Advertisement

- South Africa

- /

- Industrials

- /

- JSE:KAP

We Think KAP Industrial Holdings (JSE:KAP) Is Taking Some Risk With Its Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that KAP Industrial Holdings Limited (JSE:KAP) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for KAP Industrial Holdings

What Is KAP Industrial Holdings's Debt?

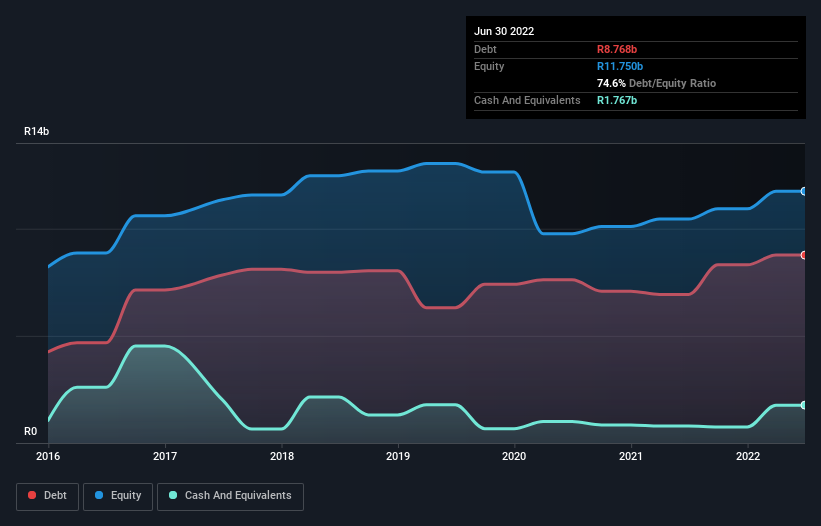

You can click the graphic below for the historical numbers, but it shows that as of June 2022 KAP Industrial Holdings had R8.77b of debt, an increase on R6.93b, over one year. On the flip side, it has R1.77b in cash leading to net debt of about R7.00b.

How Strong Is KAP Industrial Holdings' Balance Sheet?

The latest balance sheet data shows that KAP Industrial Holdings had liabilities of R7.99b due within a year, and liabilities of R9.77b falling due after that. Offsetting this, it had R1.77b in cash and R4.46b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by R11.5b.

Given this deficit is actually higher than the company's market capitalization of R11.4b, we think shareholders really should watch KAP Industrial Holdings's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

KAP Industrial Holdings's net debt is sitting at a very reasonable 1.7 times its EBITDA, while its EBIT covered its interest expense just 5.6 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. It is well worth noting that KAP Industrial Holdings's EBIT shot up like bamboo after rain, gaining 33% in the last twelve months. That'll make it easier to manage its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine KAP Industrial Holdings's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, KAP Industrial Holdings recorded negative free cash flow, in total. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

KAP Industrial Holdings's conversion of EBIT to free cash flow and level of total liabilities definitely weigh on it, in our esteem. But the good news is it seems to be able to grow its EBIT with ease. When we consider all the factors discussed, it seems to us that KAP Industrial Holdings is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for KAP Industrial Holdings you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if KAP might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:KAP

KAP

Engages in industrial, chemical, and logistics businesses in South Africa, rest of Africa, the Americas, Europe, the Middle East, and Australasia.

Very undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor