Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:STX

Does Seagate’s Rally Still Have Room After 153% Gain and Solid Cloud Demand in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

Thinking about what to do with Seagate Technology Holdings stock? If you’ve been watching its rollercoaster of impressive returns, you’re not alone. Whether you’re holding, eyeing a buy, or just looking for insight, it’s hard to ignore a stock that’s up 153.9% year-to-date and has climbed a staggering 403.4% over the last five years. Even with a slight dip of -2.2% in the past week, the long-term growth story here is loud and clear, especially as the data storage market keeps evolving and as demand for cloud infrastructure heats up.

But growth like this also comes with important questions: Is all the good news already baked into the price, or does Seagate still have room to surprise investors? That’s where smart valuation analysis comes in handy. When we run Seagate through our six-point undervaluation check, it ticks only two boxes, giving it a value score of 2. That suggests the market may have already caught on to much of the company’s potential. What does that score really mean in context, and which valuation signals matter most?

Let’s break down what valuation approaches can reveal about Seagate today, and why there might be an even more insightful angle to consider before making your next move.

Seagate Technology Holdings scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

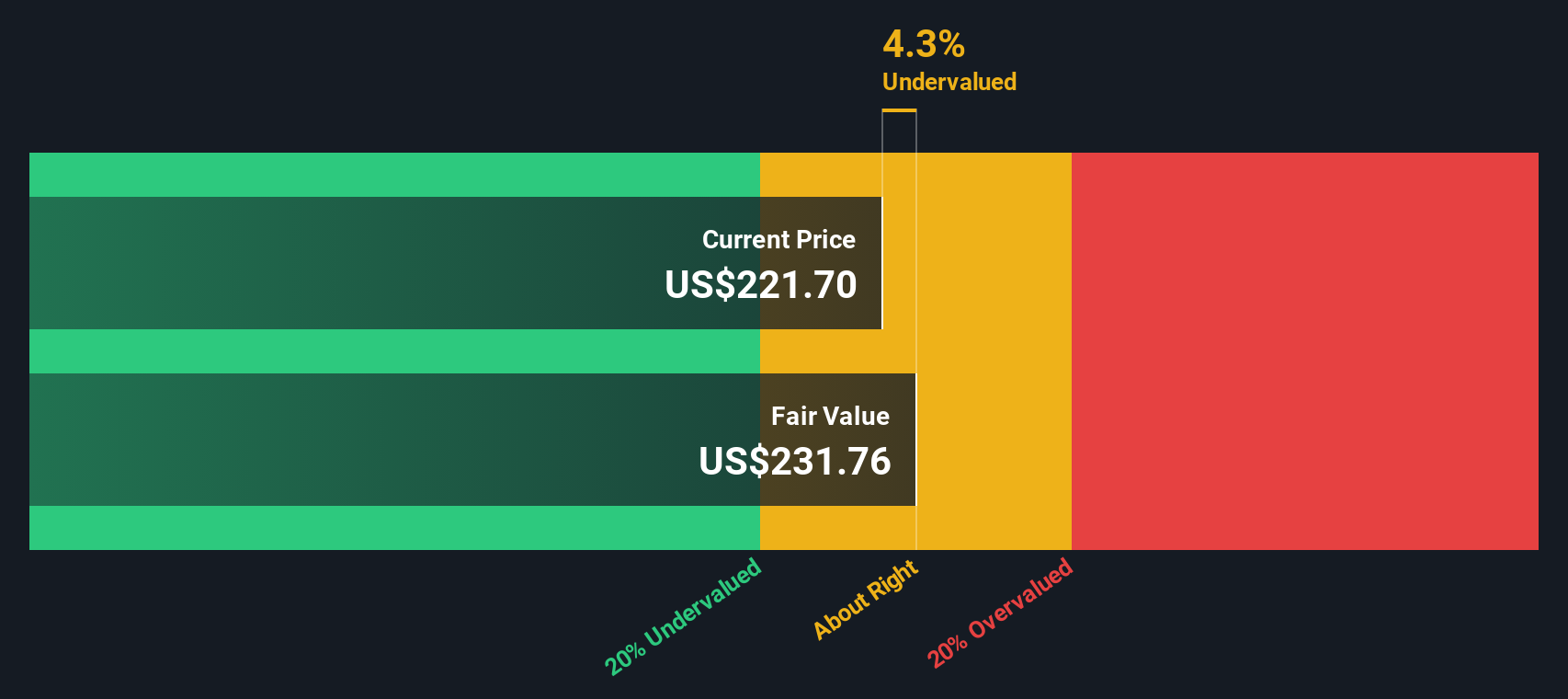

Approach 1: Seagate Technology Holdings Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) approach estimates a company’s intrinsic value by projecting its future cash flows and discounting them back to today’s dollars. This model provides a forward-looking view and helps investors judge whether a stock is trading below or above its real economic worth.

For Seagate Technology Holdings, the current Free Cash Flow (FCF) stands at $753 Million. Analyst projections see FCF growing to about $2.7 Billion by 2030, indicating expectations for substantial cash generation as demand for data storage and cloud infrastructure expands. The first five years of these forecasts are based on analyst estimates. The years that follow are extrapolated from growth trends.

Using these projections in the DCF model, the estimated fair value for Seagate stock is $230.88 per share in today’s dollars. At the moment, this calculation implies the stock is trading about 5.0% below its intrinsic value, suggesting only a modest discount compared to current prices.

Result: ABOUT RIGHT

Simply Wall St performs a valuation analysis on every stock in the world every day (check out Seagate Technology Holdings's valuation analysis). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes.

