Advertisement

- United States

- /

- Other Utilities

- /

- NYSE:WEC

WEC Energy Group (NYSE:WEC) Is Paying Out A Larger Dividend Than Last Year

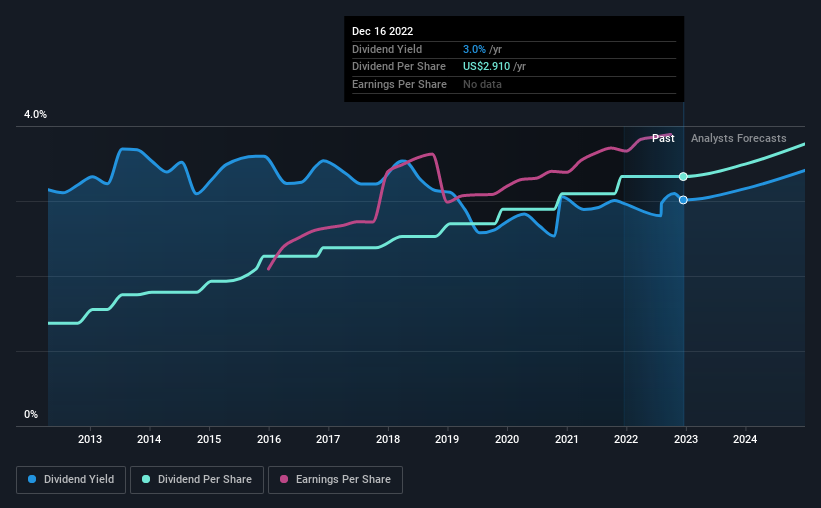

WEC Energy Group, Inc. (NYSE:WEC) has announced that it will be increasing its periodic dividend on the 1st of March to $0.78, which will be 7.2% higher than last year's comparable payment amount of $0.728. The payment will take the dividend yield to 3.0%, which is in line with the average for the industry.

View our latest analysis for WEC Energy Group

WEC Energy Group's Earnings Easily Cover The Distributions

Unless the payments are sustainable, the dividend yield doesn't mean too much. Prior to this announcement, WEC Energy Group's earnings easily covered the dividend, but free cash flows were negative. No cash flows could definitely make returning cash to shareholders difficult, or at least mean the balance sheet will come under pressure.

The next year is set to see EPS grow by 18.2%. If the dividend continues on this path, the payout ratio could be 61% by next year, which we think can be pretty sustainable going forward.

WEC Energy Group Has A Solid Track Record

The company has an extended history of paying stable dividends. The annual payment during the last 10 years was $1.20 in 2012, and the most recent fiscal year payment was $2.91. This implies that the company grew its distributions at a yearly rate of about 9.3% over that duration. The growth of the dividend has been pretty reliable, so we think this can offer investors some nice additional income in their portfolio.

WEC Energy Group Could Grow Its Dividend

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. WEC Energy Group has impressed us by growing EPS at 7.4% per year over the past five years. The company is paying out a lot of its cash as a dividend, but it looks okay based on the payout ratio.

Our Thoughts On WEC Energy Group's Dividend

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've identified 3 warning signs for WEC Energy Group (1 is a bit unpleasant!) that you should be aware of before investing. Is WEC Energy Group not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if WEC Energy Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WEC

WEC Energy Group

Through its subsidiaries, provides regulated natural gas and electricity, and renewable and nonregulated renewable energy services in the United States.

Solid track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|21.5% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|7.6% overvalued

TO

Community Contributor