Advertisement

- United States

- /

- Renewable Energy

- /

- NasdaqGS:AY

Atlantica Sustainable Infrastructure plc Just Recorded A 45% EPS Beat: Here's What Analysts Are Forecasting Next

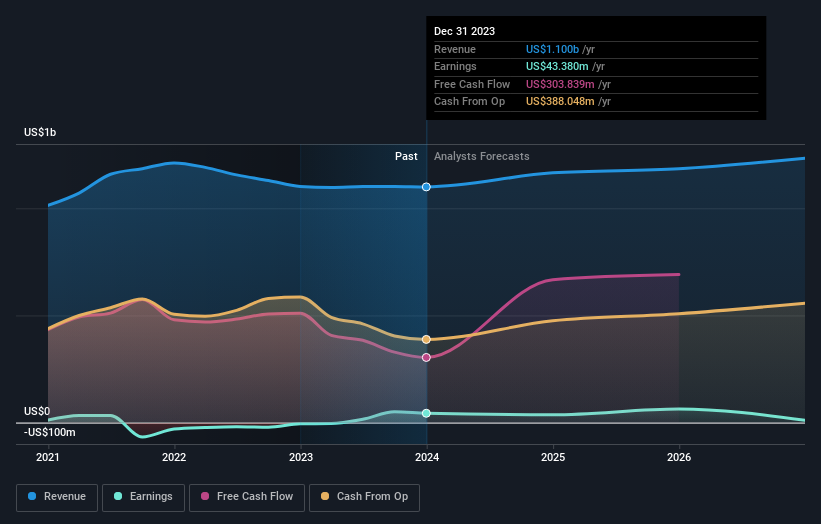

Atlantica Sustainable Infrastructure plc (NASDAQ:AY) came out with its yearly results last week, and we wanted to see how the business is performing and what industry forecasters think of the company following this report. It looks like a credible result overall - although revenues of US$1.1b were what the analysts expected, Atlantica Sustainable Infrastructure surprised by delivering a (statutory) profit of US$0.37 per share, an impressive 45% above what was forecast. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Check out our latest analysis for Atlantica Sustainable Infrastructure

Taking into account the latest results, the consensus forecast from Atlantica Sustainable Infrastructure's seven analysts is for revenues of US$1.17b in 2024. This reflects a reasonable 5.9% improvement in revenue compared to the last 12 months. Per-share earnings are expected to increase 4.1% to US$0.39. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.19b and earnings per share (EPS) of US$0.49 in 2024. The analysts seem less optimistic after the recent results, reducing their revenue forecasts and making a substantial drop in earnings per share numbers.

Despite the cuts to forecast earnings, there was no real change to the US$23.73 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Atlantica Sustainable Infrastructure at US$33.00 per share, while the most bearish prices it at US$19.00. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Atlantica Sustainable Infrastructure shareholders.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The analysts are definitely expecting Atlantica Sustainable Infrastructure's growth to accelerate, with the forecast 5.9% annualised growth to the end of 2024 ranking favourably alongside historical growth of 1.9% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 2.4% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Atlantica Sustainable Infrastructure to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Regrettably, they also downgraded their revenue estimates, but the latest forecasts still imply the business will grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Atlantica Sustainable Infrastructure. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Atlantica Sustainable Infrastructure analysts - going out to 2026, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 3 warning signs for Atlantica Sustainable Infrastructure (2 are a bit unpleasant) you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:AY

Atlantica Sustainable Infrastructure

Owns, manages, and invests in renewable energy, storage, natural gas and heat, electric transmission lines, and water assets in North America, South America, Europe, the Middle East, and Africa.

Slight with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

74 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$121.2% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$245.0% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.59.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3925.9% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

74 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative