Advertisement

- United States

- /

- Gas Utilities

- /

- NYSE:MIC

Here's Why Macquarie Infrastructure (NYSE:MIC) Has A Meaningful Debt Burden

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Macquarie Infrastructure Corporation (NYSE:MIC) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Macquarie Infrastructure

What Is Macquarie Infrastructure's Debt?

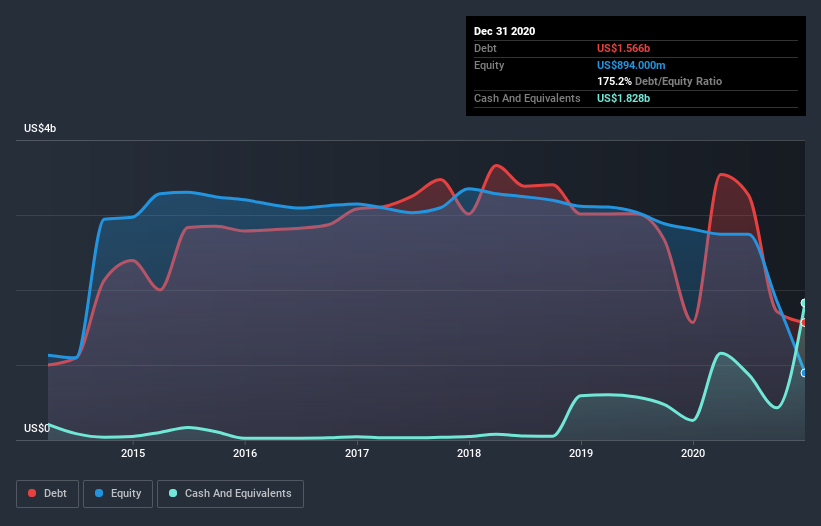

As you can see below, Macquarie Infrastructure had US$1.57b of debt, at December 2020, which is about the same as the year before. You can click the chart for greater detail. But it also has US$1.83b in cash to offset that, meaning it has US$262.0m net cash.

How Strong Is Macquarie Infrastructure's Balance Sheet?

We can see from the most recent balance sheet that Macquarie Infrastructure had liabilities of US$1.22b falling due within a year, and liabilities of US$2.06b due beyond that. Offsetting these obligations, it had cash of US$1.83b as well as receivables valued at US$47.0m due within 12 months. So its liabilities total US$1.41b more than the combination of its cash and short-term receivables.

Macquarie Infrastructure has a market capitalization of US$2.79b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. While it does have liabilities worth noting, Macquarie Infrastructure also has more cash than debt, so we're pretty confident it can manage its debt safely.

Importantly, Macquarie Infrastructure's EBIT fell a jaw-dropping 94% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Macquarie Infrastructure can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Macquarie Infrastructure may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, Macquarie Infrastructure actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

While Macquarie Infrastructure does have more liabilities than liquid assets, it also has net cash of US$262.0m. The cherry on top was that in converted 415% of that EBIT to free cash flow, bringing in US$287m. So although we see some areas for improvement, we're not too worried about Macquarie Infrastructure's balance sheet. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Macquarie Infrastructure (at least 1 which can't be ignored) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading Macquarie Infrastructure or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:MIC

Macquarie Infrastructure Holdings

Macquarie Infrastructure Holdings, LLC, together with its subsidiaries, operates as an energy company that processes and distributes gas, and provides related services to corporations, government agencies, and individual customers.

Mediocre balance sheet and overvalued.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|40.5% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|91.8% undervalued

DO

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.5% undervalued

AG

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|16.2% undervalued

CL

Community Contributor