Last Update04 Aug 25Fair value Decreased 6.86%

The downward revision in Flight Centre Travel Group’s consensus price target is primarily driven by reduced revenue growth forecasts and a slight decline in net profit margins, lowering fair value from A$16.76 to A$15.67.

What's in the News

- Flight Centre Travel Group renewed its technology partnership with Serko Limited, continuing to market and distribute Serko's online booking solutions.

- FCTG will contribute to a development fund focused on creating unique product features for its customers.

- FCTG represents a significant portion of Serko's booking volume in Australia and New Zealand for managed travel.

Valuation Changes

Summary of Valuation Changes for Flight Centre Travel Group

- The Consensus Analyst Price Target has fallen from A$16.76 to A$15.67.

- The Consensus Revenue Growth forecasts for Flight Centre Travel Group has significantly fallen from 5.8% per annum to 5.1% per annum.

- The Net Profit Margin for Flight Centre Travel Group has fallen slightly from 9.86% to 9.53%.

Key Takeaways

- Investments in high-margin luxury and cruising sectors aim to enhance revenue and strengthen market position in profitable segments.

- Implementation of AI and automation is expected to boost productivity, enhance cost efficiency, and improve net margins.

- Reliance on luxury travel amid deflation and fierce competition may risk earnings if spending shifts or targets aren't met, impacting margins and shareholder confidence.

Catalysts

About Flight Centre Travel Group- Provides travel retailing services for the leisure and corporate sectors in Australia, New Zealand, the Americas, Europe, the Middle East, Africa, Asia, and internationally.

- Flight Centre Travel Group is focusing on TTV growth, particularly in higher-margin businesses such as Corporate Traveler and Flight Centre, which is expected to lead to stronger revenues.

- The company is investing in luxury and cruising segments, including strategic investments in the Cruiseabout expansion and the new Explorations cruise line, aiming to enhance revenue streams and margins in those higher-margin sectors.

- Productivity and cost efficiency improvements are anticipated through the implementation of a single global operating system for corporate brands and the application of AI and automation, likely improving net margins.

- Expanding the global corporate market share with significant new account wins, such as the $800 million in new business for FCM, is expected to boost revenue and profitability in the corporate division.

- The ongoing expansion of online channels and independent agency networks is expected to provide scalable growth opportunities with a lower cost base, improving overall earnings.

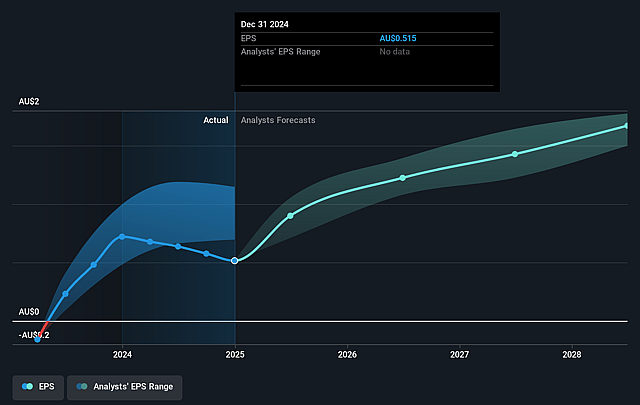

Flight Centre Travel Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Flight Centre Travel Group's revenue will grow by 5.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.1% today to 9.5% in 3 years time.

- Analysts expect earnings to reach A$303.6 million (and earnings per share of A$1.45) by about August 2028, up from A$113.5 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as A$222 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.5x on those 2028 earnings, down from 24.3x today. This future PE is lower than the current PE for the AU Hospitality industry at 32.3x.

- Analysts expect the number of shares outstanding to grow by 0.55% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.72%, as per the Simply Wall St company report.

Flight Centre Travel Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The market for airfares has been experiencing deflation in some regions, which has impacted super overrides and profit margins. A continued decline in airfare prices could pressure revenue margins further.

- High provisions for doubtful debts and system changes affected results in Asia, impacting corporate profitability. Continued issues in Asia could weigh on future earnings if not resolved effectively.

- The increase in competition and strategic investments necessary for expansion in the cruise and touring sectors imply cost pressures. If revenues don't scale with these investments, net margins could be adversely affected.

- The reliance on high-margin luxury travel and specialist divisions for substantial profit contribution entails risk if consumer behavior shifts or economic conditions impact discretionary spending, potentially affecting earnings.

- Execution risk due to ambitious growth and productivity targets, including achieving a 2% profit margin, poses a challenge. Failure to realize these targets could lead to disappointing earnings and affect shareholder confidence.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$15.613 for Flight Centre Travel Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$20.75, and the most bearish reporting a price target of just A$12.25.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$3.2 billion, earnings will come to A$303.6 million, and it would be trading on a PE ratio of 14.5x, assuming you use a discount rate of 8.7%.

- Given the current share price of A$12.74, the analyst price target of A$15.61 is 18.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.