Advertisement

We Think Some Shareholders May Hesitate To Increase Woolworths Holdings Limited's (JSE:WHL) CEO Compensation

Key Insights

- Woolworths Holdings to hold its Annual General Meeting on 22nd of November

- CEO Roy Bagattini's total compensation includes salary of R18.2m

- The total compensation is 56% higher than the average for the industry

- Woolworths Holdings' EPS grew by 95% over the past three years while total shareholder return over the past three years was 89%

Under the guidance of CEO Roy Bagattini, Woolworths Holdings Limited (JSE:WHL) has performed reasonably well recently. As shareholders go into the upcoming AGM on 22nd of November, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders will still be cautious of paying the CEO excessively.

Check out our latest analysis for Woolworths Holdings

Comparing Woolworths Holdings Limited's CEO Compensation With The Industry

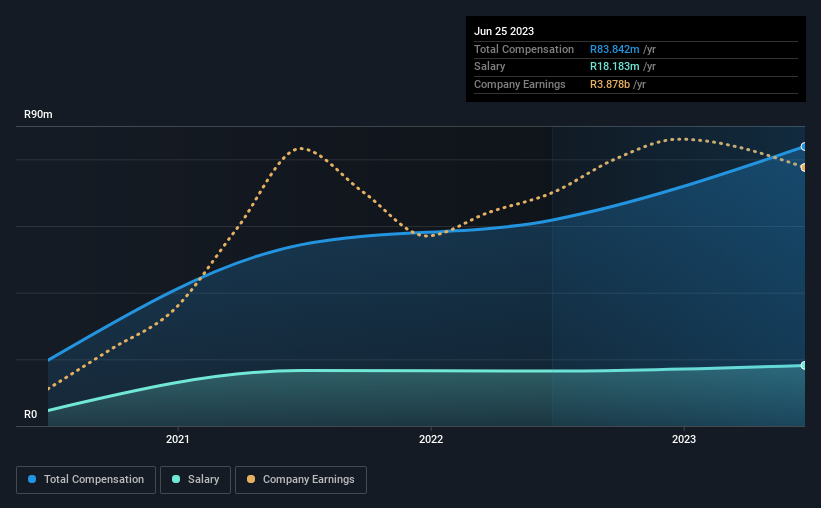

Our data indicates that Woolworths Holdings Limited has a market capitalization of R63b, and total annual CEO compensation was reported as R84m for the year to June 2023. We note that's an increase of 36% above last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at R18m.

For comparison, other companies in the South Africa Multiline Retail industry with market capitalizations ranging between R36b and R117b had a median total CEO compensation of R54m. Accordingly, our analysis reveals that Woolworths Holdings Limited pays Roy Bagattini north of the industry median. What's more, Roy Bagattini holds R176m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | R18m | R16m | 22% |

| Other | R66m | R45m | 78% |

| Total Compensation | R84m | R62m | 100% |

Talking in terms of the industry, salary represented approximately 49% of total compensation out of all the companies we analyzed, while other remuneration made up 51% of the pie. In Woolworths Holdings' case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

A Look at Woolworths Holdings Limited's Growth Numbers

Woolworths Holdings Limited has seen its earnings per share (EPS) increase by 95% a year over the past three years. In the last year, its revenue is up 10%.

Shareholders would be glad to know that the company has improved itself over the last few years. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Woolworths Holdings Limited Been A Good Investment?

Most shareholders would probably be pleased with Woolworths Holdings Limited for providing a total return of 89% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 1 warning sign for Woolworths Holdings that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Woolworths Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:WHL

Woolworths Holdings

Through its subsidiaries, operates a chain of retail stores in South Africa, Australia, and New Zealand.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative