Key Takeaways

- UBS has reduced execution risk from the Credit Suisse acquisition, boosting revenue and margins through integration and operational optimization.

- Strategic investments in technology and expanding presence in the Americas aim to enhance leverage, profitability, and growth while delivering significant cost reductions.

- UBS faces profitability challenges from interest rate headwinds, elevated credit loss expenses, costly Credit Suisse integration, regulatory uncertainties, and competitive pressures in investment banking.

Catalysts

About UBS Group- Provides financial advice and solutions to private, institutional, and corporate clients worldwide.

- UBS has successfully reduced its execution risk related to the Credit Suisse acquisition by completing major legal entity mergers and client account migrations, positioning the company for improved revenue and net margins as it integrates and optimizes operations.

- Despite current macroeconomic challenges, UBS continues to make strategic investments in technology and capabilities, which are expected to enhance operating leverage, improve profitability, and drive sustainable future revenue growth across its Global Wealth Management and Investment Bank divisions.

- UBS plans to deliver significant cost reductions by decommissioning legacy infrastructure and achieving $13 billion in gross cost savings by 2026. These savings will directly impact net margins and earnings as the company optimizes its cost structure while enhancing its tech capabilities.

- The company is focusing on expanding its presence in the Americas through targeted investments and an enhanced product offering. This strategic shift is expected to contribute to revenue growth and better earnings as UBS capitalizes on opportunities to serve ultra-high-net-worth and affluent clients.

- UBS's strong capital position, with a CET1 ratio of 14.3%, along with plans for increased dividend payouts and share repurchases, is designed to enhance shareholder returns while maintaining financial stability. This approach supports the company's EPS growth target by improving capital efficiency and delivering attractive capital returns by 2026.

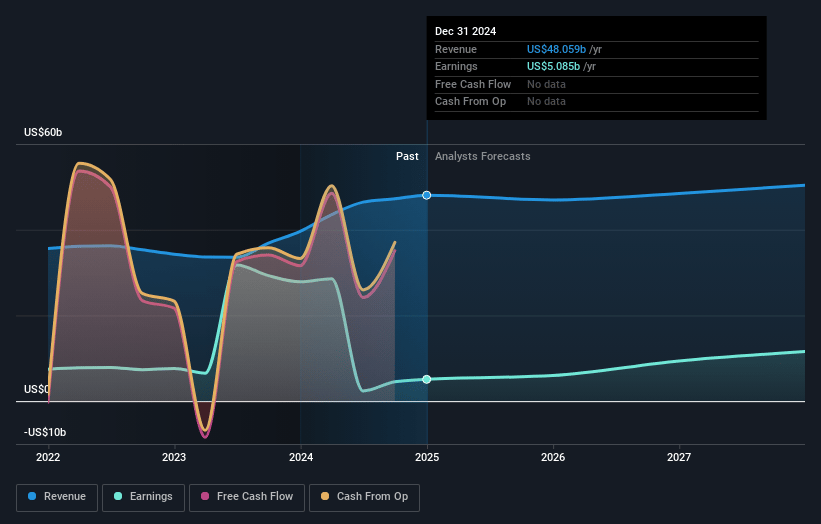

UBS Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming UBS Group's revenue will grow by 2.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.6% today to 23.0% in 3 years time.

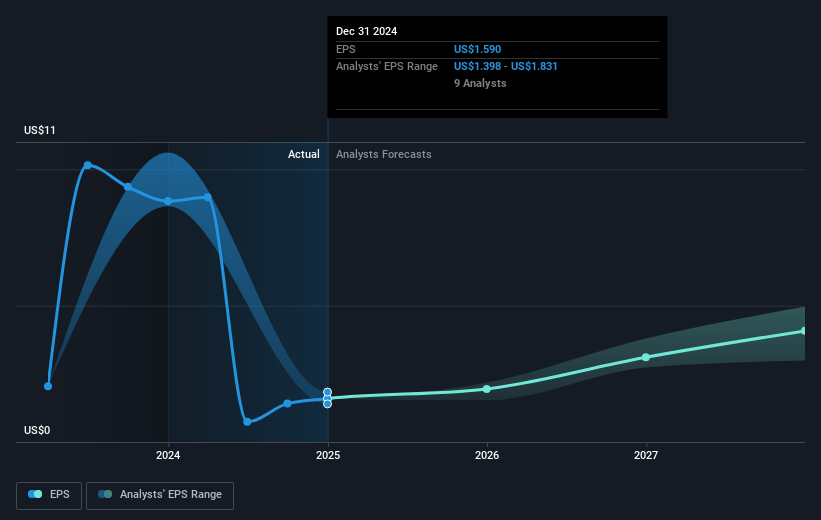

- Analysts expect earnings to reach $11.9 billion (and earnings per share of $4.12) by about March 2028, up from $5.1 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $13.7 billion in earnings, and the most bearish expecting $10.0 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.2x on those 2028 earnings, down from 20.6x today. This future PE is lower than the current PE for the GB Capital Markets industry at 17.7x.

- Analysts expect the number of shares outstanding to decline by 0.99% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.02%, as per the Simply Wall St company report.

UBS Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The prospect of declining interest rates in the Swiss franc and euro, combined with pre-acquisition Credit Suisse loan maturities, poses a significant headwind to UBS’s net interest income and profitability in their Personal and Corporate Banking division throughout 2025. This is likely to weigh on total NII and affect revenue generation.

- Elevated credit loss expenses, particularly from legacy Credit Suisse portfolios, are expected to remain a burden in 2025, impacting UBS's net margins and overall earnings. This reflects ongoing financial vulnerabilities in certain sectors, such as metals and automotive industries.

- The integration of Credit Suisse remains a complex and costly endeavor, with a projected cumulative integration-related expense of around $14 billion, potentially straining net earnings and profit margins in the near term as the company works through significant restructuring efforts.

- There is uncertainty regarding potential regulatory changes in Switzerland, particularly in capital requirements, which could necessitate higher capital retention and consequently impact UBS's return on equity. This regulatory uncertainty creates a risk to earnings and capital flexibility.

- Despite the ongoing integration and restructuring efforts, UBS still faces competitive pressures and market share challenges, especially in the Investment Bank division, where revenue growth may be constrained by broader market conditions and performance relative to peers.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CHF31.941 for UBS Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF44.5, and the most bearish reporting a price target of just CHF21.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $51.5 billion, earnings will come to $11.9 billion, and it would be trading on a PE ratio of 12.2x, assuming you use a discount rate of 9.0%.

- Given the current share price of CHF29.06, the analyst price target of CHF31.94 is 9.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.