Key Takeaways

- Strategic land acquisitions and operational discipline are positioning the company for amplifying earnings, asset appreciation, and resilience in volatile markets.

- Investments in infrastructure, vertical integration, and ESG practices are driving sustainable competitive advantages, premium market positioning, and stronger long-term profitability.

- Elevated operating risks from high financing costs, commodity price volatility, and climate variability threaten sustainable growth and weaken the long-term land appreciation business model.

Catalysts

About BrasilAgro - Companhia Brasileira de Propriedades Agrícolas- Engages in the acquisition, development, exploration, and sale of agricultural activities in Brazil, Paraguay, and Bolivia.

- Analyst consensus views BrasilAgro's land transformation and sales as a steady driver of value, but the company is now positioned to accelerate this strategy by targeting distressed and highly-leveraged farmland in emerging regions like Maranhão and Piauí, potentially securing land at highly attractive prices just as global arable land scarcity intensifies-setting the stage for greater-than-expected land appreciation and outsized capital gains, directly boosting both earnings and net asset value.

- Analysts broadly expect operational efficiencies to support margin expansion, yet management's disciplined early locking of low fertilizer input prices, aggressive capital discipline, and rapid crop rotation, combined with precision hedging strategies, greatly magnify margin potential in coming seasons, setting the company up for structurally higher net margins even in volatile environments.

- Soaring global demand for grains and animal protein, along with BrasilAgro's strong exposure to both primary crops and cattle, is establishing a compounding revenue base that should enable top-line growth well beyond consensus as emerging markets-especially Asia-lift food and feed imports due to population growth and dietary shifts.

- The company's increasing focus on logistics, storage investments, and vertical integration in Brazil's underdeveloped grain infrastructure can create durable cost advantages and stabilize crop quality, enabling market share gains and improved realized prices, with a direct positive impact on overall profitability and free cash flow conversion.

- The preference of institutional investors and multinational food groups for large, ESG-compliant, professionally managed agricultural assets gives BrasilAgro a strong premium in the capital and commercial markets, supporting premium pricing for land, crops, and joint ventures, while reducing cost of capital and further enhancing long-term return on equity.

BrasilAgro - Companhia Brasileira de Propriedades Agrícolas Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on BrasilAgro - Companhia Brasileira de Propriedades Agrícolas compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming BrasilAgro - Companhia Brasileira de Propriedades Agrícolas's revenue will grow by 3.9% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 25.2% today to 17.7% in 3 years time.

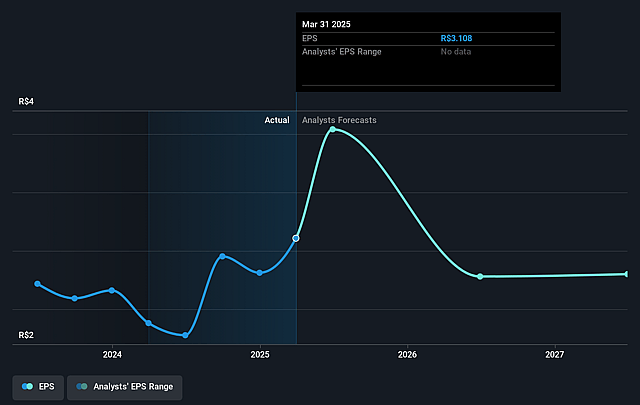

- The bullish analysts expect earnings to reach R$243.6 million (and earnings per share of R$2.46) by about August 2028, down from R$309.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 22.6x on those 2028 earnings, up from 6.6x today. This future PE is greater than the current PE for the US Food industry at 10.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 17.8%, as per the Simply Wall St company report.

BrasilAgro - Companhia Brasileira de Propriedades Agrícolas Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistent high interest rates in Brazil significantly increase the company's cost of capital, which restricts its ability to invest profitably in land acquisition, new projects, and logistics, undermining both net margins and overall earnings growth potential over the long term.

- The company's reliance on volatile commodity crops such as corn, soybeans, and sugarcane means any prolonged weakness or increased competition in global bulk commodity markets could compress its pricing power and revenue streams, leading to reduced earnings visibility and lower net margins.

- Climate variability, as evidenced by excessive rains in some regions and unanticipated droughts in others, consistently impacts crop yields and operational efficiency, potentially leading to higher costs and lower revenue, especially as the effects of climate change deepen over time.

- A potential slowdown or plateau in Brazilian farmland appreciation, which is described as lacking the explosive peaks of recent years, could weaken the core business model of acquiring, improving, and selling agricultural land, thereby slowing asset turnover and decreasing return on equity for shareholders.

- The company's expansion into regions like Maranhao and Piaui increases geographic concentration risk, exposing it to local regulatory, environmental, and logistical challenges that could generate higher volatility in both production output and future revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for BrasilAgro - Companhia Brasileira de Propriedades Agrícolas is R$34.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of BrasilAgro - Companhia Brasileira de Propriedades Agrícolas's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$34.0, and the most bearish reporting a price target of just R$22.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be R$1.4 billion, earnings will come to R$243.6 million, and it would be trading on a PE ratio of 22.6x, assuming you use a discount rate of 17.8%.

- Given the current share price of R$20.57, the bullish analyst price target of R$34.0 is 39.5% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.