Advertisement

A Quick Analysis On Keysight Technologies' (NYSE:KEYS) CEO Compensation

Ron Nersesian became the CEO of Keysight Technologies, Inc. (NYSE:KEYS) in 2013, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether Keysight Technologies pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

Check out our latest analysis for Keysight Technologies

Comparing Keysight Technologies, Inc.'s CEO Compensation With the industry

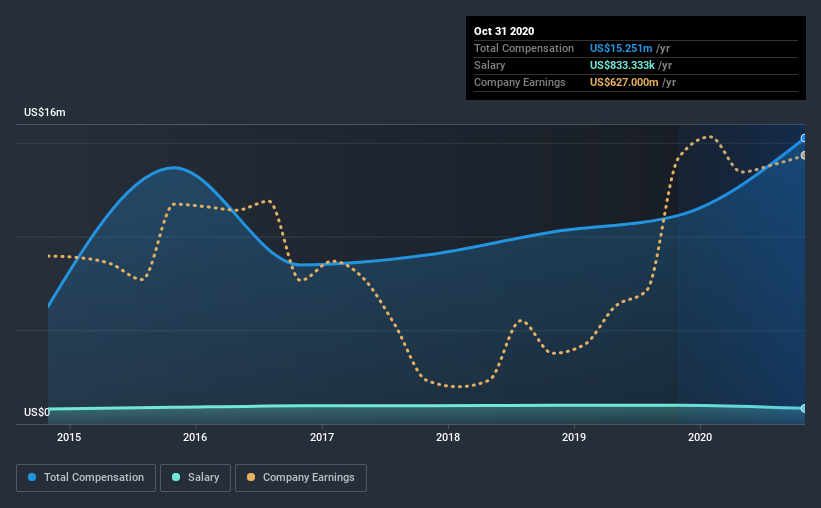

According to our data, Keysight Technologies, Inc. has a market capitalization of US$26b, and paid its CEO total annual compensation worth US$15m over the year to October 2020. Notably, that's an increase of 37% over the year before. While we always look at total compensation first, our analysis shows that the salary component is less, at US$833k.

In comparison with other companies in the industry with market capitalizations over US$8.0b , the reported median total CEO compensation was US$9.0m. Accordingly, our analysis reveals that Keysight Technologies, Inc. pays Ron Nersesian north of the industry median. What's more, Ron Nersesian holds US$37m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | US$833k | US$1.0m | 5% |

| Other | US$14m | US$10m | 95% |

| Total Compensation | US$15m | US$11m | 100% |

Talking in terms of the industry, salary represented approximately 34% of total compensation out of all the companies we analyzed, while other remuneration made up 66% of the pie. Keysight Technologies sets aside a smaller share of compensation for salary, in comparison to the overall industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Keysight Technologies, Inc.'s Growth

Over the past three years, Keysight Technologies, Inc. has seen its earnings per share (EPS) grow by 81% per year. It saw its revenue drop 1.9% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. While it would be good to see revenue growth, profits matter more in the end. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Keysight Technologies, Inc. Been A Good Investment?

Most shareholders would probably be pleased with Keysight Technologies, Inc. for providing a total return of 205% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

As previously discussed, Ron is compensated more than what is normal for CEOs of companies of similar size, and which belong to the same industry. However, Keysight Technologies has produced strong EPS growth and shareholder returns over the last three years. Considering such exceptional results for the company, we'd venture to say CEO compensation is fair. The pleasing shareholder returns are the cherry on top. We wouldn't be wrong in saying that shareholders feel that Ron's performance creates value for the company.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 3 warning signs for Keysight Technologies that you should be aware of before investing.

Important note: Keysight Technologies is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

When trading Keysight Technologies or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Keysight Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:KEYS

Keysight Technologies

Provides electronic design and test solutions worldwide.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on Myseum ·

The Future of Social Sharing Is Private and People Are Ready

Fair Value:US$7.9575.5% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on ASML Holding ·

EU#3 - From Philips Management Buyout to Europe’s Biggest Company

Fair Value:€1.31k8.7% undervalued

25 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

YI

yiannisz on Booking Holdings ·

Booking Holdings: Why Ground-Level Travel Trends Still Favor the Platform Giants

Fair Value:US$5.47k6.9% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CO

composite32 on Shell ·

A fully integrated LNG business seems to be ignored by the market.

Fair Value:UK£36.124.3% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

TH

TheInternationalInvestor on Hotel101 Global Holdings ·

Hotel101 Global: A Scalable Hospitality Platform Built to Compound

Fair Value:US$17.2352.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Tesla ·

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value:US$588.1826.6% undervalued

171 followersusers have followed this narrative

28 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.5% undervalued

37 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3321.8% undervalued

70 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0224.3% undervalued

1042 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

WE

WealthAP on Alphabet ·

The "Easy Money" Is Gone: Why Alphabet Is Now a "Show Me" Story

Fair Value:US$386.4313.0% undervalued

48 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

Trending Discussion

HO

Holger on IREN ·

<b>Reported:</b> Revenue growth: 2024 → 2025 sharp increase of approx. 165%. Assuming moderate annual growth of 40%, a fair value in three years would be approx. $170. Given the customer base and the story, this should be possible. I find the most valuable “property” particularly interesting, as it solves the electricity problem.

1

|0

HE

Hemingway on Aeva Technologies ·

NVDA+AEVA Agreement is a game changer for the AEVA stock even though it is just a partnership and does not have a roll out until 2028 (which means receivables as early as 2027, I would imagine) This agreement effectively moves the goal posts of profitability for AEVA much closer since this is in addition to the recent Forterra agreement, as well as the (previously announced) European carmaker agreement (which is believed to be Mercedes-Benz and estimated to be worth at least 1 billion in sales alone) Underneath all of this, AEVA has a pre-existing agreement with Daimler Truck. So business seems to be booming, especially with really big name brands…which tends to bring in even more brand names (and thus more agreements/contracts/announcements, etc). This dynamic often creates more coverage from analysts (often with upside stock initial coverage) that I believe will be occurring over the next 3 to 6 months (as professional traders/analysts often research for 2 to 3 months before initiating coverage of a new issue). I also feel that the above momentum increases the likelihood that companies that do not currently utilize 4G LIDAR technology might consider buying AEVA outright. Realistically, even with a substantial premium to the current stock price, the cost of AEVA would be a rounding error for the likes of a company such as Tesla, and certainly would allow them to maintain their technological edge as the competition for self-driving vehicles continues to heat up. However, I think it is equally possible for NVidea to decide to lock-in the AEVA technology for their upcoming autonomous hardware/software package by buying them outright. Obviously, the above factors and recent activity in the AEVA stock are cause for optimism. Of course, this all just one opinion , so please do your own due diligence. Disclaimer: I/We DO trade in this stock from time to time and I/we may (or may not have) a position currently, so again, please do your own due diligence.

0

|0