Key Takeaways

- Strategic investments and project ramp-up costs may reduce margins and earnings, impacting return on capital employed.

- Reduced pricing and lower sulfuric acid revenues could compress net margins, negatively affecting profitability and earnings growth.

- Aurubis demonstrates strong financial resilience and growth potential through strategic projects, diversified supply, and stable demand, countering potential share price declines.

Catalysts

About Aurubis- Processes metal concentrates and recycling materials in Germany.

- There are concerns about reduced pricing in the concentrate market, leading to reduced treatment charges and refining charges (TC/RCs). This could negatively impact Aurubis' revenue.

- The company anticipates ramp-up costs for strategic projects around €50 million during the fiscal year, which can weigh on earnings and net margins.

- Strategic investments are expected to temporarily increase capital employed, potentially reducing return on capital employed (ROCE) in the coming years, affecting overall earnings.

- Lower sulfuric acid revenues compared to prior years and anticipated subdued recycling material RCs might compress net margins, impacting profitability.

- Continued high investments in strategic projects mean that cash flow could remain negative in the short term, affecting free cash flow and possibly leading to lower earnings growth.

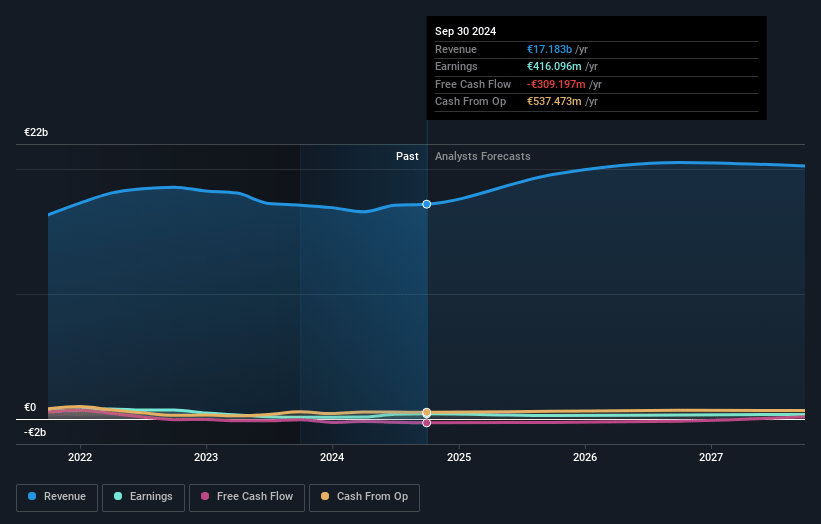

Aurubis Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Aurubis's revenue will grow by 5.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 2.4% today to 1.8% in 3 years time.

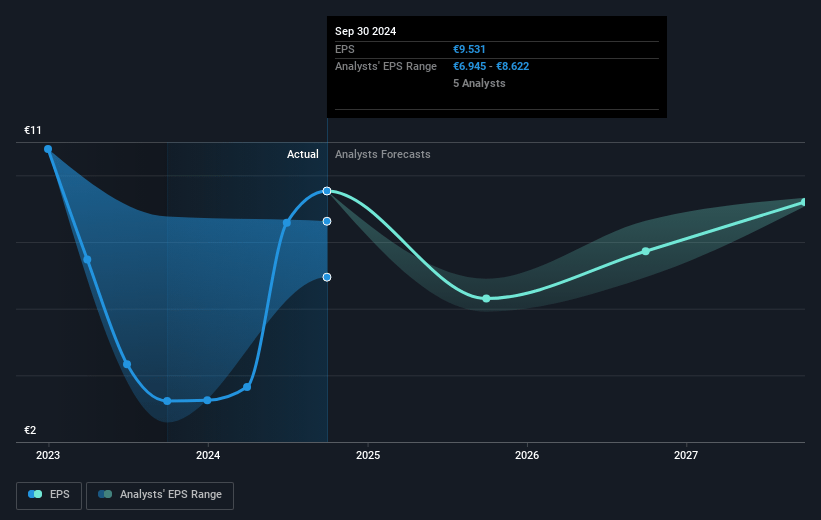

- Analysts expect earnings to reach €364.4 million (and earnings per share of €8.35) by about January 2028, down from €416.1 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €407.1 million in earnings, and the most bearish expecting €290 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.4x on those 2028 earnings, up from 7.6x today. This future PE is lower than the current PE for the GB Metals and Mining industry at 13.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.59%, as per the Simply Wall St company report.

Aurubis Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Aurubis demonstrated strong financial performance with a significant operating EBT increase to €413 million, highlighting earnings strength despite market conditions, which could counter potential share price declines by bolstering earnings.

- The company completed 5 out of 11 strategic projects, with expectations of up to €260 million EBITDA contribution over the next 3-4 years, indicating potential revenue growth from new investments, which could challenge the belief of a decreasing share price.

- Aurubis has a solid cash position of €322 million and is expected to generate a net cash flow between €500 million and €600 million, showing financial resilience and capability to fund growth, positively impacting free cash flow.

- Despite anticipated tighter TC/RC market conditions, Aurubis' diversified supplier base and long-term contracts provide stability, mitigating potential revenue volatility.

- Ongoing demand for copper and strong pricing of precious metals, combined with a commitment to delivering on strategic plans and maintaining dividend payouts, suggest stable revenue and encouraging profit margins, which are supportive factors against share price decline.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €75.2 for Aurubis based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €90.0, and the most bearish reporting a price target of just €58.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €20.1 billion, earnings will come to €364.4 million, and it would be trading on a PE ratio of 10.4x, assuming you use a discount rate of 5.6%.

- Given the current share price of €72.65, the analyst's price target of €75.2 is 3.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives