Last Update 23 Jul 26

Fair value Increased 27%ARIS: Future Production Outlook Signals Bullish Upside Potential

Analysts have revised their fair value estimate for Aris Mining to CA$34.82 from CA$27.45. This revision reflects updated assumptions around discount rates, revenue growth, profit margins and future P/E levels.

What’s in the News for Aris Mining

- Aris Mining reported unaudited consolidated gold production of 73.7 koz for Q2 2026, which the company stated was up 26% compared with Q2 2025, according to its recent operating results announcement.

- For the first half of 2026, Aris Mining reported consolidated gold production of 148.0 koz, described by the company as a 31% increase over the first half of 2025, based on its production update.

- In a separate announcement, Aris Mining stated that first half 2026 gold production reached 148,000 ounces and that it remains on track with 2026 production guidance of 300,000 to 350,000 ounces, with full Q2 2026 financial and operating results scheduled for release on July 29, 2026, along with a conference call. Source: Company guidance update.

- Aris Mining reported that revenues from gold sales in the first half of 2026 were above US$680 million, alongside ongoing expansion efforts across properties in Colombia, Canada, and Guyana. Source: Company guidance update.

- Nearby in Colombia’s Segovia Gold District, Quimbaya Gold Inc. reported identifying a new gold target at Tahami Southeast adjacent to Aris Mining’s high grade operations, with initial rock samples reportedly up to 59.4 g/t gold and 52.30 g/t silver. Source: Quimbaya Gold exploration update.

Valuation Changes for Aris Mining

- Fair Value: The updated fair value estimate for Aris Mining has increased from CA$27.45 to CA$34.82.

- Discount Rate: The discount rate has increased from 7.43% to 8.17%, indicating a higher required return in the model.

- Revenue Growth: The assumed revenue growth rate has been reduced from 46.90% to 30.92%.

- Net Profit Margin: The assumed net profit margin has been revised from 34.63% to 30.27%.

- Future P/E: The expected future P/E multiple has moved up from 7.37x to 8.79x.

Catalysts

About Aris Mining

Aris Mining operates gold mines and develops large-scale gold projects in Colombia and Guyana.

What are the underlying business or industry changes driving this perspective?

- While the ramp-up at Segovia following the second ball mill installation is increasing throughput capacity to 3,000 tonnes per day, the plan to source more tonnes from Contract Mining Partners and underground development could strain mine planning and grade control, which may limit future gains in revenue and compress all-in sustaining cost margins if ore quality or dilution is not carefully managed.

- Although Marmato’s Bulk Mining Zone is progressing with major equipment on site and first gold targeted for the second half of 2026, the need for a sharp increase in construction capital spending and dependence on timely power line permitting introduces execution and timing risk that could pressure free cash flow and delay contributions to earnings.

- While the pre-feasibility study for Soto Norte outlines a long-life, low-cost underground operation with an expected environmental license application in the first half of 2026, the lengthy permitting process and extensive environmental and social commitments may extend timelines and raise compliance costs, which could defer EBITDA and net earnings from this project.

- Despite Toroparu’s long-life open pit profile and ongoing work to move from a preliminary economic assessment to a pre-feasibility study by 2026, the US$820 million initial capital requirement and reliance on stable governmental support in Guyana could constrain balance sheet flexibility and pressure future returns on capital, with knock-on effects on cash generation and earnings if costs rise.

- While the company currently reports low net leverage, no significant debt maturities until October 2029 and strong trailing 12-month adjusted EBITDA, the simultaneous funding needs for Marmato, Toroparu and eventually Soto Norte may require careful capital allocation choices that could limit future margin expansion and slow growth in net income if internal cash flow proves insufficient.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Aris Mining compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Aris Mining's revenue will grow by 30.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 15.2% today to 30.3% in 3 years time.

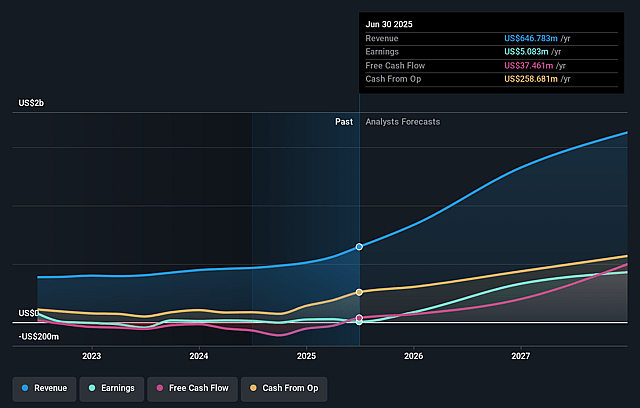

- The bearish analysts expect earnings to reach $776.2 million (and earnings per share of $3.66) by about July 2029, up from $173.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 8.8x on those 2029 earnings, down from 17.7x today. This future PE is lower than the current PE for the CA Metals and Mining industry at 14.4x.

- The bearish analysts expect the number of shares outstanding to grow by 1.98% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.17%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- If the ramp-up at Segovia continues to lift throughput towards 3,000 tonnes per day while maintaining grades near 9.9 grams per tonne and recoveries around 96.1%, the combination of higher volumes and strong all in sustaining cost margins could support higher gold output and cash generation over time, which may put upward pressure on revenue and earnings.

- The Marmato Bulk Mining Zone is described as on schedule, with key earthworks largely complete, major equipment on site and first gold targeted for the second half of 2026. Successful completion and ramp-up could add a new source of production and free cash flow, which may change expectations for future net margins and earnings.

- Long life projects such as Soto Norte and Toroparu are outlined with multi decade mine lives, sizable reserves and resources, and projected annual EBITDA figures in the hundreds of millions of US dollars at the assumed gold prices in the studies. If either project advances through permitting and construction in line with management plans, the additional production capacity could materially lift long term revenue and earnings.

- The company currently reports adjusted trailing 12 month EBITDA of US$352 million, cash of US$418 million, net debt of US$64 million and low net leverage of 0.2x with no significant debt maturities until October 2029. If this balance sheet strength is maintained while funding growth projects, it could support expansion without heavy dilution, with potential benefits for future earnings per share and free cash flow.

- Management repeatedly highlights a backdrop of rising gold prices and uses assumed gold prices of US$2,600 and US$3,000 per ounce in project studies. If the long term gold price environment remains supportive or improves relative to these assumptions, realized pricing on current and future production could be higher than implied by a flat share price view, which would likely impact revenue and all in sustaining cost margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Aris Mining is CA$34.82, which represents up to two standard deviations below the consensus price target of CA$40.69. This valuation is based on what can be assumed as the expectations of Aris Mining's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$46.27, and the most bearish reporting a price target of just CA$34.82.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $2.6 billion, earnings will come to $776.2 million, and it would be trading on a PE ratio of 8.8x, assuming you use a discount rate of 8.2%.

- Given the current share price of CA$20.97, the analyst price target of CA$34.82 is 39.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Aris Mining?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.