Key Takeaways

- Regulatory pressures and shifts toward in-house lottery distribution may undermine revenue growth and threaten Jumbo's existing business model.

- Aging customer demographics and increased competition could further constrain future market potential and compress profit margins.

- Diversification into global SaaS and charity lottery markets, digital growth, and strong cost control enhance Jumbo Interactive's revenue stability, margins, and resilience against jackpot volatility.

Catalysts

About Jumbo Interactive- Engages in the retail of lottery tickets through the internet and mobile devices in Australia, the United Kingdom, Canada, Fiji, and internationally.

- A sustained increase in regulatory scrutiny on online gambling and lottery operations worldwide threatens to restrict market access and growth potential for Jumbo Interactive, which could cause long-term pressure on revenue expansion and international earnings diversification.

- Intensifying concerns about responsible gambling, particularly as governments and advocacy groups push for tighter controls, may suppress lottery participation and reduce ticket sales, impacting both revenue growth and customer acquisition rates in future years.

- Younger generations are exhibiting declining interest in lottery products and shifting entertainment preferences; as Jumbo's customer base ages and digital penetration plateaus, the long-term addressable market may shrink and reduce top-line revenue potential over time.

- Heightened competition from emerging digital lottery platforms and international operators increases the risk of market share erosion and compresses revenue growth, especially as acquisition costs rise and Jumbo is forced to spend more on marketing to simply maintain share, placing sustained downward pressure on margins.

- Lottery regulators may increasingly bypass third-party distributors by bringing more ticket sales in-house, which would severely undermine Jumbo's business model and threaten both recurring revenues and net margins as key state contracts become vulnerable to non-renewal or adverse renegotiation.

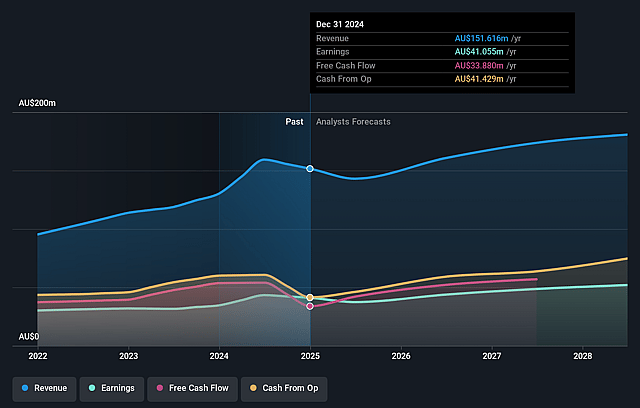

Jumbo Interactive Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Jumbo Interactive compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Jumbo Interactive's revenue will grow by 4.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 27.3% today to 25.0% in 3 years time.

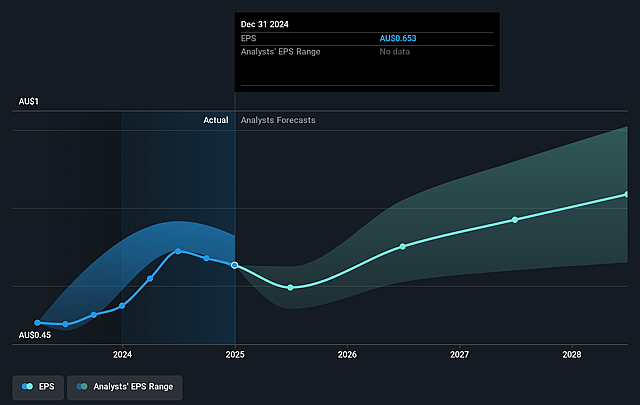

- The bearish analysts expect earnings to reach A$42.4 million (and earnings per share of A$0.7) by about September 2028, up from A$40.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 16.3x on those 2028 earnings, down from 17.7x today. This future PE is lower than the current PE for the AU Hospitality industry at 35.2x.

- Analysts expect the number of shares outstanding to decline by 0.43% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.97%, as per the Simply Wall St company report.

Jumbo Interactive Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rapid digitalisation and increased digital penetration continue to raise overall online lottery engagement, with digital penetration reaching nearly 42% and trending higher, which should expand Jumbo Interactive's user base and drive recurring revenue growth over the long term.

- The company's ability to adapt quickly to jackpots cycles and mean reversion expectations, as well as the historical tendency for higher jackpots to follow subdued years, positions Jumbo to benefit from future rebound periods and lift both revenue and earnings.

- Diversification into SaaS offerings, charity lotteries, proprietary products, and managed services across international markets provides new, less cyclical, and higher-margin revenue streams, reducing reliance on volatile Australian jackpot cycles and supporting healthier net margins.

- Robust cost control, consistently high cash conversion over 100%, a strong balance sheet, and a track record of returning capital to shareholders through buybacks and record dividends provide resilience and flexibility for sustained earnings growth.

- Continued investment in data analytics, a multipronged marketing playbook, and customer loyalty programs like Daily Winners drive increased player quality, retention, and lifetime value, underpinning stable or rising top-line revenue and improved profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Jumbo Interactive is A$9.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Jumbo Interactive's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$15.2, and the most bearish reporting a price target of just A$9.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be A$169.6 million, earnings will come to A$42.4 million, and it would be trading on a PE ratio of 16.3x, assuming you use a discount rate of 8.0%.

- Given the current share price of A$11.4, the bearish analyst price target of A$9.0 is 26.7% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.