Coherent (COHR) shares have seen a sharp pullback of 2.5% at the close, reversing part of their steady month-long climb. The move has caught the attention of investors tracking the company's recent performance.

After building strong momentum year to date with a 27.95% share price return and delivering an impressive 37.54% total shareholder return over the past year, Coherent’s latest slip comes after a period of remarkable gains. While short-term volatility is grabbing attention, the long-term trajectory still reflects substantial value creation for shareholders.

With the stock still up substantially over the past year but currently trading just above its intrinsic value and slightly above analyst targets, investors face a classic dilemma: is Coherent now undervalued, or is all the optimism already priced in?

Advertisement

Most Popular Narrative: 6.7% Overvalued

The most-followed narrative places Coherent’s fair value at $120.63, about 6% below the recent close of $128.70. This suggests that the latest rally has pushed the shares just beyond what’s justified by fundamentals. Here is one key insight that is shaping this view on valuation.

The ongoing expansion of AI datacenter infrastructure and high-performance computing is propelling structural growth in demand for advanced optical transceivers (800G, 1.6T, and beyond), optical circuit switches, and related photonics components, which is fueling robust sequential order growth and sustained revenue momentum in Coherent's datacom and communications business.

Want to know what big narrative assumptions drive this premium? This fair value hinges on rapid infrastructure growth, margin expansion, and future profit multiples rarely seen outside top tech. Get the details underlying this bold valuation call. See the dramatic projections shaping the consensus target.

However, ongoing pricing pressure from low-cost Asian rivals and unpredictable fluctuations in end-market demand could quickly challenge the current upbeat outlook.

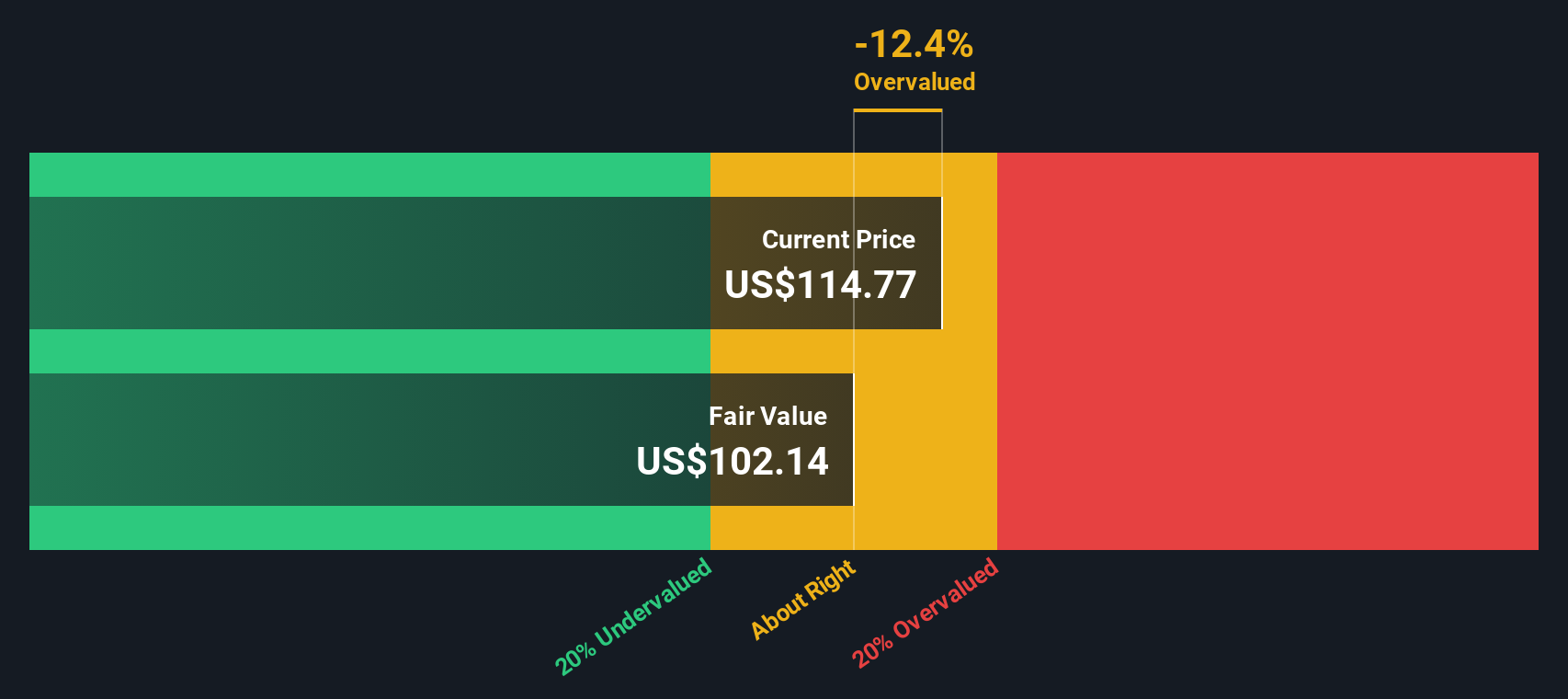

Looking at Coherent through the lens of our DCF model, there is a different perspective. The DCF approach suggests that, at $128.70, the stock is trading slightly below our fair value estimate of $131.33. This signals a modest undervaluation rather than a premium. This contrast raises the question: Could forward-looking cash flow potential be the key investors are missing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Coherent for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 841 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Coherent Narrative

If you prefer hands-on analysis or want to see if your own perspective leads to a different conclusion, you can easily build your own view in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Coherent.

Looking for More Smart Investment Ideas?

Serious investors always keep their edge by scanning for unique opportunities. Don’t let the next big winner slip past you. Energize your portfolio today using these hand-picked stock ideas:

Ride the wave of artificial intelligence innovation by checking out these 27 AI penny stocks poised to benefit from the AI technology boom.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Develops, manufactures, and markets engineered materials, optoelectronic components and devices, and laser systems for the use in the industrial, communications, electronics, and instrumentation markets worldwide.