Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:PLUS

Will Weakening IT Demand And Falling Sales Projections Change ePlus' (PLUS) Growth Narrative?

Reviewed by Sasha Jovanovic

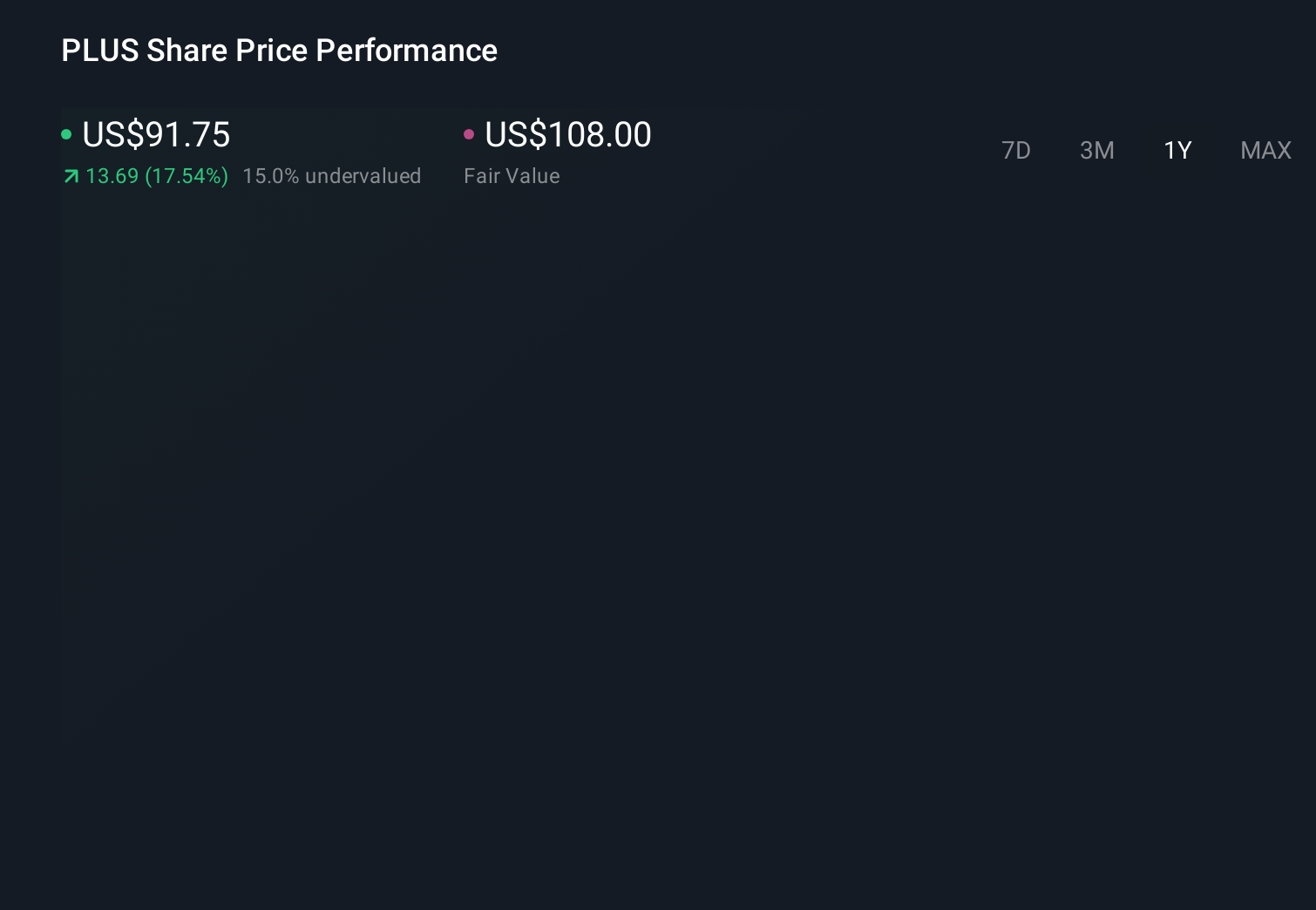

- Recently, commentary around ePlus (NASDAQ:PLUS) highlighted that its sales have been flat for the past two years and are projected to fall over the next 12 months as demand for its IT solutions fades.

- This shift in demand expectations raises questions about the durability of ePlus’s business model and its ability to sustain prior operating trends.

- We’ll now explore how weakening demand and expectations for declining sales could reshape ePlus’s existing investment narrative.

These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

ePlus Investment Narrative Recap

To own ePlus, you need to believe it can convert its IT solutions expertise into durable, recurring revenue despite lumpier project demand. The latest commentary on flat sales and expected declines makes the near term revenue trend a more pressing risk than before, but it does not directly change the main positive catalyst, which is the company’s positioning in AI, security and cloud infrastructure where demand remains an important swing factor.

The recent initiation and affirmation of a quarterly US$0.25 dividend, alongside ongoing share repurchases, is the announcement that sits closest to this debate, because it highlights management’s current confidence in cash generation at a time when some forecasts are turning more cautious on sales. These capital returns may appeal to investors, but they also sharpen the question of how resilient earnings will be if demand for large projects weakens further.

Yet behind these reassuring capital returns, one specific risk around revenue concentration is something investors should be aware of...

Read the full narrative on ePlus (it's free!)

ePlus’ narrative projects $2.2 billion revenue and $78.4 million earnings by 2028. This implies a 0.2% yearly revenue decline and a $32.5 million earnings decrease from $110.9 million today.

Uncover how ePlus' forecasts yield a $108.00 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span a wide range from about US$37 to US$108, underscoring how far apart individual views can be. When you set that against concerns about flat to declining sales and potential revenue volatility, it becomes even more important to compare several perspectives on what might drive ePlus’s performance over the next few years.

Explore 2 other fair value estimates on ePlus - why the stock might be worth less than half the current price!

Build Your Own ePlus Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ePlus research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ePlus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ePlus' overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PLUS

ePlus

Provides information technology (IT) solutions that enable organizations to optimize IT environment and supply chain processes in the United States and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

121 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

SE

SeanTho on lululemon athletica ·

China Is Growing 46%, The Stock Is Down 47%. Growth and Value Outside the US Market.

Fair Value:US$26540.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

max_profit on Indegene ·

Indegene deep undervalued stock

Fair Value:₹808.9446.9% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on VEON ·

VEON Ltd. (VEON): The Frontier "Digital Operator" and the 84% Hypergrowth Inflection

Fair Value:US$67.825.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1310 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0