Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:SMCI

Super Micro Computer (SMCI) Stock After 28% Weekly Drop Is The Rally Running Out Of Steam

Reviewed by Bailey Pemberton

- If you are wondering whether Super Micro Computer stock still offers value after its big run in recent years, the next sections will break down what the current price might be implying.

- The stock recently closed at US$29.22 and has declined 28.1% over the past week, 5.9% over the past month and 5.6% year to date, while still sitting far above its level from three years ago.

- These moves come as investors continue to reassess Super Micro Computer's role in AI related infrastructure and high performance computing, with sentiment shifting quickly as expectations adjust. Coverage has increasingly focused on how much future demand is already reflected in the share price and whether recent volatility points to changing risk perceptions.

- On Simply Wall St's valuation checks, Super Micro Computer currently has a valuation score of 4 out of 6. This sets up a closer look at P/E, DCF and other methods, followed by a broader way to think about what valuation really means for long term investors.

Find out why Super Micro Computer's -32.2% return over the last year is lagging behind its peers.

Approach 1: Super Micro Computer Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what Super Micro Computer stock might be worth today by projecting future cash flows and then discounting them back to a present value using a required rate of return.

For Super Micro Computer, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is a loss of about $6,890.9 million, and analysts plus extrapolations project free cash flow moving to $980.1 million by 2029, with further estimates out to 2035. Simply Wall St uses analyst forecasts up to 2029, then extends the trend to build a 10 year cash flow path.

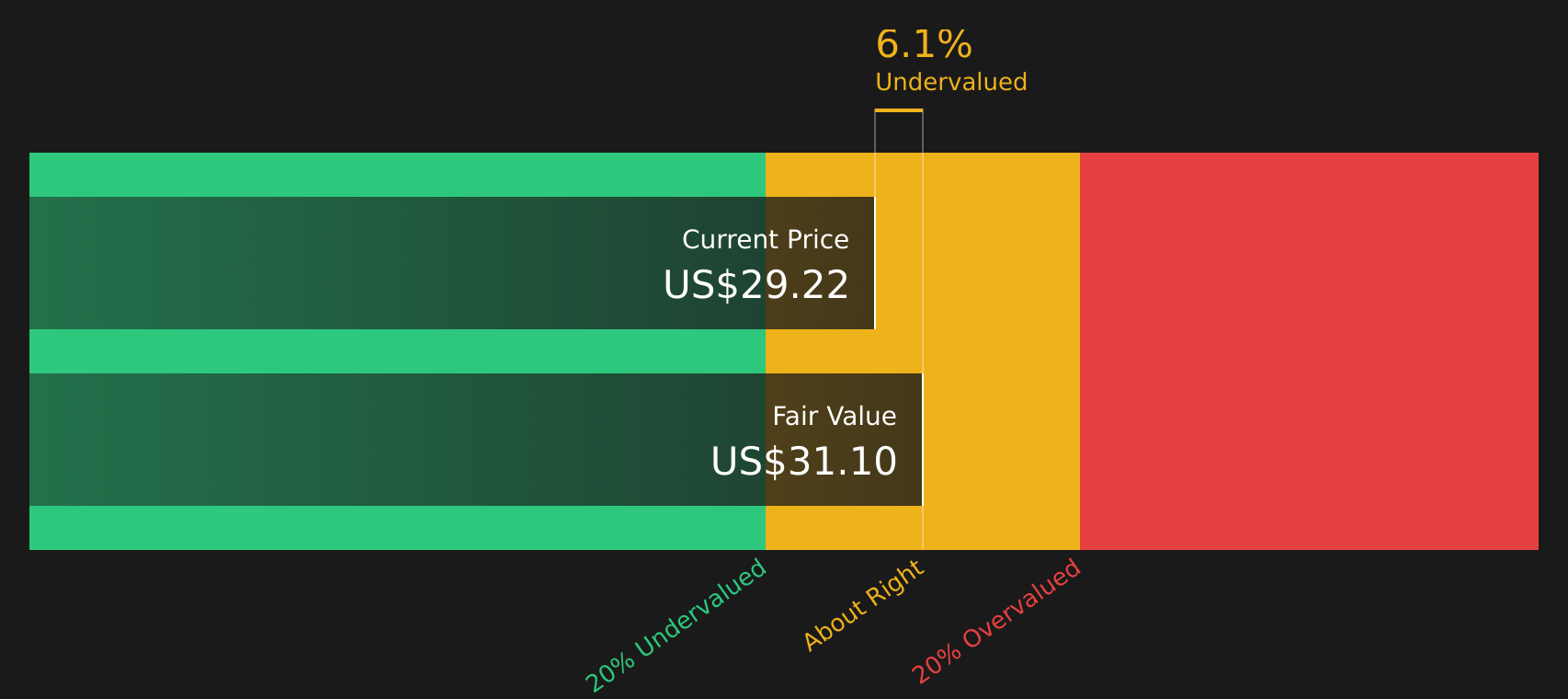

On this basis, the DCF model arrives at an estimated intrinsic value of about $31.10 per share, compared with the recent share price of $29.22. That implies Super Micro Computer is trading at roughly a 6.1% discount to this cash flow based estimate. This is a relatively small gap and could easily move either way as assumptions change.

Result: ABOUT RIGHT

Super Micro Computer is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Super Micro Computer Price vs Earnings

For a profitable company like Super Micro Computer, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings. A higher or lower P/E often reflects how the market weighs growth expectations and risk, with faster growth and lower perceived risk usually supporting a higher ratio.

Super Micro Computer currently trades on a P/E of 15.15x. This sits below the Tech industry average of 24.17x and also below the peer group average of 52.23x. On the surface, that might suggest the stock is priced more conservatively than many listed peers.

Simply Wall St’s Fair Ratio framework goes a step further. It estimates what a more tailored P/E could look like, given factors such as earnings growth, industry, profit margins, market cap and company specific risks. This is designed to be more informative than a simple comparison with broad industry or peer averages. For Super Micro Computer, the Fair Ratio is 54.18x, which is materially higher than the current 15.15x P/E. On these inputs, the stock screens as trading below this model based estimate.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Super Micro Computer Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives on Simply Wall St take the story you believe about Super Micro Computer, link it directly to a financial forecast, then translate that into a fair value you can compare to the current price.

In practice, a Narrative lets you set assumptions for future revenue, earnings and margins. This way your view of the company is tied to concrete numbers rather than a vague opinion, and the platform then shows whether your implied fair value suggests the stock looks expensive or cheap relative to where it trades today.

These Narratives live in the Community page on Simply Wall St, are used by millions of investors, and update automatically when new data, news or earnings are added. This means your story and the resulting fair value move as fresh information comes through.

For Super Micro Computer, one investor might build a cautious Narrative around legal risk and margin pressure that leads to a fair value near US$16 per share. Another might focus on AI infrastructure demand and higher long term revenue forecasts that point to a fair value closer to US$58. Comparing those figures with the current price can help each investor decide whether the stock fits their own risk and return expectations.

For Super Micro Computer, however, we will make it really easy for you with previews of two leading Super Micro Computer Narratives:

Each one ties a clear story about the business to a fair value, so you can quickly see which assumptions line up more closely with your own view before building a narrative yourself.

🐂 Super Micro Computer Bull Case

Fair value: US$33.20

Implied undervaluation vs last close: about 12.0% below this narrative fair value

Revenue growth assumption: 28.0%

- Frames Super Micro Computer as a beneficiary of growing AI and analytics infrastructure spending, with modular data center solutions supporting revenue expansion and higher margin potential.

- Highlights product mix, global manufacturing footprint, and broader customer base as tools that could support margin recovery and reduce reliance on a few large buyers over time.

- Balances this with clear risks around customer concentration, hardware price competition, longer purchasing cycles, platform adoption, and global supply chain and trade exposure.

🐻 Super Micro Computer Bear Case

Fair value: US$24.50

Implied overvaluation vs last close: about 19.3% above this narrative fair value

Revenue growth assumption: 5.67%

- Accepts that Super Micro Computer has reported rapid AI related revenue growth, but focuses on how lower gross margins and reliance on one very large customer leave the earnings base exposed.

- Places legal and governance issues at the center of the thesis, with Department of Justice related risks and customer dependence used to justify a lower multiple and wide valuation range.

- Describes Super Micro Computer stock as a high risk, event driven situation where outcomes hinge on how legal matters evolve and whether the company can improve profitability while maintaining demand.

If you want to see how other investors are joining these dots around growth, margins, legal risk, and valuation for Super Micro Computer, it can be useful to read the full range of narratives and then test which set of assumptions you find more reasonable.See what the community is saying about Super Micro Computer

Do you think there's more to the story for Super Micro Computer? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SMCI

Super Micro Computer

Develops and sells server and storage solutions based on modular and open-standard architecture in the United States, Asia, Europe, and internationally.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3450.6% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.3% overvalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.651.0% undervalued

13 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£163.7% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

SI

Silvester on Medtronic ·

Strong in favor of diversity in value portfolio

Fair Value:US$90.3710.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DI

Didier_Lambert_private_inv on Novo Nordisk ·

Relatively mispriced taken into account its intrinsic growth profile, providing a defensive, cash-generative entry point for investors

Fair Value:DKK 35019.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GO

GoranLagea on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d. future looks bright with a profit margin change of 38%

Fair Value:€36035.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.2% undervalued

56 followersusers have followed this narrative

8 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.3% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

AC

ACV on Alignment Healthcare ·

high medical loss ratios, and negative free cash flow signal that scaling profitably remains elusive...

0

|0