Key Takeaways

- Prolonged industry headwinds and digital disruption threaten Reece's market share, pricing power, and top-line revenue across its core geographies.

- Complex U.S. expansion, elevated debt, and persistent supply chain challenges risk prolonged margin pressure and unstable long-term profitability.

- Strategic investments, digital innovation, and expanding scale position Reece to capitalize on structural growth drivers, enhance operational efficiency, and increase market share in key markets.

Catalysts

About Reece- Engages in the distribution of plumbing, bathroom, heating, ventilation, air-conditioning, waterworks, and refrigeration products to commercial and residential customers in Australia, the United States, and New Zealand.

- Prolonged high interest rates and persistent inflation are expected to dampen new construction and renovation activity in both the U.S. and ANZ, directly suppressing demand for plumbing and HVAC supplies and risking further declines in Reece's top-line revenue for several years.

- The shift toward digital direct-to-contractor platforms by manufacturers is likely to accelerate, which could bypass traditional distributors like Reece, progressively eroding pricing power and market share, and putting long-term downward pressure on both revenue and net margins.

- The ongoing expansion into the fragmented U.S. market is introducing significant operational complexity and integration risk, which, if not managed flawlessly, will drive cost overruns and continue to dilute margins, ultimately hurting future earnings growth and delaying return on investment from new branches.

- Increased leverage from acquisition-led growth combined with rising gross interest expense, currently anticipated at up to $63 million for the full year, creates exposure to refinancing risk if earnings before interest, tax, depreciation, and amortization (EBITDA) do not recover, threatening both net profit and free cash flow stability in the long term.

- Persistent supply chain disruptions-intensified by global material shortages and potential tariff changes-will inflate procurement costs and create ongoing margin compression, further undermining the company's ability to achieve sustainable profitability and consistent earnings growth.

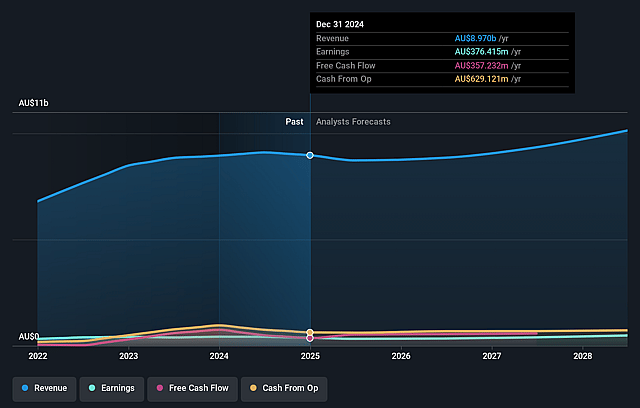

Reece Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Reece compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Reece's revenue will grow by 3.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 4.2% today to 4.3% in 3 years time.

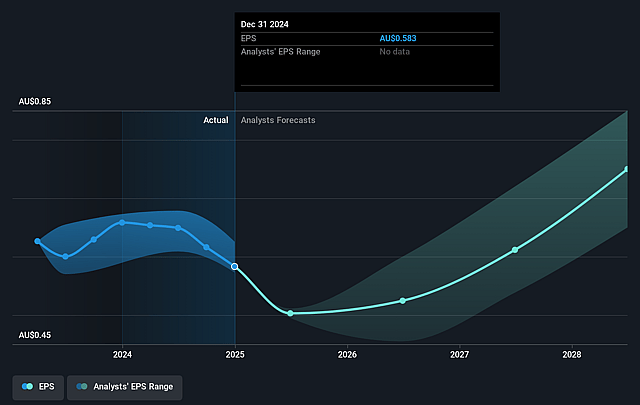

- The bearish analysts expect earnings to reach A$419.9 million (and earnings per share of A$0.65) by about August 2028, up from A$376.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 24.1x on those 2028 earnings, down from 25.6x today. This future PE is greater than the current PE for the AU Trade Distributors industry at 20.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.87%, as per the Simply Wall St company report.

Reece Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Reece continues to invest through the cycle with a focus on long-term growth, including expanding its branch network domestically and in the US, ongoing digital innovation initiatives, and investments in operational excellence-all of which could drive sustained revenue and earnings growth and support higher long-term returns.

- The company's strong balance sheet with sufficient capacity for further organic and inorganic growth, along with a disciplined capital management strategy, positions Reece to weather downturns and capitalize on market recovery, which could help preserve or improve net margins and enable continued shareholder returns.

- Exposure to long-term secular trends such as urbanization, population growth, and ongoing underbuild in housing and infrastructure demand across Australia, New Zealand, and the US provides a structural tailwind for the business, supporting a larger addressable market and growth in sales and earnings.

- Emphasis on innovation, private label expansion, improved digital capabilities, and omni-channel customer experiences positions Reece to gain market share as the trade distribution sector undergoes digital transformation, potentially driving higher operational efficiency and gross margins.

- Continued industry consolidation and the company's growing scale, especially in the fragmented US market, could lead to strengthened pricing power, greater supplier relationships, and enhanced market share, supporting higher revenues and enabling margin expansion over the long-term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Reece is A$12.5, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Reece's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$19.9, and the most bearish reporting a price target of just A$12.5.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be A$9.9 billion, earnings will come to A$419.9 million, and it would be trading on a PE ratio of 24.1x, assuming you use a discount rate of 7.9%.

- Given the current share price of A$14.93, the bearish analyst price target of A$12.5 is 19.4% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Reece?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.