Advertisement

Earnings Update: Here's Why Analysts Just Lifted Their Methode Electronics, Inc. (NYSE:MEI) Price Target To US$10.25

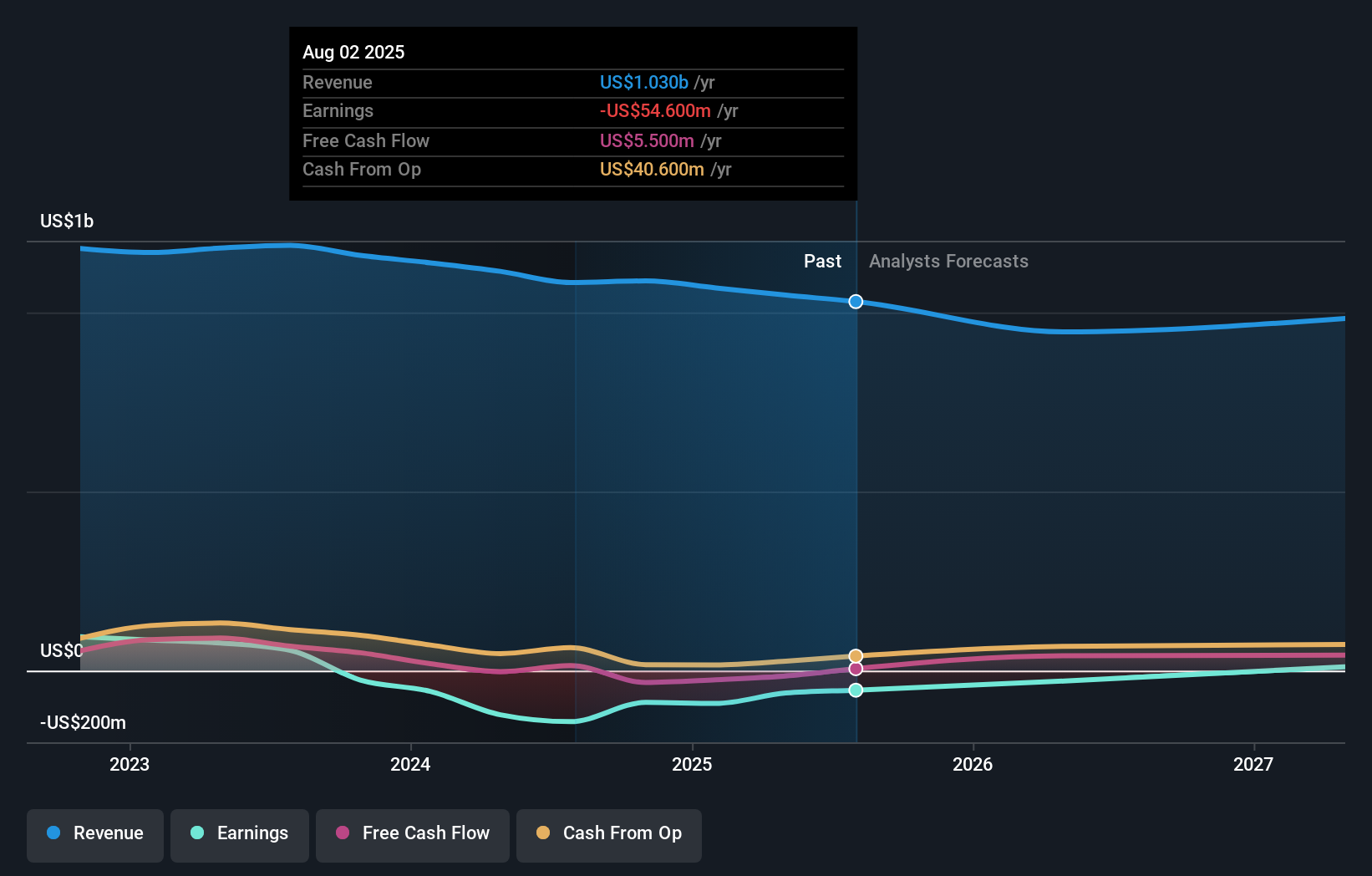

As you might know, Methode Electronics, Inc. (NYSE:MEI) just kicked off its latest first-quarter results with some very strong numbers. Methode Electronics outperformed estimates, with revenues of US$241m beating estimates by 11%. Statutory losses were US$0.29, 28% smaller thanthe analysts expected. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Following the recent earnings report, the consensus from three analysts covering Methode Electronics is for revenues of US$945.6m in 2026. This implies a definite 8.2% decline in revenue compared to the last 12 months. Per-share statutory losses are expected to explode, reaching US$0.82 per share. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$925.9m and earnings per share (EPS) of US$0.67 in 2026. While they've upgraded their revenue numbers for next year, the consensus also expects losses to increase, perhaps due to the investments required to fund that growth In any event, it's not clear that these new estimates are particularly bullish.

See our latest analysis for Methode Electronics

It will come as a surprise to learn that the consensus price target rose 7.9% to US$10.25, with the analysts clearly more interested in growing revenue, even as losses intensify. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Methode Electronics analyst has a price target of US$12.00 per share, while the most pessimistic values it at US$8.50. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 11% by the end of 2026. This indicates a significant reduction from annual growth of 0.4% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 8.4% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Methode Electronics is expected to lag the wider industry.

The Bottom Line

The biggest low-light for us was that the forecasts for Methode Electronics dropped from profits to a loss next year. They also upgraded their revenue estimates for next year, even though it is expected to grow slower than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that in mind, we wouldn't be too quick to come to a conclusion on Methode Electronics. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Methode Electronics analysts - going out to 2027, and you can see them free on our platform here.

Even so, be aware that Methode Electronics is showing 1 warning sign in our investment analysis , you should know about...

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:MEI

Methode Electronics

Designs, engineers, manufacture, and sells mechatronic products in North America, Europe, the Middle East, Africa, and Asia.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1939.7% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6527.1% undervalued

37 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.6% undervalued

13 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30155.3% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

PI

PittTheYounger on Erste Group Bank ·

An Austrian industry leader with attractive CEE exposure

Fair Value:€149.2321.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EU

European_Hidden_Gem_Stocks on Yü Group ·

Massive Cash Pile. Accelerating Growth. Is the Market Mispricing Yü Group?

Fair Value:UK£44.4263.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PR

PrashhD on MRF ·

MRF to See 22.9% Future PE Growth in Five Years

Fair Value:₹117.53k12.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.3% undervalued

90 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5451.0% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3462.5% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative