Advertisement

- United States

- /

- Telecom Services and Carriers

- /

- NasdaqCM:SIFY

A Look At Sify Technologies (NasdaqCM:SIFY) Valuation After Data Center IPO Steps And Capital Structure Changes

Sify Technologies (SIFY) is drawing fresh attention after its data center arm, Sify Infinit Spaces, converted Kotak held compulsorily convertible debentures into equity and reshaped investor agreements ahead of a planned Indian IPO.

See our latest analysis for Sify Technologies.

At a share price of $15.05, Sify Technologies has seen a 24.79% 90 day share price return and a very large 1 year total shareholder return of 242.82%, suggesting momentum has recently been building.

If this data center news has you thinking about where digital infrastructure goes next, it could be a good moment to scan 34 AI infrastructure stocks as potential companions to your watchlist.

With Sify posting a very large 1 year total shareholder return and analysts setting a US$22 price target above the current US$15.05 share price, the key question is whether there is still an opportunity to invest here or if markets are already pricing in future growth.

Most Popular Narrative: 31.6% Undervalued

With Sify Technologies last closing at $15.05 against a widely followed fair value estimate of $22, the current market price sits well below that narrative anchor.

Sify Technologies is investing in AI capabilities, likely leading to increased demand from enterprises seeking mature network, data center, and digital services. This is expected to impact revenue and earnings positively as AI workloads grow in India.

Want to see what sits behind that valuation gap? The narrative leans heavily on fast rising revenue, a clear earnings swing, and a future profit multiple that assumes sustained traction. Curious which specific forecasts and margin shifts need to land for $22 to make sense? The full breakdown lays out the numbers and timing in detail.

Result: Fair Value of $22 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh execution risks, including ongoing losses and high SG&A and expansion costs that could keep margins under pressure longer than expected.

Find out about the key risks to this Sify Technologies narrative.

Another Angle On The Valuation

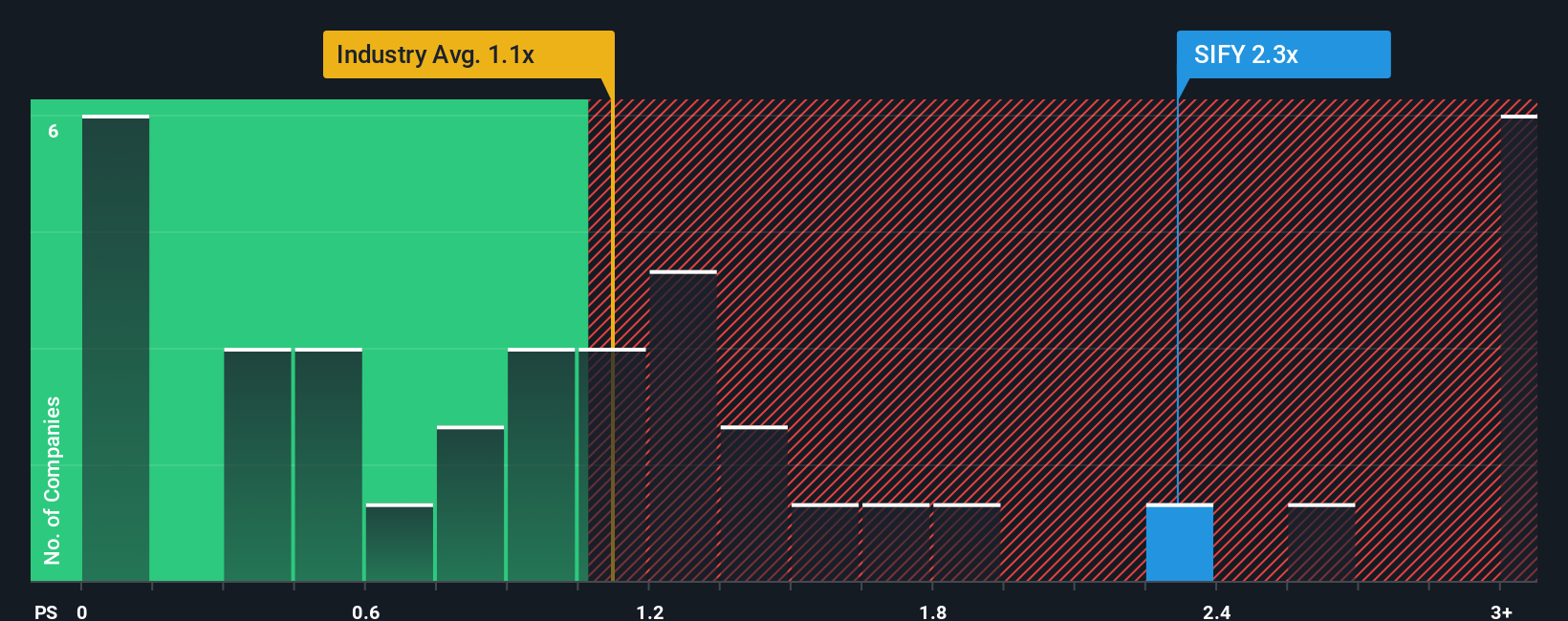

The fair value narrative suggests Sify Technologies looks 31.6% undervalued at $22, but the price tag tells a different story when you look at sales. Sify trades on a P/S of 2.3x, which is richer than both the US Telecom industry at 1.2x and its own fair ratio of 1.8x, so is this really a discount or just optimism priced in early?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With all this in mind, do the story and the numbers line up for you, or not yet? It is worth moving quickly to test the data yourself and see how it stacks up against the mix of concerns and optimism captured in 1 key reward and 1 important warning sign

Looking for more investment ideas?

If this Sify story has sharpened your focus, do not stop here. The next move that fits your portfolio might sit just outside your current watchlist.

- Target resilient income by checking out 13 dividend fortresses, which aim to combine higher yields with balance sheets you can scrutinize in detail.

- Hunt for potential value by scanning screener containing 24 high quality undiscovered gems, which our filters flag for strong fundamentals but limited market attention so far.

- Prioritise capital protection first by reviewing 83 resilient stocks with low risk scores, which score well on stability and downside risk metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:SIFY

Sify Technologies

Offers information and communication technology solutions and services in India and internationally.

High growth potential with worrying balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.3% undervalued

151 followersusers have followed this narrative

1 commentusers have commented on this narrative

25 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k22.9% overvalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9417.0% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87185.3% overvalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AG

Agricola on Midland Exploration ·

A Case for Midland Exploration Inc Base CAD$8.75 (18x), Bull CAD$12.50 (25x+)

Fair Value:CA$8.7594.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BR

Brenin on Tristel ·

Tristel's US Expansion Could Spark a 286% Revenue Surge

Fair Value:UK£2.25k99.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

A1

A10 on Vanguard Whitehall Funds - Vanguard High Dividend Yield ETF ·

My take on VYM

Fair Value:US$19825.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

55 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9825.2% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$594.6234.1% undervalued

1313 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative