Key Takeaways

- Expanding into embedded finance, integrated payments, and AI-powered automation positions Locaweb for accelerated growth, improved profitability, and greater operational efficiency.

- Strategic moves in cloud services, enterprise expansion, and omnichannel retail enhance revenue diversification and strengthen long-term earnings potential.

- Heightened competition from global cloud giants and integrated platforms, rising costs, and innovation challenges threaten Locaweb's revenue growth and long-term profitability.

Catalysts

About Locaweb Serviços de Internet- Offers hosting, software licensing, and technical support services in Brazil.

- Analyst consensus is that leveraging embedded finance, ERP, and improved operational efficiency will boost growth, but with the company's accelerating revenue and sequential margin expansion alongside advanced AI-driven automation, there is potential for sustained, double-digit growth in both revenue and net margin, surpassing current expectations as profitability outpaces topline gains.

- While analysts broadly agree that payments institution authorization could unlock new revenue streams, the combination of a digitally native, integrated payments and credit platform, experienced fintech leadership, and proprietary SME data has potential to create a dominant, multi-vertical financial services business, greatly expanding addressable market and driving a step-change in free cash flow and EPS.

- The soft launch of Locaweb's public cloud service positions the company to capture a material share of Brazil's rapidly growing multi-billion US dollar cloud infrastructure market, enhancing both profitability and revenue diversification as local businesses migrate en masse to cloud-based, AI-enabled commerce and business platforms.

- Locaweb's deep integration of generative AI and automation across both internal operations and all customer-facing workflows is already producing substantial productivity gains-up to eighty percent in areas like engineering-indicating a powerful, durable reduction in cost-to-serve and structural improvement in EBITDA margins for years to come.

- The company's growing base of medium and large enterprise clients, expansion in omnichannel retail, and successful M&A track record signal the start of a new growth cycle in which scaling cross-sell, higher ARPU tools, and consolidated platform stickiness will drive robust subscription revenue growth and durable gains in long-term earnings power.

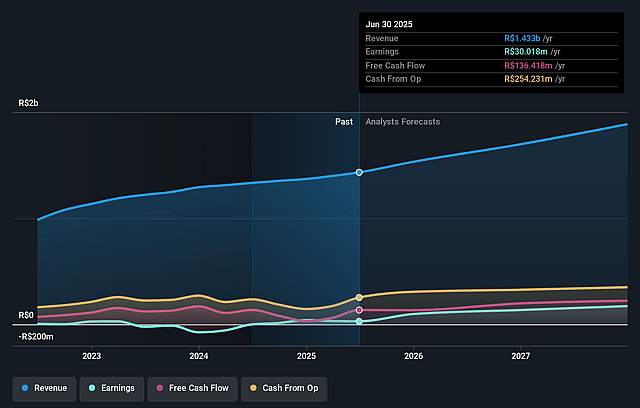

Locaweb Serviços de Internet Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Locaweb Serviços de Internet compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Locaweb Serviços de Internet's revenue will grow by 13.4% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 2.1% today to 12.2% in 3 years time.

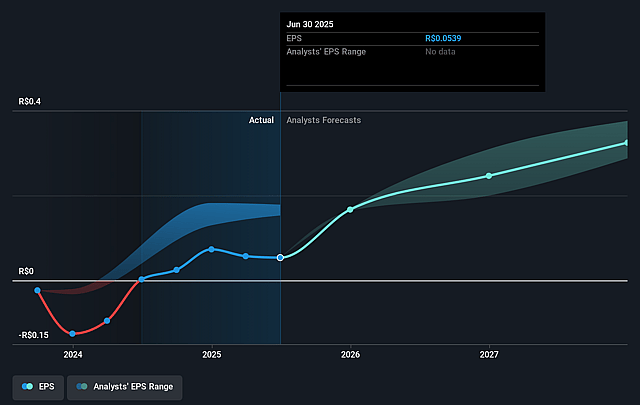

- The bullish analysts expect earnings to reach R$255.7 million (and earnings per share of R$0.48) by about September 2028, up from R$30.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 27.2x on those 2028 earnings, down from 75.6x today. This future PE is lower than the current PE for the BR IT industry at 75.6x.

- Analysts expect the number of shares outstanding to decline by 1.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 21.41%, as per the Simply Wall St company report.

Locaweb Serviços de Internet Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The accelerating dominance of global cloud and SaaS giants such as Amazon, Google, and Microsoft poses a significant risk to Locaweb's future market share and pricing power, given the company's cloud offering is still in soft launch and may struggle to compete on scale and innovation, which could pressure long-term revenues and margins.

- An ongoing shift by small and medium businesses toward integrated e-commerce and social media sales platforms, especially with fast integrations from players like Shopify and Mercado Libre, may bypass traditional hosting and SaaS providers, leading to stagnating or declining future demand for Locaweb's core offerings, impacting its revenue growth trajectory.

- Locaweb's product innovation, while described as improved with AI and integration, may still lag behind both global peers and new regional fintech/tech upstarts, potentially limiting cross-selling/upselling opportunities and reducing the company's ability to lift ARPU and total revenues over the long run.

- Intensifying price competition, both locally and from global entrants, alongside the commoditization of web hosting and digital services with low switching costs, could force Locaweb into ongoing price cuts or higher promotional spending, which would negatively affect net margins and overall earnings.

- Rising technology investment needs-especially for AI and cybersecurity-as well as growing labor costs due to tech sector wage inflation in Brazil, could erode Locaweb's operational leverage and profitability, resulting in squeezed EBITDA margins and greater long-term cost pressures on earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Locaweb Serviços de Internet is R$7.5, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Locaweb Serviços de Internet's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$7.5, and the most bearish reporting a price target of just R$4.1.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be R$2.1 billion, earnings will come to R$255.7 million, and it would be trading on a PE ratio of 27.2x, assuming you use a discount rate of 21.4%.

- Given the current share price of R$4.14, the bullish analyst price target of R$7.5 is 44.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.