Advertisement

- United States

- /

- Transportation

- /

- NasdaqGS:CAR

Benign Growth For Avis Budget Group, Inc. (NASDAQ:CAR) Underpins Its Share Price

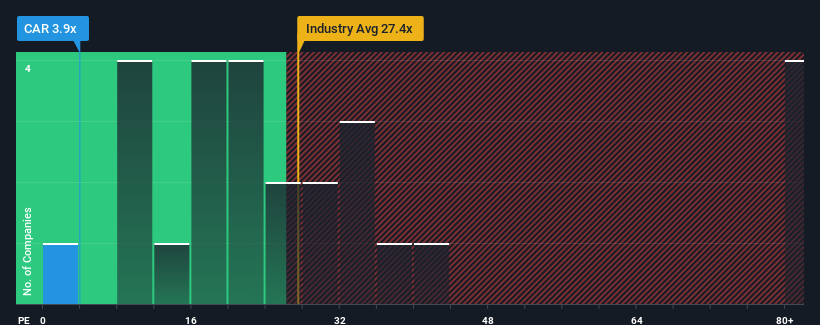

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") above 18x, you may consider Avis Budget Group, Inc. (NASDAQ:CAR) as a highly attractive investment with its 3.9x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

With earnings that are retreating more than the market's of late, Avis Budget Group has been very sluggish. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

See our latest analysis for Avis Budget Group

Does Growth Match The Low P/E?

Avis Budget Group's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 60%. Even so, admirably EPS has lifted 740% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Shifting to the future, estimates from the seven analysts covering the company suggest earnings growth is heading into negative territory, declining 20% per annum over the next three years. Meanwhile, the broader market is forecast to expand by 10% each year, which paints a poor picture.

With this information, we are not surprised that Avis Budget Group is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Avis Budget Group's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 3 warning signs for Avis Budget Group (2 don't sit too well with us!) that you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CAR

Avis Budget Group

Provides car and truck rentals, car sharing, and ancillary products and services to businesses and consumers in the Americas, Europe, the Middle East and Africa, Asia, and Australasia.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor