- United States

- /

- Other Utilities

- /

- NYSE:WEC

We Wouldn't Be Too Quick To Buy WEC Energy Group, Inc. (NYSE:WEC) Before It Goes Ex-Dividend

It looks like WEC Energy Group, Inc. (NYSE:WEC) is about to go ex-dividend in the next four days. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. This means that investors who purchase WEC Energy Group's shares on or after the 14th of November will not receive the dividend, which will be paid on the 1st of December.

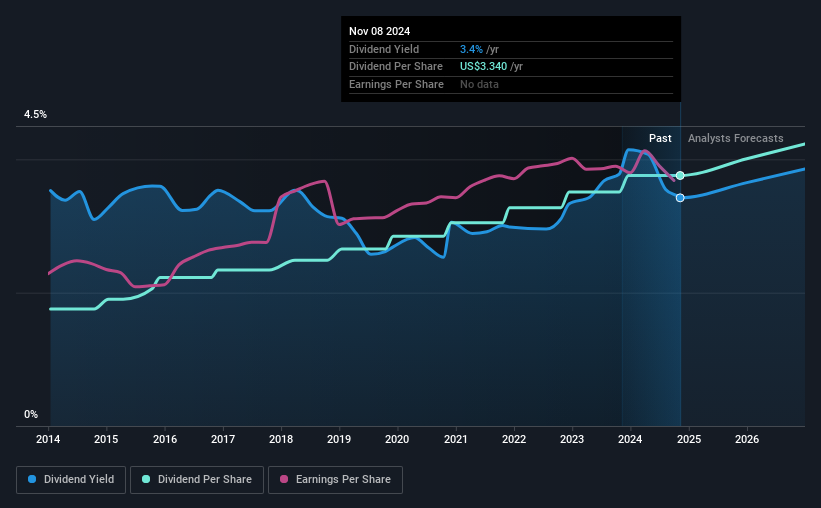

The company's next dividend payment will be US$0.835 per share, and in the last 12 months, the company paid a total of US$3.34 per share. Based on the last year's worth of payments, WEC Energy Group stock has a trailing yield of around 3.4% on the current share price of US$97.59. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to investigate whether WEC Energy Group can afford its dividend, and if the dividend could grow.

Check out our latest analysis for WEC Energy Group

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Its dividend payout ratio is 80% of profit, which means the company is paying out a majority of its earnings. The relatively limited profit reinvestment could slow the rate of future earnings growth. We'd be concerned if earnings began to decline. A useful secondary check can be to evaluate whether WEC Energy Group generated enough free cash flow to afford its dividend. Over the last year, it paid out dividends equivalent to 252% of what it generated in free cash flow, a disturbingly high percentage. It's pretty hard to pay out more than you earn, so we wonder how WEC Energy Group intends to continue funding this dividend, or if it could be forced to cut the payment.

While WEC Energy Group's dividends were covered by the company's reported profits, cash is somewhat more important, so it's not great to see that the company didn't generate enough cash to pay its dividend. Cash is king, as they say, and were WEC Energy Group to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. With that in mind, we're encouraged by the steady growth at WEC Energy Group, with earnings per share up 4.0% on average over the last five years. Earnings have been growing somewhat, but we're concerned dividend payments consumed most of the company's cash flow over the past year.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. WEC Energy Group has delivered 7.9% dividend growth per year on average over the past 10 years. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

Final Takeaway

Should investors buy WEC Energy Group for the upcoming dividend? Earnings per share have grown somewhat, although WEC Energy Group paid out over half its profits and the dividend was not well covered by free cash flow. Bottom line: WEC Energy Group has some unfortunate characteristics that we think could lead to sub-optimal outcomes for dividend investors.

With that in mind though, if the poor dividend characteristics of WEC Energy Group don't faze you, it's worth being mindful of the risks involved with this business. For instance, we've identified 2 warning signs for WEC Energy Group (1 makes us a bit uncomfortable) you should be aware of.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if WEC Energy Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WEC

WEC Energy Group

Through its subsidiaries, provides regulated natural gas and electricity, and renewable and nonregulated renewable energy services in the United States.

Average dividend payer with acceptable track record.