Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:RELL

Do Richardson Electronics’ (RELL) Earnings Beat and Dividend Signal Enduring Profit Growth?

Reviewed by Sasha Jovanovic

- Richardson Electronics reported its first quarter 2026 results on October 8, 2025, posting sales of US$54.61 million and net income of US$1.91 million, both higher than the same period last year, and reaffirmed its quarterly dividend of US$0.06 per common share and US$0.054 per Class B share.

- These results reflect both revenue and earnings growth paired with continued shareholder returns, highlighting stronger profitability and an ongoing commitment to dividends.

- With the earnings growth outpacing last year's results, we'll examine how this improved financial performance may influence Richardson Electronics' investment narrative.

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Richardson Electronics Investment Narrative Recap

To own shares of Richardson Electronics, an investor needs to believe in the company’s ability to transition from its legacy component businesses toward faster-growing energy and automation markets. While the latest earnings release showed solid revenue and net income growth, the impact on overcoming the biggest short-term risk, quarterly volatility tied to the project-based Green Energy Solutions segment, remains limited, and the company’s exposure to mature markets is still a consideration for the investment case.

Among recent announcements, the ongoing affirmation of Richardson Electronics’ quarterly dividend stands out. Continued dividend payments, even through volatile periods, signal management’s confidence in underlying cash flows, which may appeal to income-focused investors and support sentiment as the company navigates growth initiatives and unpredictable project timelines.

Yet, despite robust short-term performance, investors should also weigh the potential downside if the company’s reliance on project-based revenues means another quarter of...

Read the full narrative on Richardson Electronics (it's free!)

Richardson Electronics' outlook anticipates $265.0 million in revenue and $16.7 million in earnings by 2028. This scenario assumes an annual revenue growth rate of 8.2% and a $17.8 million increase in earnings from the current $-1.1 million.

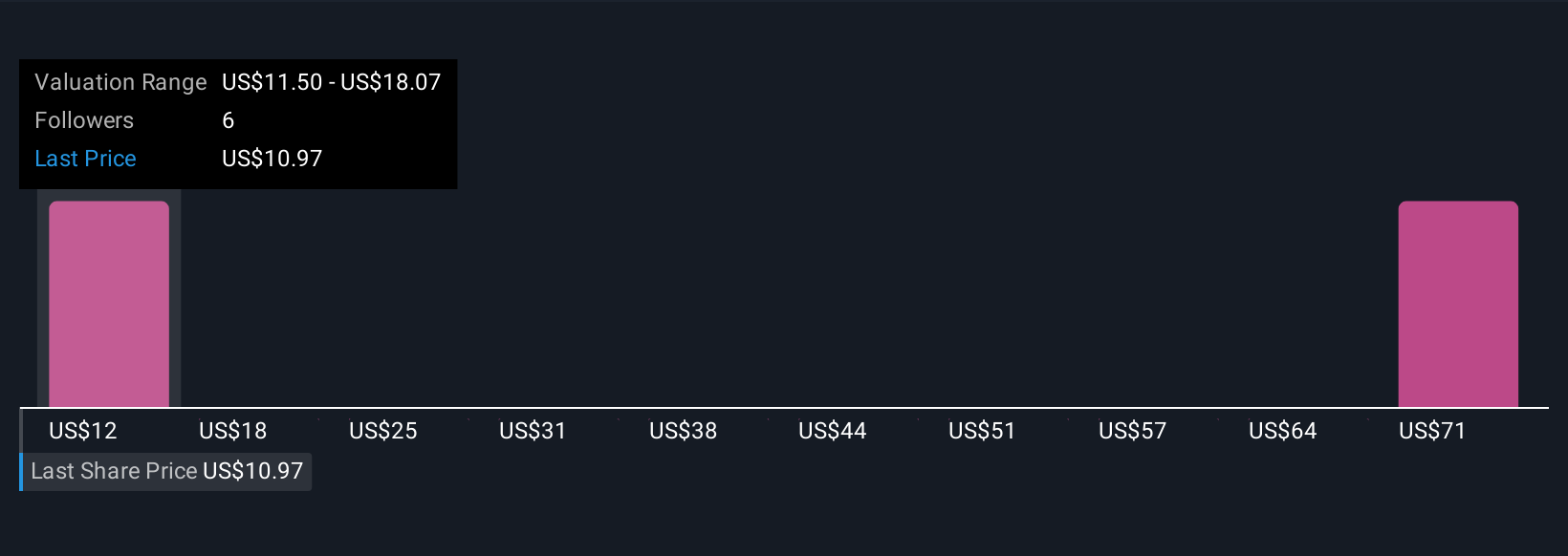

Uncover how Richardson Electronics' forecasts yield a $11.50 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community fair value estimates for Richardson Electronics span from US$11.50 to US$77.82, with just two individual perspectives shaping this wide range. As you consider these differing views, keep in mind that ongoing volatility in project-based revenue may influence how the company performs relative to both market expectations and peer groups.

Explore 2 other fair value estimates on Richardson Electronics - why the stock might be worth just $11.50!

Build Your Own Richardson Electronics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Richardson Electronics research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Richardson Electronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Richardson Electronics' overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:RELL

Richardson Electronics

Provides engineered solutions, power grid and microwave tube, and related consumables in North America, the Asia Pacific, Europe, and Latin America.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2554.7% undervalued

110 followersusers have followed this narrative

0 commentsusers have commented on this narrative

24 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4859.0% undervalued

213 followersusers have followed this narrative

8 commentsusers have commented on this narrative

32 likesusers have liked this narrative

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43047.7% undervalued

20 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9953.6% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

TH

TheGrayWolf_80 on Schwab Strategic Trust - Schwab U.S. Dividend Equity ETF ·

Building a 75/15/10 Income Machine with Schwab's Dividend ETF

Fair Value:US$63.7546.9% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SI

simplydunno on Microsoft ·

Microsoft's Capex Bill Comes Due Before the AI Revenue Does

Fair Value:US$512.123.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HE

Henrynuke03 on Nigerian Exchange Group ·

Future Growth Awaits NGXGROUP with New High-Profile Listings

Fair Value:₦221.1732.3% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28032.1% undervalued

211 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.917.0% undervalued

97 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6510.2% undervalued

74 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

BL

Blegells on Terra Balcanica Resources ·

⏫42X THE AVERAGE DAILY TRADING VOLUME TODAY, JULY 28 🐂🐂🐂 FORTY-TWO!

1

|0

DE

derek_3wsdg on Teladoc Health ·

You’ve overlooked the activist investor factor. Travis Cocke’s Voss has announced 5% ownership through a 13G filing. They’ve added to that 5% since, and in doing so, have created a structural trap door for 27.42 Million Shares actively sold short. Chuck will announce lots of positives on July 29 but it’s what Voss announces shortly after that will rock the overextended Teledoc shorts. The Walmart partnership is the tip of the iceberg. The market is missing the sheer regulatory and enterprise friction of modern corporate healthcare. Teladoc isn't a "consumer app"; it is the primary digital infrastructure integrated directly into the legacy backends of Tier-1 insurance companies and fortune 500 employers, covering 105 million+ lives. Teladoc is acting as the digital top-of-funnel engine for the world's largest retailer. If Voss pushes the narrative that Teladoc is effectively the outsourced digital brain of Walmart's entire healthcare footprint, the fair value shifts from a basic health multiple to an enterprise distribution premium. Additionally , we are in a structural gold rush for high-quality, legally compliant, longitudinal medical data to train vertical healthcare AI models. Large technology hyperscalers and pharmaceutical giants cannot simply scrape the internet for this; they need structured clinical inputs. Teladoc sits on one of the largest de-identified virtual medical datasets on earth. From the activist playbook , we’ll see Voss demand the immediate creation of a Data & Diagnostics Licensing Division, transforming a legacy liability into an incredibly high-margin, pure-software data asset that requires zero human clinician hours to scale. Chuck is doing great work and deserves credi5 for the Teledoc turnaround but it will be Travis Cocke who will be responsible for a share price way beyond your $15 valuation.

1

|0