- South Africa

- /

- Capital Markets

- /

- JSE:VUN

Why It Might Not Make Sense To Buy Vunani Limited (JSE:VUN) For Its Upcoming Dividend

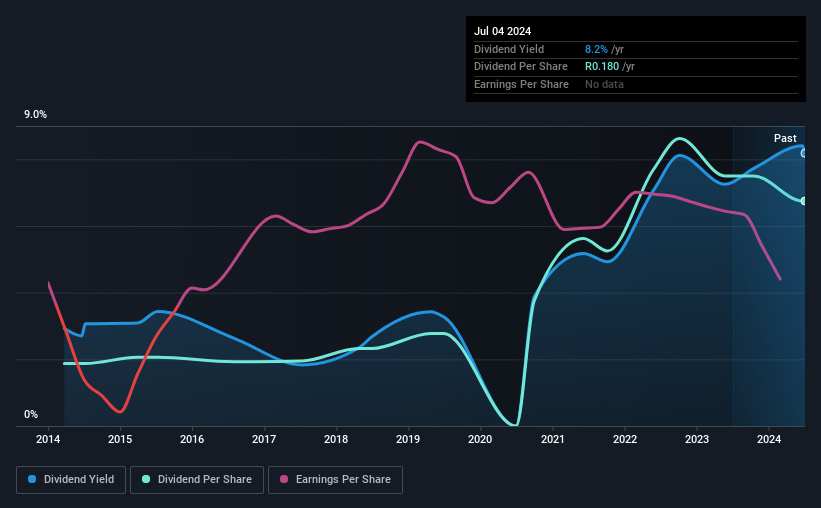

Vunani Limited (JSE:VUN) stock is about to trade ex-dividend in four days. Typically, the ex-dividend date is one business day before the record date which is the date on which a company determines the shareholders eligible to receive a dividend. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. Thus, you can purchase Vunani's shares before the 10th of July in order to receive the dividend, which the company will pay on the 15th of July.

The company's next dividend payment will be R00.09 per share. Last year, in total, the company distributed R0.18 to shareholders. Based on the last year's worth of payments, Vunani has a trailing yield of 8.2% on the current stock price of R02.20. If you buy this business for its dividend, you should have an idea of whether Vunani's dividend is reliable and sustainable. So we need to investigate whether Vunani can afford its dividend, and if the dividend could grow.

See our latest analysis for Vunani

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Vunani distributed an unsustainably high 200% of its profit as dividends to shareholders last year. Without more sustainable payment behaviour, the dividend looks precarious.

Generally, the higher a company's payout ratio, the more the dividend is at risk of being reduced.

Click here to see how much of its profit Vunani paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Vunani's earnings have collapsed faster than Wile E Coyote's schemes to trap the Road Runner; down a tremendous 30% a year over the past five years.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the past 10 years, Vunani has increased its dividend at approximately 14% a year on average. The only way to pay higher dividends when earnings are shrinking is either to pay out a larger percentage of profits, spend cash from the balance sheet, or borrow the money. Vunani is already paying out 200% of its profits, and with shrinking earnings we think it's unlikely that this dividend will grow quickly in the future.

The Bottom Line

Has Vunani got what it takes to maintain its dividend payments? Earnings per share are in decline and Vunani is paying out what we feel is an uncomfortably high percentage of its profit as dividends. Generally we think dividend investors should avoid businesses in this situation, as high payout ratios and declining earnings can lead to the dividend being cut. These characteristics don't generally lead to outstanding dividend performance, and investors may not be happy with the results of owning this stock for its dividend.

With that being said, if you're still considering Vunani as an investment, you'll find it beneficial to know what risks this stock is facing. To that end, you should learn about the 6 warning signs we've spotted with Vunani (including 2 which are a bit unpleasant).

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About JSE:VUN

Excellent balance sheet with slight risk.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion