- United States

- /

- Water Utilities

- /

- NasdaqGS:HTO

Here's Why Shareholders May Want To Be Cautious With Increasing SJW Group's (NYSE:SJW) CEO Pay Packet

Key Insights

- SJW Group will host its Annual General Meeting on 20th of June

- Total pay for CEO Eric Thornburg includes US$874.0k salary

- The total compensation is 1,441% higher than the average for the industry

- Over the past three years, SJW Group's EPS grew by 7.0% and over the past three years, the total loss to shareholders 17%

The underwhelming share price performance of SJW Group (NYSE:SJW) in the past three years would have disappointed many shareholders. However, what is unusual is that EPS growth has been positive, suggesting that the share price has diverged from fundamentals. The AGM coming up on the 20th of June could be an opportunity for shareholders to bring these concerns to the board's attention. They could also influence management through voting on resolutions such as executive remuneration. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

View our latest analysis for SJW Group

How Does Total Compensation For Eric Thornburg Compare With Other Companies In The Industry?

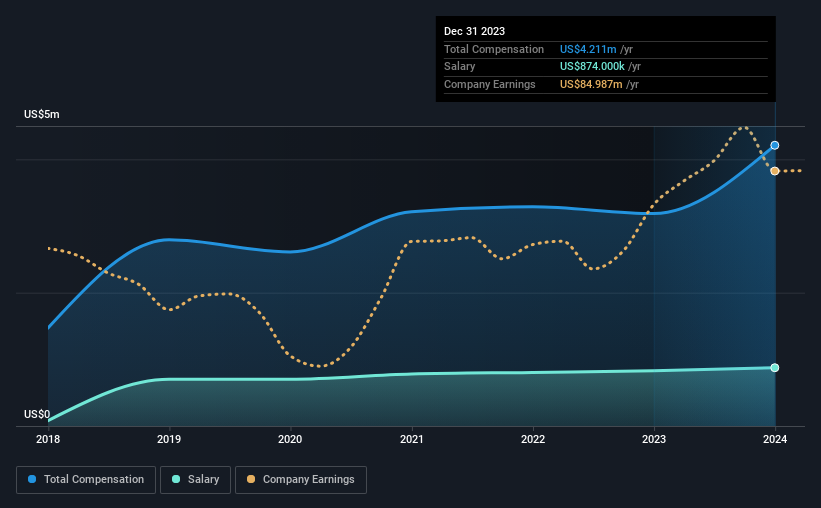

Our data indicates that SJW Group has a market capitalization of US$1.7b, and total annual CEO compensation was reported as US$4.2m for the year to December 2023. Notably, that's an increase of 32% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at US$874k.

On comparing similar companies from the American Water Utilities industry with market caps ranging from US$1.0b to US$3.2b, we found that the median CEO total compensation was US$273k. Accordingly, our analysis reveals that SJW Group pays Eric Thornburg north of the industry median. Moreover, Eric Thornburg also holds US$2.4m worth of SJW Group stock directly under their own name.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$874k | US$828k | 21% |

| Other | US$3.3m | US$2.4m | 79% |

| Total Compensation | US$4.2m | US$3.2m | 100% |

On an industry level, around 38% of total compensation represents salary and 62% is other remuneration. SJW Group sets aside a smaller share of compensation for salary, in comparison to the overall industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

SJW Group's Growth

Over the past three years, SJW Group has seen its earnings per share (EPS) grow by 7.0% per year. It achieved revenue growth of 7.7% over the last year.

We're not particularly impressed by the revenue growth, but it is good to see modest EPS growth. It's clear the performance has been quite decent, but it it falls short of outstanding,based on this information. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has SJW Group Been A Good Investment?

With a three year total loss of 17% for the shareholders, SJW Group would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Shareholders have not seen their shares grow in value, rather they have seen their shares decline. The fact that the stock price hasn't grown along with earnings may indicate that other issues may be affecting that stock. Shareholders would probably be keen to find out what are the other factors could be weighing down the stock. At the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. That's why we did our research, and identified 3 warning signs for SJW Group (of which 1 is concerning!) that you should know about in order to have a holistic understanding of the stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if H2O America might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HTO

H2O America

Through its subsidiaries, provides water utility and other related services in the United States.

Solid track record average dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion