Key Takeaways

- Expansion into the U.S. and operational efficiencies position Zedcor to capture market share and drive recurring, high-margin revenue growth.

- Differentiated AI-enabled solutions and compliance advances will broaden the customer base and support sustained improvement in profitability and earnings stability.

- Margin pressure, high capital intensity, increasing competition, labor shortages, and rising technology standards are key risks that may hinder profitability, returns, and competitive positioning.

Catalysts

About Zedcor- Provides turnkey and customized mobile surveillance and live monitoring solutions in Canada and the United States.

- Rapid expansion of U.S. operations and increasing tower deployment, combined with strong demand from both new and existing customers, positions Zedcor to capture a larger share of a growing North American market for remote security and surveillance solutions-supporting strong recurring revenue growth.

- Ongoing digital transformation among clients and Zedcor's increasing investment in in-house, AI-enabled monitoring (such as Live Verified Monitoring and advanced camera features) differentiates its offerings, expands the high-margin VSaaS platform, and is expected to drive further improvement in net margins.

- Strategic geographic expansion, with plans to double U.S. branch count and achieve sub-8-hour service coverage, will both increase addressable market size and reduce customer concentration risk-boosting topline revenue and improving earnings stability.

- Manufacturing efficiency gains and scale (e.g., decreasing tower costs, larger facilities, and the ability to rapidly ramp up production) are lowering unit costs and improving gross margins, which should support EBITDA margin expansion as density builds in new markets.

- Progress towards industry-leading compliance standards (such as SOC 2) and successful penetration into large enterprise retail and logistics sectors will enable access to new, high-value contracts-expanding the customer base and driving sustainable long-term revenue growth.

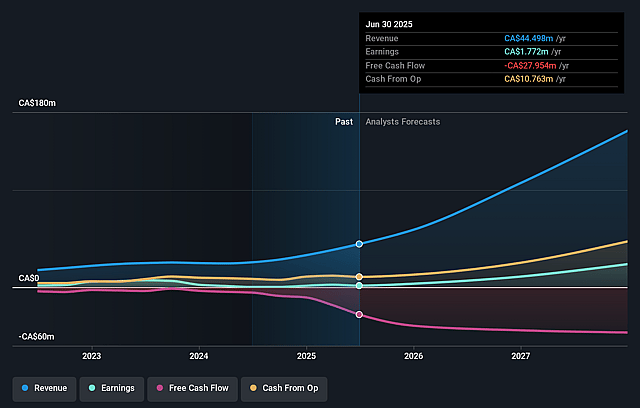

Zedcor Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Zedcor's revenue will grow by 62.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.0% today to 17.0% in 3 years time.

- Analysts expect earnings to reach CA$32.5 million (and earnings per share of CA$0.31) by about September 2028, up from CA$1.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.0x on those 2028 earnings, down from 254.3x today. This future PE is greater than the current PE for the CA Trade Distributors industry at 14.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.08%, as per the Simply Wall St company report.

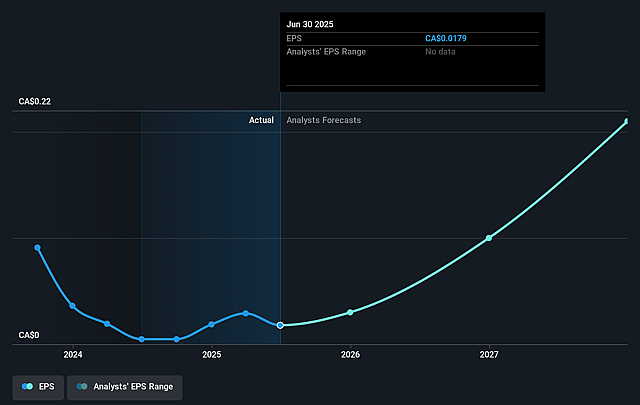

Zedcor Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Significant margin pressure in the U.S. versus Canada (26% vs. 66% EBITDA margins) indicates it may take years for U.S. profitability to catch up, and even then, competitive dynamics or regional cost structure could prevent margins from matching Canadian levels, impacting long-term EBITDA and net earnings.

- Rapid expansion and a high capital expenditure cycle-including a major facility buildout and ongoing investments in fleet and branch openings-raise the risk that revenue growth will not keep pace with asset and debt growth, potentially resulting in compressed returns on capital, higher leverage, and lower free cash flow.

- While Zedcor is winning business with service and integrated in-house monitoring, its core market is seeing increased price competition, especially in the U.S., where some competitors are aggressively discounting; this could pressure Zedcor's ability to maintain premium pricing, risking slower revenue growth or margin compression as the industry matures.

- The company's strategy is highly dependent on scaling its service footprint and workforce across North America, but ongoing labor shortages, particularly in accounting and specialized technical areas, could slow expansion, increase wage costs, or negatively affect execution and operational efficiency, thereby increasing operating expenses and reducing net margins.

- Rising customer expectations for cybersecurity, data privacy (e.g., the need for SOC 2 compliance), and integrated AI features signal an accelerating pace of technological change; if Zedcor fails to keep up with evolving industry standards or faces costly regulatory requirements, it could be exposed to higher compliance costs, liability risks, or technological obsolescence, negatively impacting profitability and long-term competitiveness.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$5.6 for Zedcor based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$7.0, and the most bearish reporting a price target of just CA$5.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$191.5 million, earnings will come to CA$32.5 million, and it would be trading on a PE ratio of 27.0x, assuming you use a discount rate of 7.1%.

- Given the current share price of CA$4.28, the analyst price target of CA$5.6 is 23.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.