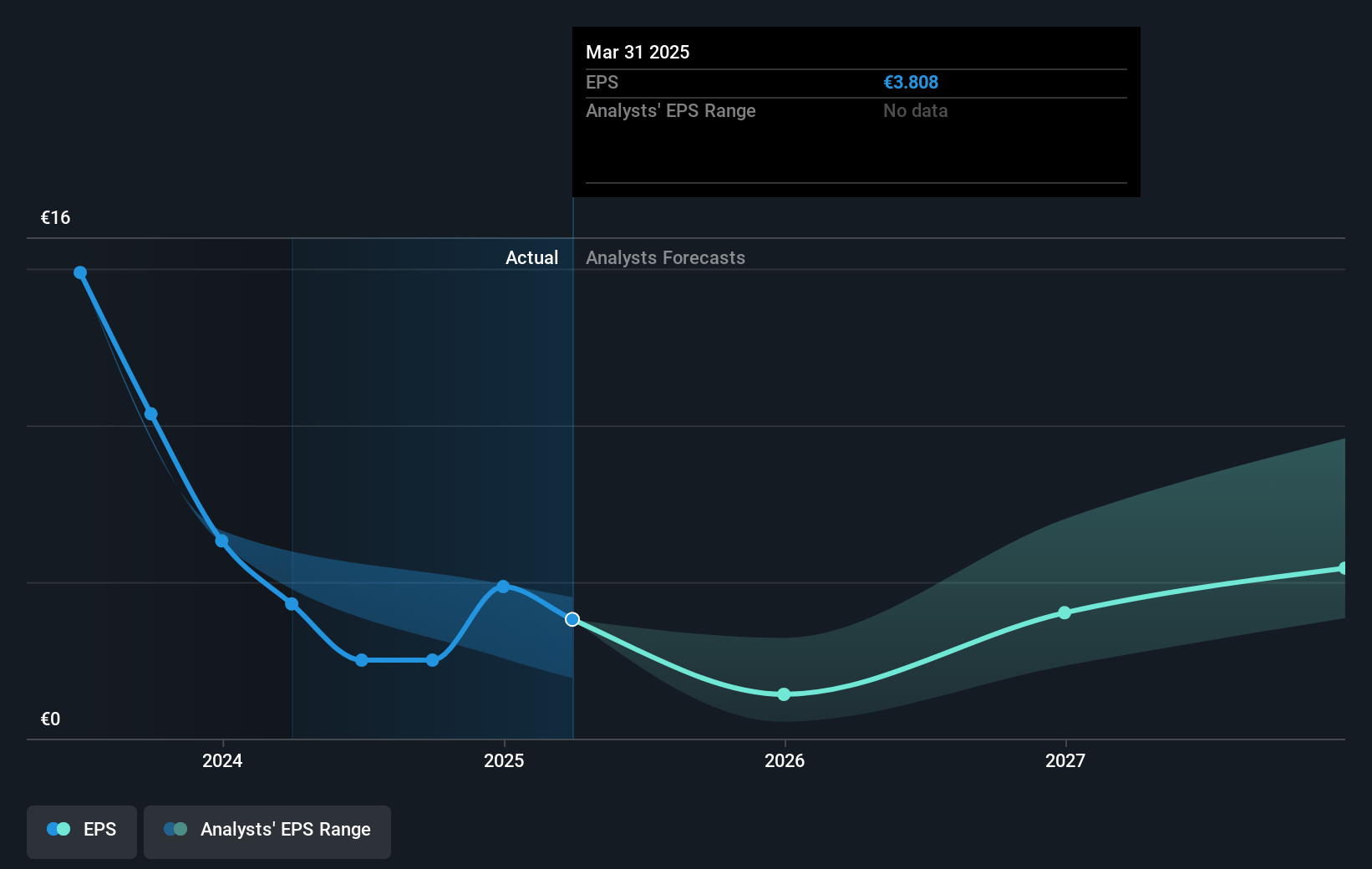

- The bearish analysts expect earnings to reach €211.6 million (and earnings per share of €4.25) by about July 2028, up from €188.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 11.4x on those 2028 earnings, down from 18.5x today. This future PE is lower than the current PE for the GB Chemicals industry at 18.5x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.1%, as per the Simply Wall St company report.

Wacker Chemie Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Wacker Chemie's ongoing focus on specialty silicones and chemical specialties, combined with innovation in new products such as hybrid polymers, eco-line sealants, and coatings for high-value infrastructure, could enhance its product mix and lift profit margins over the long term, supporting higher earnings and net margins.

- The company is ramping up next-generation semiconductor polysilicon production, with its new etching line in Burghausen and strong contracted market share of about 50 percent, positioning it well to benefit from the global trends in semiconductor electronics and potential growth in revenue and gross margins.

- Wacker's persistent efficiency and cost-cutting initiatives, as demonstrated by nearly 1,000 projects in the previous year yielding significant energy and operating cost savings, should improve operational resilience and free cash flow, enabling improved long-term net income.

- The group's expansion in high-value biopharma and biosolutions, supported by global assets and projects beyond the European Union, opens up access to growing life sciences and healthcare markets, supporting revenue diversification and long-term earnings stability.

- Long-term global megatrends such as renewable energy, electromobility, sustainable construction, and digitalization-which directly align with Wacker's core product offerings-are expected to drive structural volume and pricing growth, potentially resulting in sustained improvements in revenue and profit.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Wacker Chemie is €52.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Wacker Chemie's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €113.0, and the most bearish reporting a price target of just €52.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be €5.8 billion, earnings will come to €211.6 million, and it would be trading on a PE ratio of 11.4x, assuming you use a discount rate of 6.1%.

- Given the current share price of €70.35, the bearish analyst price target of €52.0 is 35.3% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.