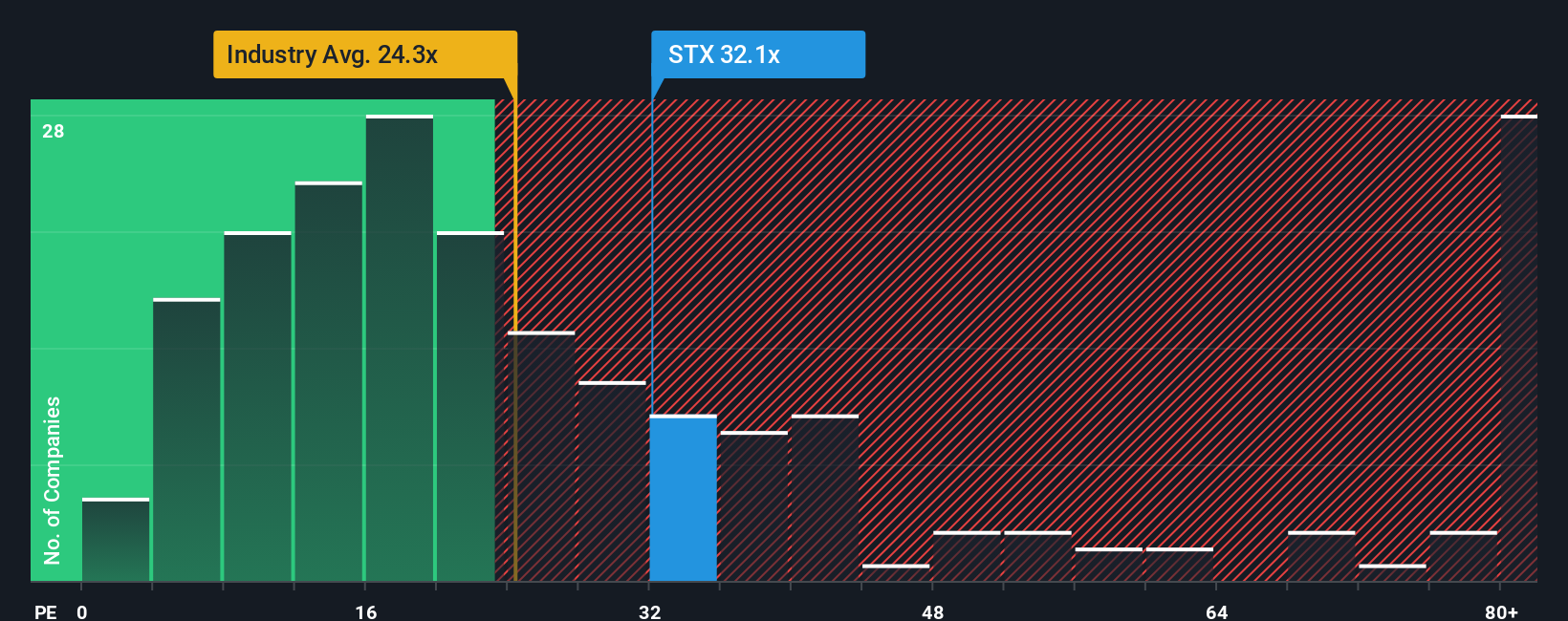

Approach 2: Seagate Technology Holdings Price vs Earnings

For established, profitable companies like Seagate Technology Holdings, the Price-to-Earnings (PE) ratio is a widely used metric because it links a company’s current share price with the profits it generates. Investors use the PE ratio to quickly compare how much they are paying for each dollar of earnings, with higher ratios often reflecting higher expectations for future growth or lower risk.

Growth prospects and risk profiles play a big part in what counts as a “fair” or “normal” PE ratio. Businesses expected to grow faster or with lower perceived risk tend to justify higher PE ratios, while slower-growing or riskier firms will typically trade at lower multiples.

Seagate Technology Holdings is currently trading at a PE ratio of 31.8x. This sits above both the peer average of 21.6x and the technology industry average of 23.6x. At first glance, this premium might suggest the stock is overvalued, but context is crucial here.

Simply Wall St’s proprietary “Fair Ratio” metric goes beyond just industry or peer comparisons. It incorporates important factors like Seagate's specific earnings growth outlook, profit margins, industry characteristics, market cap, and risk profile to calculate what a truly fair multiple should be for the business. This holistic approach can be more telling than a simple side-by-side with competitors.

For Seagate, the calculated Fair Ratio is 34.9x, just slightly higher than its actual PE ratio of 31.8x. This close alignment indicates the share price is about in line with the level you would expect given the current fundamentals and outlook.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Seagate Technology Holdings Narrative

Earlier we mentioned that there’s an even better way to understand valuation, so let’s introduce you to Narratives. Narratives are simple, powerful tools that let investors connect their personal perspective or “story” about a company, such as their beliefs about Seagate’s breakthroughs or the challenges it faces, with concrete financial forecasts for revenue, margins, and fair value.

Rather than just comparing standard ratios or targets, Narratives help you build your own investment scenario by linking what you think will drive the business to an estimate of fair value, all in one place. They make this process accessible: on Simply Wall St’s Community page, millions of investors share and update Narratives so you can easily find, follow, or even challenge real-world outlooks on Seagate.

What makes Narratives especially useful is that they update automatically, factoring in news, earnings releases, and other market-moving events, keeping your assumptions and fair value in sync with new reality. For example, some investors believe robust cloud demand and Mozaic drive adoption justify a bullish fair value above $200 per share, while others cite industry risks for a more cautious target closer to $80. Narratives give you the context and dynamic tools to make smarter, more confident decisions about when to buy or sell, based not just on numbers but on the story you believe.

Do you think there's more to the story for Seagate Technology Holdings? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:STX

Seagate Technology Holdings

Engages in the provision of data storage technology and infrastructure solutions in Singapore, the United States, the Netherlands, and internationally.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor