Key Takeaways

- Disciplined cost management and proprietary technology are driving margin expansion, operational efficiency, and higher revenue per client as digital engagement accelerates.

- Strong growth in high net worth and adviser channels, supported by deep partnerships and product expansion, underpins sustainable inflows and rising long-term earnings.

- Intensifying competition, regulatory costs, and shifting industry trends threaten Netwealth's margins, revenue growth, and long-term profitability as growth opportunities mature.

Catalysts

About Netwealth Group- A financial services company, engages in the wealth management business in Australia.

- While analyst consensus expects operational expense growth from higher headcount, evidence suggests that Netwealth's disciplined cost management and continued productivity gains-such as delivering a 10.5% productivity delta and maintaining a 50%+ EBITDA margin-could significantly expand EBITDA margins over time, as investments unlock greater operating leverage.

- Analyst consensus projects short-term earnings impact from expanding into new markets and product adjacencies, but current record net flows, rapid account growth across both new and existing customers, and a well-diversified, expanding pipeline indicate a much stronger acceleration in top-line revenue and sustainable growth in assets under administration than currently priced in.

- The accelerating intergenerational transfer of wealth, combined with Netwealth's strong traction in the high net worth and family office segments, positions the company for outsized, multi-year inflows and a structurally higher earnings base as these assets move onto platforms.

- Netwealth's proprietary technology stack, integration of data analytics (including AI-enabled efficiencies and automation), and agile rollout of mobile and trading capabilities are driving superior client engagement and efficiency improvements, setting the stage for margin expansion and higher revenue per client as digital adoption intensifies industry-wide.

- Deep, strengthening partnerships with advisers-supported by integration of practice management solutions like Xeppo and Flux-and the move to capture non-platform and broker-linked assets position Netwealth to realize both higher persistency in flows and materially increase share of wallet, enhancing recurring revenues and long-term earnings growth.

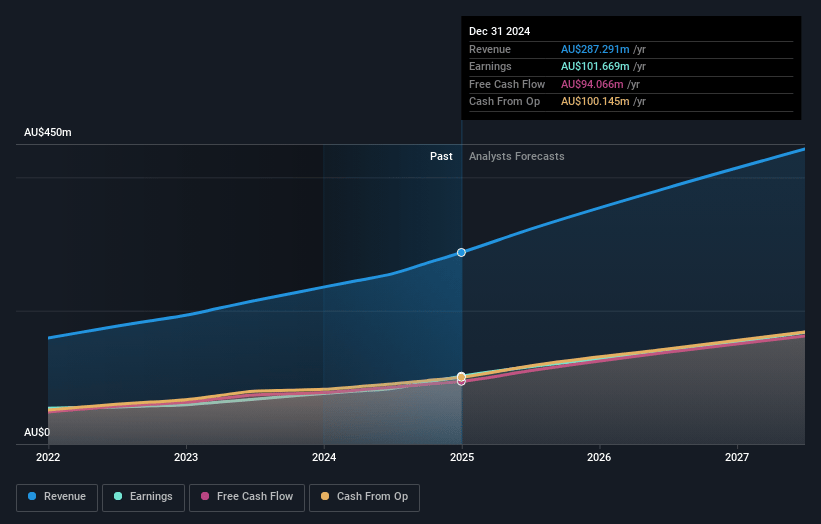

Netwealth Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Netwealth Group compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Netwealth Group's revenue will grow by 24.7% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 35.4% today to 36.7% in 3 years time.

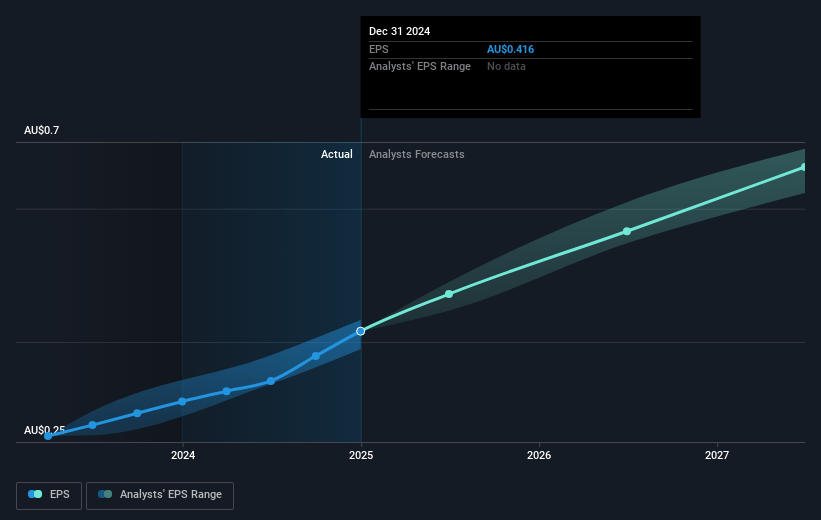

- The bullish analysts expect earnings to reach A$204.6 million (and earnings per share of A$0.83) by about July 2028, up from A$101.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 60.2x on those 2028 earnings, down from 88.5x today. This future PE is greater than the current PE for the AU Capital Markets industry at 15.5x.

- Analysts expect the number of shares outstanding to grow by 0.31% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.59%, as per the Simply Wall St company report.

Netwealth Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The wealth management industry is facing sustained pricing and margin pressure due to increasing competition from both large incumbents and new entrants, with management indicating current and future pricing flexibility to absorb market pressure; this trend risks eroding Netwealth's net profit margins over time.

- The rise of passive investing, direct indexing, and decentralized finance threatens to diminish long-term demand for traditional platform services, potentially capping future net inflows and impacting the company's revenue growth trajectory.

- Ongoing regulatory scrutiny and the need for regular compliance uplifts are elevating operating costs, which, together with the requirement to remain transparent and adapt to shifting regulations, could compress operating margins and reduce overall earnings quality.

- The need for accelerated investment in technology and headcount to remain competitive in product, functionality, and distribution may drive sustained higher operating expenses, particularly as technology cycles shorten and failure to keep pace could result in costly obsolescence, negatively impacting net margins and long-term profitability.

- Market saturation and potential brand fatigue among advisers and clients, highlighted by the heavy reliance on existing mature customers for inflows, suggest that organic growth could slow as the business matures, directly constraining the future expansion of fee revenue and recurring income.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Netwealth Group is A$40.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Netwealth Group's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$40.0, and the most bearish reporting a price target of just A$12.3.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be A$557.3 million, earnings will come to A$204.6 million, and it would be trading on a PE ratio of 60.2x, assuming you use a discount rate of 7.6%.

- Given the current share price of A$36.74, the bullish analyst price target of A$40.0 is 8.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.