Advertisement

- United States

- /

- Airlines

- /

- NYSE:DAL

How Delta’s AI-Powered Fare Strategy Impacts Its Valuation in 2025

Simply Wall St

Reviewed by Simply Wall St

If you are considering what to do with Delta Air Lines stock right now, you are not alone. The past year has been a ride, with the share price up almost 49% over the last 12 months and a staggering 82% gain over three years. But what is truly catching investors’ attention is the narrative behind those gains: a mix of optimism, risk, and shifting strategy that feels almost like a preview of what is next, rather than just a look in the rearview mirror.

Delta’s stock has moved higher recently, thanks in part to its ambitious use of artificial intelligence to optimize fare prices, with the company targeting 20% of its domestic flights to be dynamically priced by year end. Investors seem to be buying into the idea that smarter pricing can drive more consistent revenues, even as external events such as flight cancellations or regulatory threats briefly shake confidence. The ongoing government review of its partnership with Aeromexico and other recent headlines have added some drama, but so far, have not dimmed the stock’s longer-term uptrend.

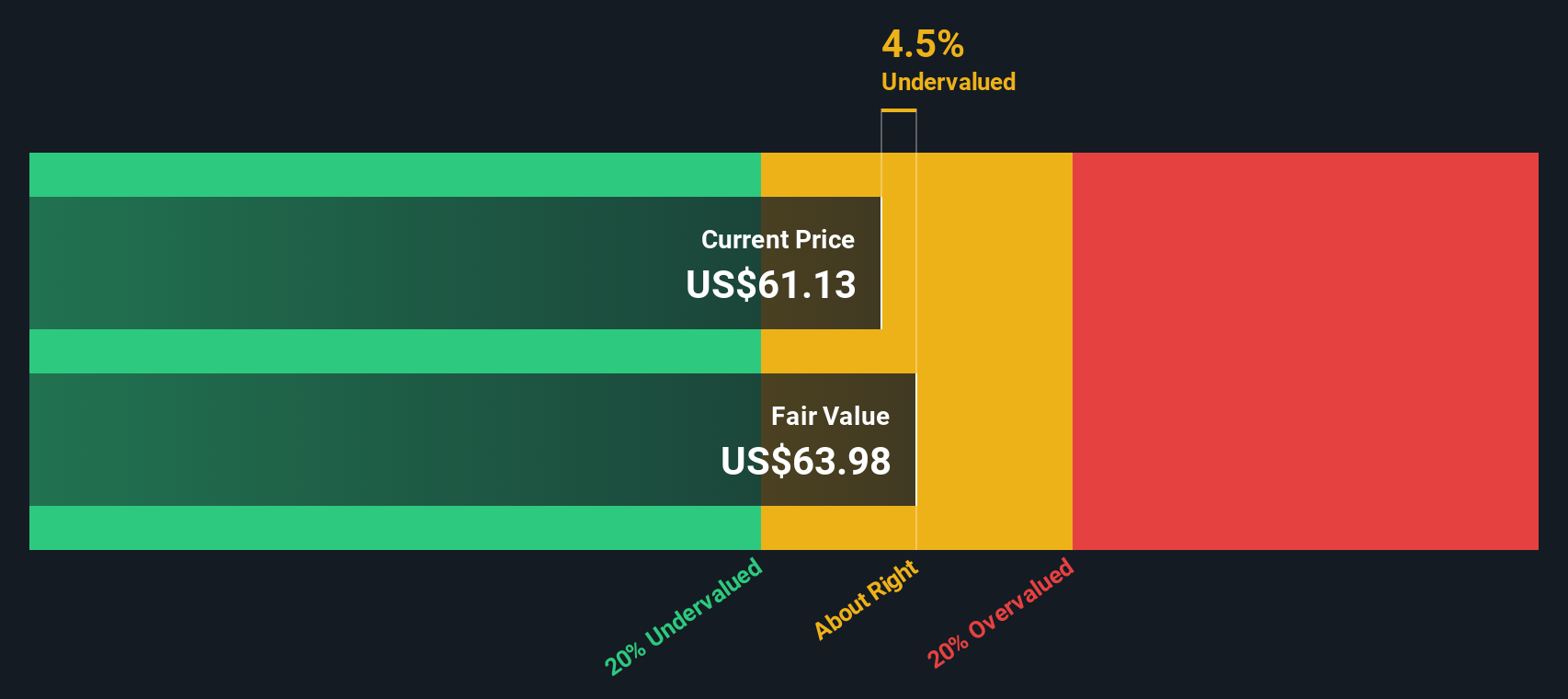

So what does all of this mean for valuation? On a simple value score, Delta clocks in at 4 out of 6, indicating the stock is undervalued by several important checks, though not across the board. We will break down what those checks are and how Delta stacks up against typical valuation models. As you will see, sometimes the usual screens are just the beginning, and there is a smarter way to look at what a company is really worth.

Delta Air Lines delivered 48.7% returns over the last year. See how this stacks up to the rest of the Airlines industry.Approach 1: Delta Air Lines Cash Flows

The Discounted Cash Flow (DCF) model helps investors estimate a company’s intrinsic value by projecting its future free cash flows and then discounting those numbers back to today’s value. This gives a clearer picture of what the business may actually be worth, beyond its current share price.

For Delta Air Lines, the most recent twelve months saw free cash flow reach $1.64 billion. Looking forward, analysts project consistent growth, with free cash flow expected to climb to about $3.10 billion in 2035. Over the next decade, annual projections show a pattern of steady increases. Some slowdown is typical in later years as the business matures.

Based on these assumptions, the DCF model estimates Delta’s fair value per share at $63.61. When compared to the current market price, the stock is about 7.2% undervalued. This suggests the current price and the “true value” of the business are fairly close, indicating that the market is pricing Delta with reasonable accuracy at this time.

Result: ABOUT RIGHT

Approach 2: Delta Air Lines Price vs Earnings

For profitable companies like Delta Air Lines, the Price-to-Earnings (PE) ratio is one of the most widely used valuation tools. It allows investors to see how much they are paying for each dollar of earnings. This method provides a simple, effective way to gauge if the stock is trading at a premium or discount relative to its profits. Growth expectations, industry trends, and risk factors all influence what makes a “normal” or “fair” PE ratio for any given stock. Companies with strong growth prospects or lower perceived risk often command higher multiples, while those with slower growth or higher risk tend to trade at lower PE ratios.

Delta is trading at a PE ratio of 8.5x. That figure is considerably lower than both the broader airline industry average of 9.8x and the average among Delta’s peers at 21.8x. To provide an even more tailored benchmark, the Fair Ratio, calculated by Simply Wall St using factors like Delta’s earnings growth, profit margins, industry conditions, and risks, stands at 12.0x for this stock.

Comparing Delta’s current 8.5x PE ratio to its Fair Ratio of 12.0x suggests that Delta appears to be undervalued on this basis. The stock trades well below what would be considered fair for a company with its characteristics and market context.

Result: UNDERVALUED

Upgrade Your Decision Making: Choose your Delta Air Lines Narrative

Narratives go beyond numbers by giving you the story behind a company. Your perspective on a company's strategy, risks, and opportunities shapes your view of its future value and performance. In simple terms, a Narrative connects what you believe about a business—such as its competitive strengths or changing industry trends—to a specific, data-driven forecast and fair value, making your analysis clearer and more actionable.

On the Simply Wall St platform, Narratives are designed to be highly accessible, allowing you to see and share your perspective alongside those of millions of other investors. This can help you make more informed decisions by directly comparing your Fair Value to the current Price and by seeing how your assumptions compare to the wider community. The best part is that Narratives update automatically when new news, earnings, or company events are released, so your investment thesis can evolve with the facts and not just with changes in market sentiment.

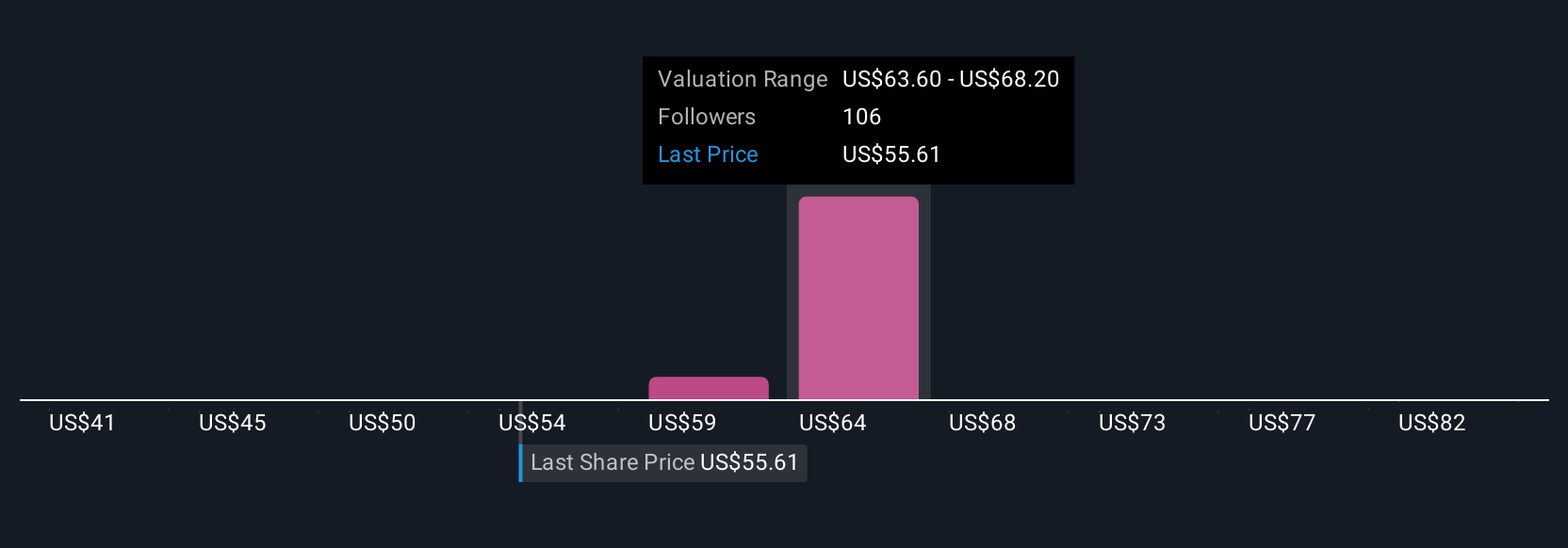

For Delta Air Lines, for example, some users base their outlooks on cautious forecasts ($49 fair value) while others see much more potential upside ($90 fair value), depending on their chosen assumptions about growth, risks, and margins.

Do you think there's more to the story for Delta Air Lines? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DAL

Delta Air Lines

Provides scheduled air transportation for passengers and cargo in the United States and internationally.

Good value with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor