Advertisement

Methode Electronics' (NYSE:MEI) Dividend Will Be $0.14

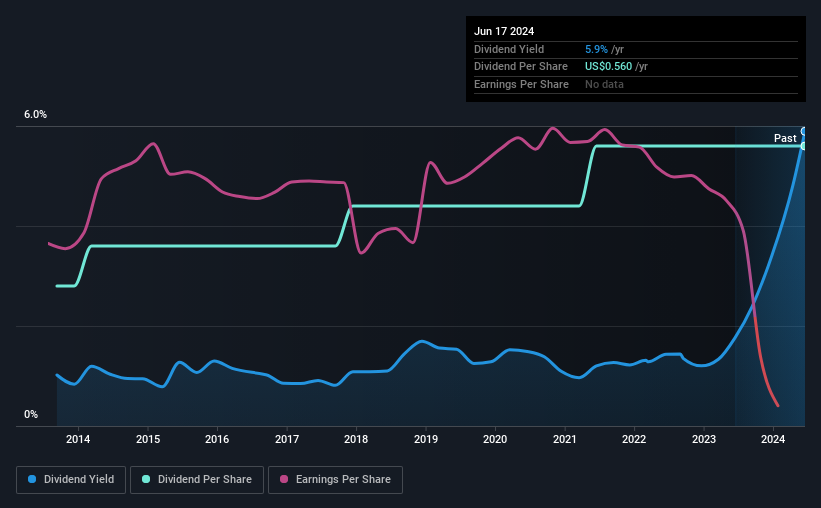

The board of Methode Electronics, Inc. (NYSE:MEI) has announced that it will pay a dividend on the 26th of July, with investors receiving $0.14 per share. The dividend yield will be 5.9% based on this payment which is still above the industry average.

Check out our latest analysis for Methode Electronics

Methode Electronics Doesn't Earn Enough To Cover Its Payments

A big dividend yield for a few years doesn't mean much if it can't be sustained. Methode Electronics isn't generating any profits, and it is paying out a very high proportion of the cash it is earning. This is quite a strong warning sign that the dividend may not be sustainable.

Over the next year, EPS is forecast to expand by 110.7%. Assuming the dividend continues along recent trends, we think the payout ratio could get very high, which probably can't continue without starting to put some pressure on the balance sheet.

Methode Electronics Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. The annual payment during the last 10 years was $0.28 in 2014, and the most recent fiscal year payment was $0.56. This works out to be a compound annual growth rate (CAGR) of approximately 7.2% a year over that time. Dividends have grown at a reasonable rate over this period, and without any major cuts in the payment over time, we think this is an attractive combination as it provides a nice boost to shareholder returns.

The Dividend Has Limited Growth Potential

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. However, things aren't all that rosy. Methode Electronics' EPS has fallen by approximately 19% per year during the past five years. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this becomes a long term trend.

Methode Electronics' Dividend Doesn't Look Sustainable

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. In the past the payments have been stable, but we think the company is paying out too much for this to continue for the long term. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For instance, we've picked out 1 warning sign for Methode Electronics that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MEI

Methode Electronics

Designs, engineers, produces, and sells mechatronic products internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.3% undervalued

143 followersusers have followed this narrative

1 commentusers have commented on this narrative

24 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k22.4% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9421.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87177.0% overvalued

3 followersusers have followed this narrative

1 commentusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Red Cat Holdings ·

Red Cat Holdings (RCAT): The Small-Drone Contender Bracing for Q4 Impact

Fair Value:US$18.458.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Micron Technology ·

Micron Technology Inc. (MU): The "Silicon Gold" Rush Reaches a Fever Pitch

Fair Value:US$4956.7% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Jabil ·

Jabil Inc. (JBL): The AI "Picks and Shovels" Play Ahead of Earnings

Fair Value:US$295.511.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.8% undervalued

54 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9824.4% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.0% undervalued

1312 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0