Advertisement

- United States

- /

- Transportation

- /

- NasdaqGS:LYFT

Is Lyft (NASDAQ:LYFT) Using Debt Sensibly?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Lyft, Inc. (NASDAQ:LYFT) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Lyft

How Much Debt Does Lyft Carry?

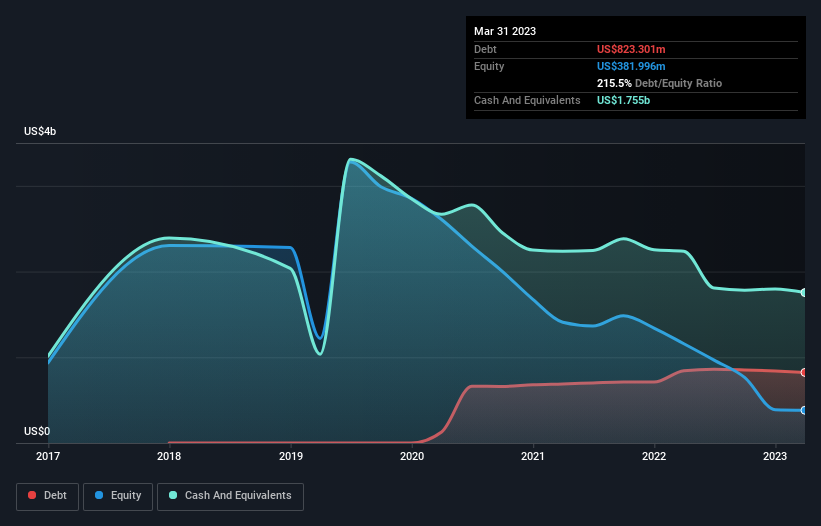

As you can see below, Lyft had US$823.3m of debt, at March 2023, which is about the same as the year before. You can click the chart for greater detail. However, its balance sheet shows it holds US$1.75b in cash, so it actually has US$931.5m net cash.

A Look At Lyft's Liabilities

Zooming in on the latest balance sheet data, we can see that Lyft had liabilities of US$3.14b due within 12 months and liabilities of US$1.01b due beyond that. On the other hand, it had cash of US$1.75b and US$321.1m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$2.07b.

This deficit isn't so bad because Lyft is worth US$4.10b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. While it does have liabilities worth noting, Lyft also has more cash than debt, so we're pretty confident it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Lyft's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Lyft wasn't profitable at an EBIT level, but managed to grow its revenue by 21%, to US$4.2b. With any luck the company will be able to grow its way to profitability.

So How Risky Is Lyft?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Lyft had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of US$290m and booked a US$1.6b accounting loss. But the saving grace is the US$931.5m on the balance sheet. That means it could keep spending at its current rate for more than two years. With very solid revenue growth in the last year, Lyft may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Lyft , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:LYFT

Lyft

Operates a peer-to-peer marketplace for on-demand ridesharing in the United States and Canada.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on Myseum ·

The Future of Social Sharing Is Private and People Are Ready

Fair Value:US$7.9577.1% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on ASML Holding ·

EU#3 - From Philips Management Buyout to Europe’s Biggest Company

Fair Value:€1.31k7.1% undervalued

29 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

YI

yiannisz on Booking Holdings ·

Booking Holdings: Why Ground-Level Travel Trends Still Favor the Platform Giants

Fair Value:US$5.47k8.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CO

composite32 on Shell ·

A fully integrated LNG business seems to be ignored by the market.

Fair Value:UK£36.122.6% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

EM

emndy on Presco ·

High Quality Business and a true compounding machine

Fair Value:₦2.2k25.7% undervalued

10 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CL

Clive_Thompson on Roche Holding ·

Roche Holding AG To Benefit From Strong Drug Pipeline In 2027 And Beyond

Fair Value:CHF 430.0118.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Otokar Otomotiv ve Savunma Sanayi ·

Otokar is the first choice for tactical armored land vehicles to meet Europe's defense industry needs.

Fair Value:₺668.1135.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3324.4% undervalued

71 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0224.5% undervalued

1048 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Amazon.com ·

AMZN: Acceleration In Cloud And AI Will Drive Margin Expansion Ahead

Fair Value:US$295.6119.1% undervalued

1344 followersusers have followed this narrative

5 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

JA

jayhcee on Motorcar Parts of America ·

MPAA often has inventory and core-related timing issues. While this quarter’s problems may ease, similar issues have recurred historically and can persist for several quarters. It's not a one-off, it's a structural part of their business. Core returns are simply estimates: How many customers will actually return the original part; how quickly they'll do so; how many are useable; what they're worth, etc. MPAA predicts X sales in a quarter and Y core returns and its reserves, inventory values, etc. are based on that. If they expect a 90% core return rate and only 80% come back it doesn't change cash but they have to write down inventory and increase cost of goods sold which impacts EPS. They've also cited inventory buildup at key customers multiple times in the past. The assumption the latest backlog will all shift into future quarters this year with no impact on pricing, etc. seems more like wishful thinking. Retailer X was slated to buy $10m in parts this quarter but finds they have a lot more inventory on hand than they anticipated so they pushed the order. Realistically there are likely to be SKU cuts, reduction in safety stock on others, etc. Assuming that all $10m will come in this year plus the regular replenishment seems pretty unrealistic. MPAA also has a shaky track record when it comes to new lines and the supposed impact on business. If you look at the EV testing solutions hype back around 2020 that was supposed to diversify them beyond traditional reman and be a higher margin business that would grow with EV adoption. But it has never turned into a material contributor. The debt reduction and stock buy backs are meaningful but IMHO this narrative takes a very optimistic view of things.

0

|0