Key Takeaways

- Margin pressures and reduced sales volumes affect profitability, with potential impacts from delayed projects and customer mix issues in the Electronics segment.

- Challenges in Lifecycle and a slowdown in electrification threaten future revenue and earnings growth, with negative net cash flow remaining an ongoing concern.

- Expanding global order intake and focus on cost reductions could enhance revenue growth and financial stability, offsetting recent declines in electronics.

Catalysts

About HELLA GmbH KGaA- Develops, manufactures, and sells lighting systems and electronic components for automotive industry worldwide.

- A major reason for the negative growth in the Electronics segment, with a decline of 3.2%, is due to delayed start of production (SOP) projects, customer mix issues, and a significant reduction in sales of electrified cars. This impacts anticipated future revenue needed to drive growth.

- The company has been facing margin pressures leading to a reduction in its income margin from 6.1% last year to 5.8% this year, attributed to lower gross profit margins due to reduced sales volumes and negative mix effects. This is likely to continue impacting profitability.

- Challenges in the Lifecycle segment, particularly in the SOE business, with sales down by 20% due to lower demand in key sectors like agriculture and construction, could hinder revenue growth announcements in the future.

- The slowdown in electrification and one-off impacts from the end of high-volume programs, as mentioned with clients in China like Tesla, pose threats to segments like Electronics and Lighting, impacting future earnings.

- Despite efforts to improve the net cash flow and operational excellence, net cash flow remains negative, and while improvement is expected by year-end, the uncertainties could still weigh on lenders and affect future earnings visibility.

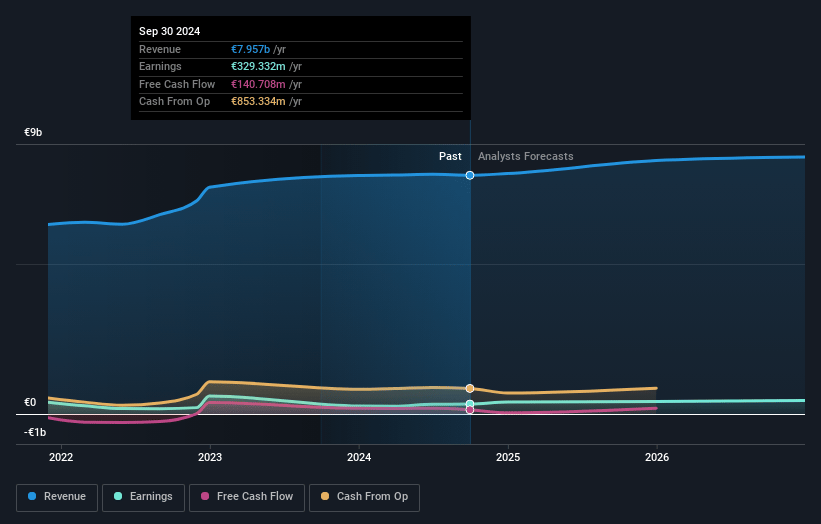

HELLA GmbH KGaA Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming HELLA GmbH KGaA's revenue will grow by 3.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.1% today to 5.6% in 3 years time.

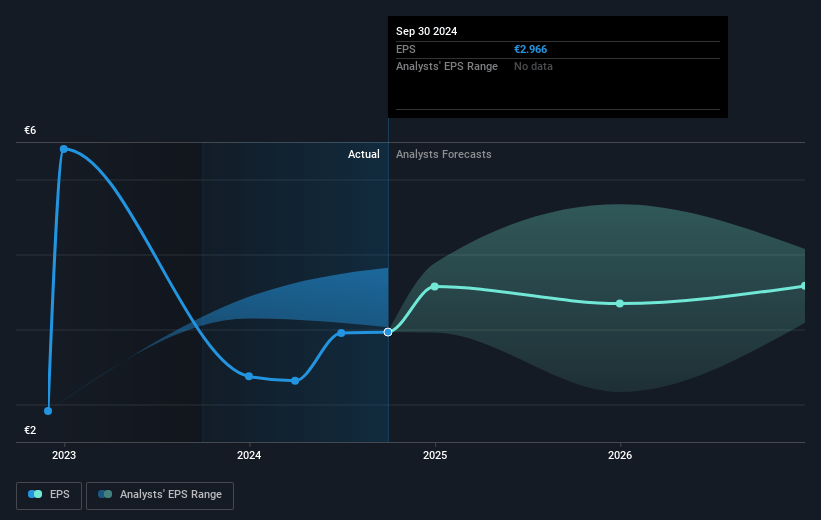

- Analysts expect earnings to reach €499.6 million (and earnings per share of €3.73) by about January 2028, up from €329.3 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.0x on those 2028 earnings, down from 30.4x today. This future PE is greater than the current PE for the GB Auto Components industry at 9.3x.

- Analysts expect the number of shares outstanding to grow by 6.4% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.26%, as per the Simply Wall St company report.

HELLA GmbH KGaA Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company expects cash inflows and improvements in working capital by the end of the year, which may enhance their net cash flow and overall financial stability.

- Order intake is increasing and diversifying globally, particularly outside of Europe. This suggests potential future revenue improvements as HELLA expands its market reach.

- HELLA is focusing on cost reductions and operational excellence, including automation and process improvements, which could improve net margins.

- The Electronics segment won significant business in new markets such as the U.S., Japan, India, and China. This expansion may enhance revenue growth and offset recent declines in electronic sales.

- HELLA's investments in new technologies and sustainability initiatives could position them favorably to capture market demand and improve earnings over time.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €71.0 for HELLA GmbH KGaA based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €8.9 billion, earnings will come to €499.6 million, and it would be trading on a PE ratio of 22.0x, assuming you use a discount rate of 5.3%.

- Given the current share price of €90.2, the analyst's price target of €71.0 is 27.0% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives