Advertisement

- United States

- /

- Other Utilities

- /

- NYSE:WEC

WEC Energy Group (WEC): Evaluating Valuation After Strong Q3 Results and Major Capital-Raising Moves

Simply Wall St

Reviewed by Simply Wall St

WEC Energy Group (WEC) has been in the spotlight after beating analysts’ expectations on both earnings and revenue for the third quarter. The company also unveiled major capital-raising efforts, which signals confidence for the road ahead.

See our latest analysis for WEC Energy Group.

The third quarter's upbeat results and capital-raising moves have caught investors’ attention, but momentum has actually been building for a while. WEC Energy Group posted an 18.7% share price return year-to-date and a total shareholder return of 16.5% over the past year. Combined with recent updates, that suggests investors are recognizing both the company’s earnings progress and its growth potential heading into next year.

If strong utility sector momentum has you curious, this could be a perfect moment to discover fast growing stocks with high insider ownership

As valuations climb and the company’s outlook brightens, investors may wonder whether there is still untapped value in WEC Energy Group, or if the current share price fully reflects its growth prospects.

Most Popular Narrative: 9% Undervalued

WEC Energy Group’s most popular narrative places its fair value at $122.62, a notable premium over the stock’s last close at $111.60. Market participants are dissecting whether this difference can be maintained as earnings power and sector policy tailwinds play out.

Surging power demand and grid modernization efforts position WEC for sustained top-line and earnings growth, supported by infrastructure investments and a favorable regulatory environment. Accelerated investment in renewables and battery storage secures long-term benefits from the energy transition and strengthens regulated earnings as decarbonization intensifies.

Wondering what’s driving this bullish valuation? The narrative is built on bold growth forecasts and profit margins that rival industry leaders. Curious which financial assumptions are shifting the fair value? Get the full picture. One surprising variable could define WEC’s future upside.

Result: Fair Value of $122.62 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising financing costs and regulatory uncertainties could quickly challenge WEC Energy Group’s growth story. This is especially true if key approvals or market trends shift unexpectedly.

Find out about the key risks to this WEC Energy Group narrative.

Another View: Looking at Valuation Multiples

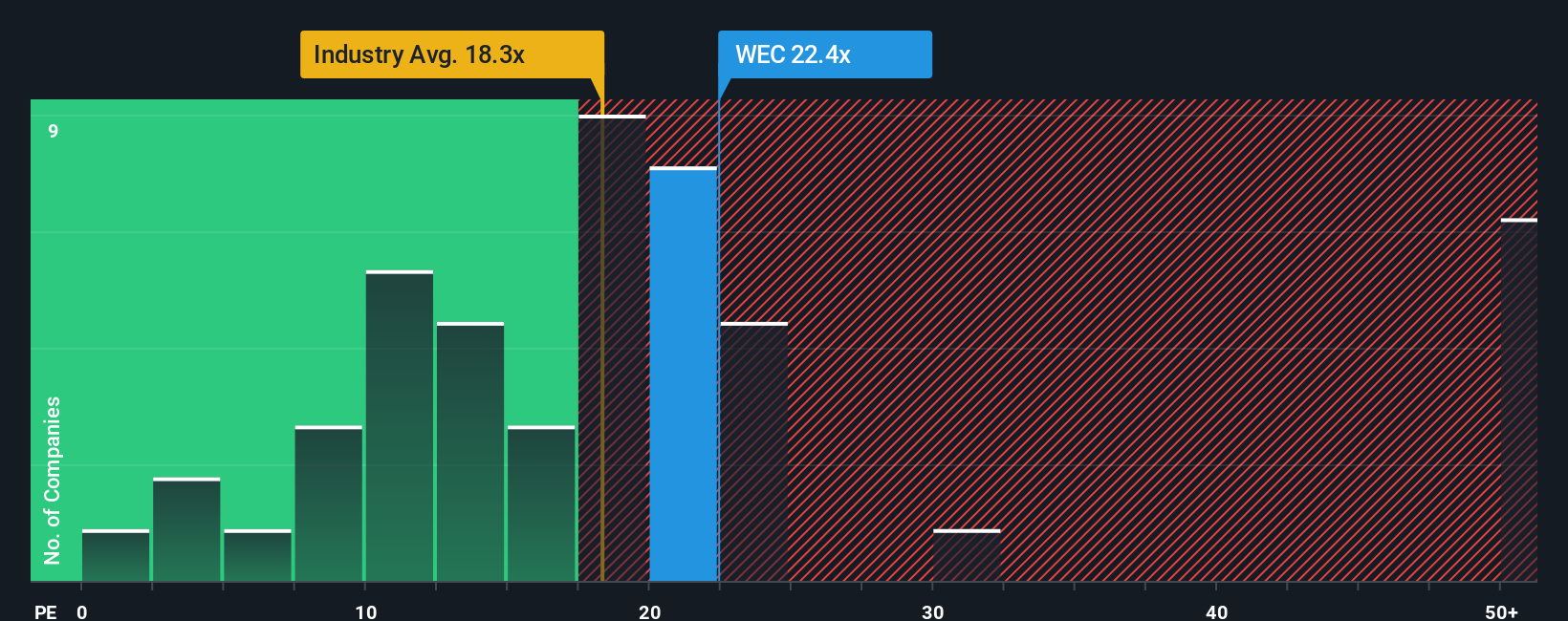

Despite the fair value narrative painting WEC Energy Group as undervalued, the price-to-earnings ratio tells a different story. WEC trades at 21.4 times earnings, which is pricier than both its industry peers at 20.8x and the global sector average of 18.4x. In fact, this closely matches its fair ratio of 21.4x, so there may not be much of a valuation buffer if performance wavers. If the market’s mood shifts, could the premium vanish?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own WEC Energy Group Narrative

If you see things differently or want to dig into the numbers yourself, you can shape your own take in just a few minutes. Do it your way

A great starting point for your WEC Energy Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Expand your watchlist with stocks that have real momentum and growth potential. Miss this and you could be leaving tomorrow’s market leaders behind.

- Capture the opportunity for consistent income by checking out these 18 dividend stocks with yields > 3% offering yields above 3% and robust dividend histories.

- Ride the wave of innovation and see which players are defining the future in artificial intelligence by reviewing these 27 AI penny stocks.

- Tap into undervalued gems by browsing these 906 undervalued stocks based on cash flows built on strong cash flow fundamentals and overlooked upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if WEC Energy Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WEC

WEC Energy Group

Through its subsidiaries, provides regulated natural gas and electricity, and renewable and nonregulated renewable energy services in the United States.

Solid track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor