Advertisement

Assessing Arrow Electronics (ARW) Valuation After Recent Share Price Momentum

Arrow Electronics stock: recent move and key fundamentals

Arrow Electronics (ARW) has drawn closer investor attention after a recent share price move, prompting a closer look at how its current performance metrics and business profile line up for longer term holders.

See our latest analysis for Arrow Electronics.

At a share price of US$132.91, Arrow Electronics has seen firm near term momentum, with a 30 day share price return of 17.61% and a 1 year total shareholder return of 13.60%, while the 3 year total shareholder return of 0.29% suggests much flatter longer term progress.

If Arrow’s recent move has you reviewing your watchlist, this could be a useful moment to widen the net and check out high growth tech and AI stocks as potential comparison ideas.

With Arrow trading at US$132.91 and sitting above an analyst price target of US$108.25, plus an intrinsic value estimate suggesting a premium, you have to ask: is there still a buying opportunity here, or is future growth already priced in?

Most Popular Narrative: 23% Overvalued

Arrow Electronics last closed at $132.91, compared with a most widely followed fair value estimate of $108.25, putting the current price above that narrative view.

The normalization of customer inventory levels and broad-based backlog growth, especially in mass market segments, point to improving order patterns and sustainable sales momentum, increasing the likelihood of stronger operating leverage and earnings growth as volumes return across regions.

Curious what kind of revenue path and margin profile sits behind that fair value, and how earnings and share count assumptions fit together? The narrative spells out a detailed road map for how Arrow could get there, including how much profit power is being penciled in a few years from now and what kind of earnings multiple that might support.

Result: Fair Value of $108.25 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points, including potential distributor disintermediation and uneven demand recovery, that could challenge revenue, margins and the current valuation story.

Find out about the key risks to this Arrow Electronics narrative.

Another view on Arrow’s valuation

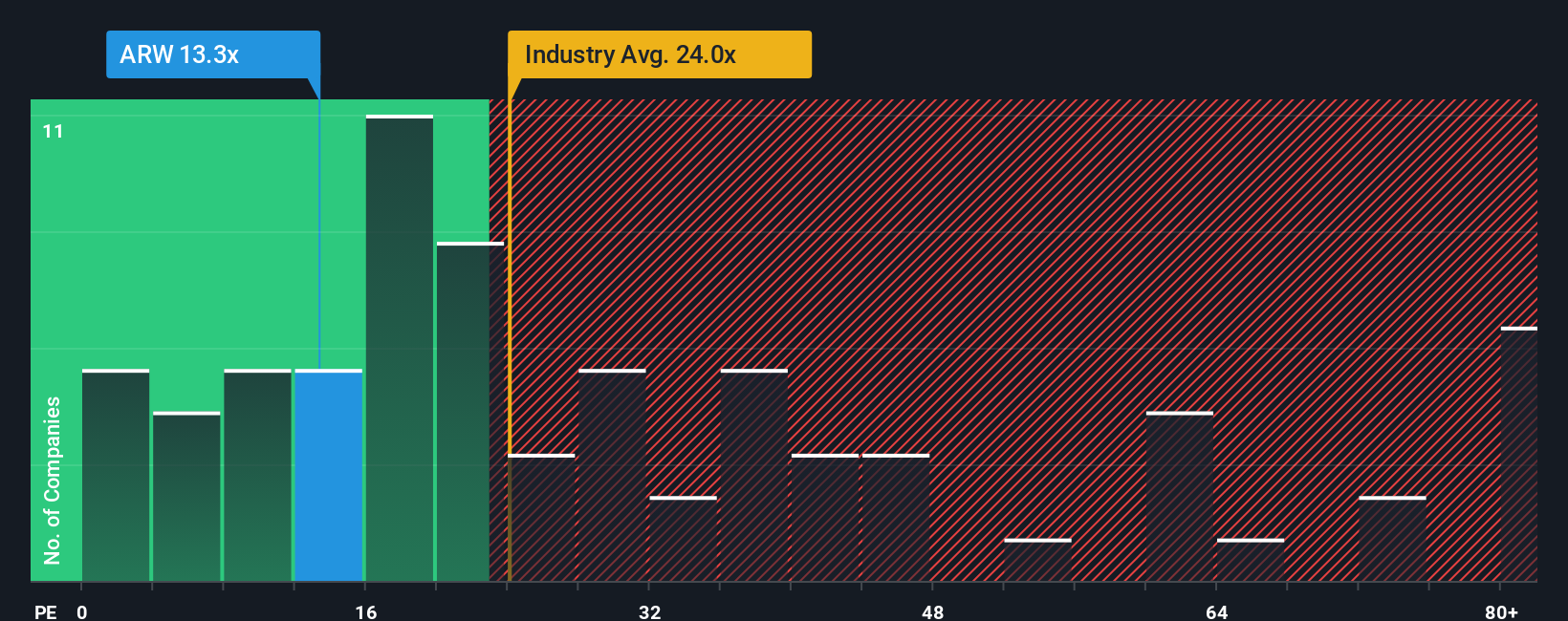

That narrative-based fair value of $108.25 paints Arrow as 23% overvalued, yet the current P/E of 14.4x looks quite different. It sits below peers at 18.9x and below a fair ratio of 17.7x. This points to less valuation risk than the headline discount suggests. Which signal appears more relevant?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Arrow Electronics Narrative

If you see Arrow’s story differently or prefer to test your own assumptions against the numbers, you can sketch out a complete narrative in minutes, starting with Do it your way.

A great starting point for your Arrow Electronics research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Arrow has your attention, do not stop here. You could miss other opportunities that fit your style even better. Use the Screener to widen your field of vision.

- Spot potential mispricings by scanning these 866 undervalued stocks based on cash flows that line up with your return expectations and risk tolerance.

- Ride major technology shifts by filtering for these 24 AI penny stocks shaping everything from automation to next generation software.

- Lock in potential portfolio income by tracking these 14 dividend stocks with yields > 3% that might suit your yield and payout preferences.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ARW

Arrow Electronics

Arrow Electronics, Inc. sources and engineers technology for manufacturers, service providers, and users of enterprise computing solutions in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on ZenaTech ·

ZenaTech: A big bet on the rise of AI drones and drones-as-a-service

Fair Value:US$6.8563.8% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$50014.6% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

FA

FA_Trader on A1 A.K. Koh Group Berhad ·

A1 A.K. Koh Group Berhad: A simple local food story that could ride on Visit Malaysia 2026

Fair Value:RM 0.3340.9% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kaladorm on American Integrity Insurance Group ·

Priced for worse weather, but undervalued even for a high hurricane season

Fair Value:US$37.1948.7% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on BridgeBio Pharma ·

BridgeBio Pharma (BBIO): The "Catalyst Symphony" and the Rare Disease Transition

Fair Value:US$89.520.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Toronto-Dominion Bank ·

TD Bank (TD): The "Remediation Rally" and the AI Compliance Guard

Fair Value:CA$1226.8% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6095.6% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9827.9% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.7% undervalued

56 followersusers have followed this narrative

3 commentsusers have commented on this narrative

30 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6432.4% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

DS

dsfaggafgafg on Micron Technology ·

This is truly one of the worst predictions of all time. Its forward PE is 3.9x.

0

|0