Key Takeaways

- Weak credit demand, demographic shifts, and property sector risks threaten revenue growth, asset quality, and future earnings.

- Rising competition and slow core deposit growth pressure profitability, while regulatory tightening escalates operational challenges.

- Strategic focus on digitalization, risk management, and policy-aligned lending is improving efficiency, asset quality, and earnings while diversifying revenues and supporting sustainable growth.

Catalysts

About Ping An Bank- Provides commercial banking products and services for individual and corporate customers, government agencies, institutions, and other small businesses in China and internationally.

- The persistent decline in effective credit demand due to China's demographic challenges and economic slowdown is expected to limit Ping An Bank's long-term revenue growth, while also increasing the risk of higher non-performing loan ratios as the population ages and consumption weakens.

- Intensifying competition from digital platforms and fintech disruptors is set to compress Ping An Bank's net interest margins further, undermining its ability to sustain profitability even as it increases investments in digital transformation and technology initiatives.

- Ping An Bank's significant and potentially rising exposure to real estate lending leaves it highly vulnerable to ongoing downturns in China's property sector, thus increasing credit costs and eroding asset quality, a trend likely to weigh heavily on future earnings.

- Slower-than-peer progress in core deposit growth threatens to elevate funding costs and inhibit net interest margin expansion, placing additional pressure on the bank's ability to maintain or expand profit margins over the long term.

- Regulatory tightening and ongoing industry consolidation will likely lead to increased compliance costs and intensified competition, reducing fee income opportunities and making it more difficult for Ping An Bank to differentiate itself, ultimately dampening both revenue and earnings prospects.

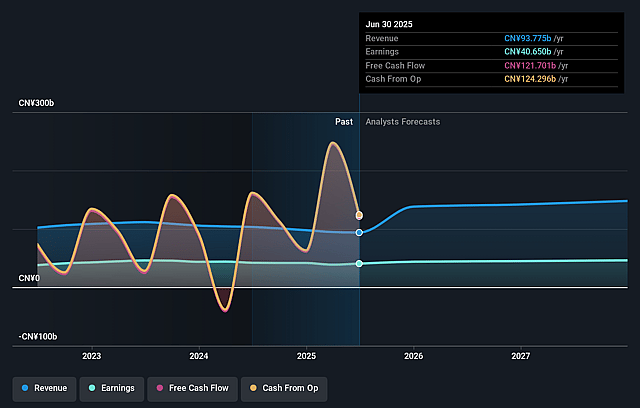

Ping An Bank Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Ping An Bank compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Ping An Bank's revenue will grow by 15.5% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 41.0% today to 29.1% in 3 years time.

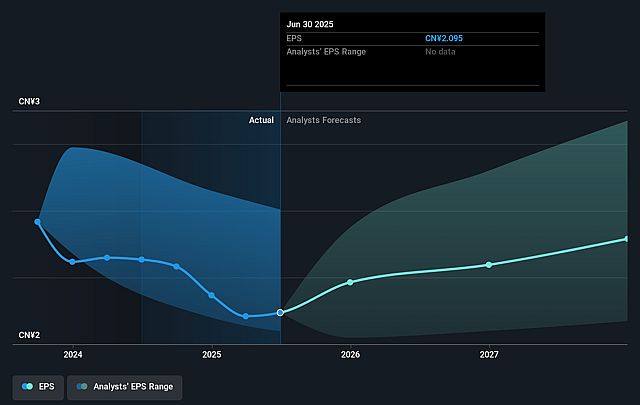

- The bearish analysts expect earnings to reach CN¥42.4 billion (and earnings per share of CN¥2.11) by about August 2028, up from CN¥38.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 6.9x on those 2028 earnings, up from 6.2x today. This future PE is greater than the current PE for the CN Banks industry at 6.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.03%, as per the Simply Wall St company report.

Ping An Bank Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ping An Bank's significant and ongoing investment in digitalization, artificial intelligence, and technology-enabled services positions it to enhance operational efficiency, lower costs, and provide differentiated customer experiences, which could translate to improved profit margins and strengthen long-term earnings.

- The bank has demonstrated a robust approach to risk management, with a stable non-performing loan (NPL) ratio and a high provision coverage ratio, suggesting that asset quality is resilient and credit costs could remain contained over time, directly benefiting net profit and reducing downside risk.

- Structural reforms and strategic transformation within the retail banking segment, including the removal of high-risk assets and the rollout of medium-risk products, indicate the potential for a return to positive growth in retail lending and improved asset quality, which could support higher revenues and earnings.

- Continued expansion and high growth in corporate lending, particularly in sectors supported by government policy (such as infrastructure, green finance, and technology), as well as successful cross-selling through the Ping An Group ecosystem, can drive top-line revenue growth and diversify income streams.

- Favorable government initiatives-such as policies to boost consumption and credit demand, along with emphasis on supporting technology, small

- and medium-sized enterprises, and real economy sectors-create a supportive macro environment that could stimulate loan growth, increase fee income, and underpin sustainable improvement in the bank's financial results.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Ping An Bank is CN¥11.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Ping An Bank's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CN¥17.19, and the most bearish reporting a price target of just CN¥11.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be CN¥146.0 billion, earnings will come to CN¥42.4 billion, and it would be trading on a PE ratio of 6.9x, assuming you use a discount rate of 11.0%.

- Given the current share price of CN¥12.4, the bearish analyst price target of CN¥11.0 is 12.7% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.