Advertisement

- United States

- /

- Other Utilities

- /

- NYSE:NI

Will NiSource's (NI) $852 Million Equity Raise and Shelf Registration Reshape Its Investment Story?

Simply Wall St

Reviewed by Sasha Jovanovic

- In late October 2025, NiSource Inc. completed a follow-on equity offering raising approximately US$852.5 million and filed a shelf registration to potentially issue up to US$1.5 billion in additional securities across multiple types, including common stock and debt.

- The combination of these substantial capital market activities allowed NiSource to quickly access significant funding flexibility, signaling a shift in the company’s financial structure and future growth opportunities.

- We’ll consider how this sizeable equity raising and expanded shelf registration could alter NiSource’s investment narrative, particularly around dilution and capital deployment.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

NiSource Investment Narrative Recap

To be a shareholder in NiSource today, you need to believe that sustained demand for regulated electric and gas infrastructure investments will outweigh both regulatory and decarbonization challenges. The recent equity raise and expanded shelf registration have provided substantial financial flexibility, but for now, the most important near-term catalyst, regulatory approval for major projects, remains unchanged, while the biggest risk of long-term gas demand erosion due to electrification trends persists and has not been materially altered by this news.

Of the recent announcements, NiSource’s updated 2026 EPS guidance of US$2.02 to US$2.07 stands out, as it provides a current snapshot of the company’s earnings outlook. This target helps investors gauge whether recent capital raises, which may introduce short-term dilution, are supporting long-term project returns and the drivers for future growth or simply offsetting the pressures of high capital requirements.

But with capital needs still high and electrification trends accelerating, investors should be aware that…

Read the full narrative on NiSource (it's free!)

NiSource's narrative projects $6.8 billion revenue and $1.1 billion earnings by 2028. This requires 3.5% yearly revenue growth and a $215 million earnings increase from $884.6 million.

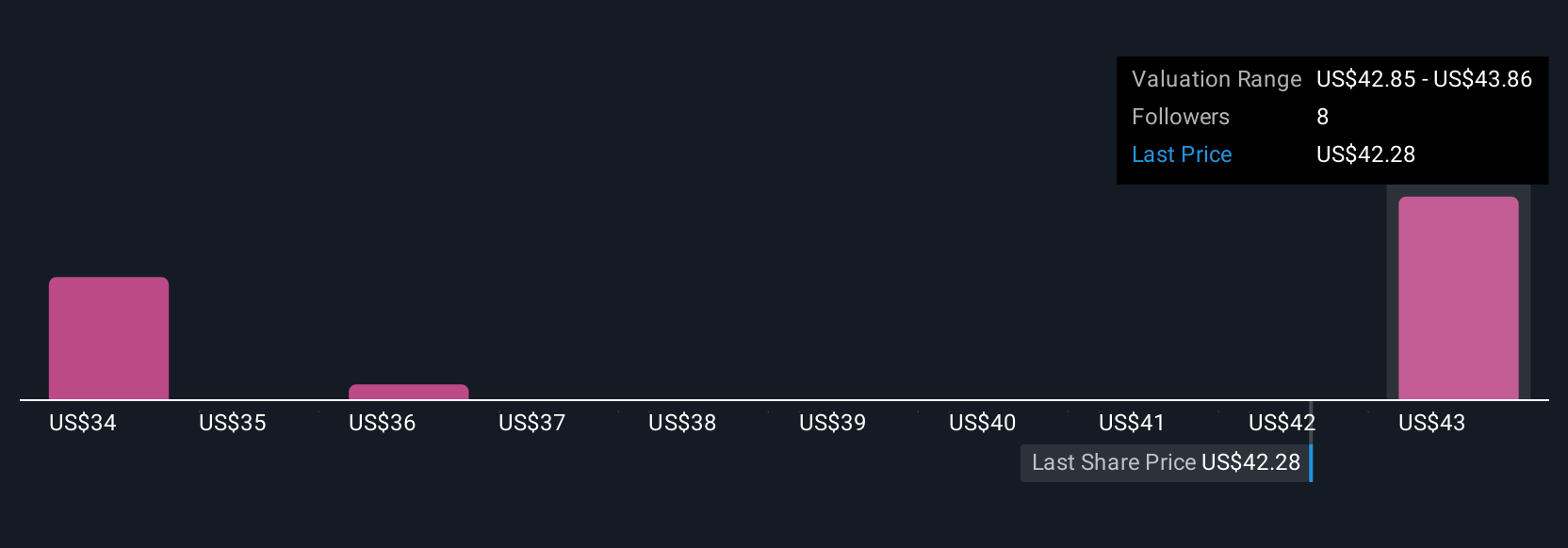

Uncover how NiSource's forecasts yield a $44.60 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members offered three fair value estimates for NiSource stock, ranging from US$34.03 to US$44.60 per share. With fresh capital raised, it is worth considering how NiSource’s substantial infrastructure modernization plans might affect both risk and reward, especially as views on future profitability and regulatory outcomes often differ widely.

Explore 3 other fair value estimates on NiSource - why the stock might be worth 20% less than the current price!

Build Your Own NiSource Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your NiSource research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free NiSource research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NiSource's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find companies with promising cash flow potential yet trading below their fair value.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NiSource might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NI

NiSource

An energy holding company, operates as a regulated natural gas and electric utility company in the United States.

Proven track record second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor