Advertisement

- United States

- /

- Communications

- /

- NasdaqGS:NTCT

Is NetScout Systems (NASDAQ:NTCT) Using Too Much Debt?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that NetScout Systems, Inc. (NASDAQ:NTCT) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for NetScout Systems

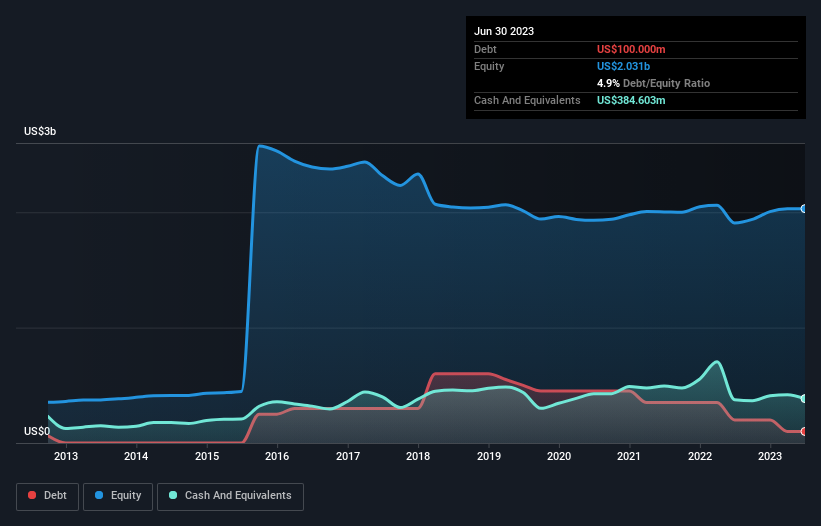

What Is NetScout Systems's Debt?

As you can see below, NetScout Systems had US$100.0m of debt at June 2023, down from US$200.0m a year prior. But on the other hand it also has US$384.6m in cash, leading to a US$284.6m net cash position.

How Strong Is NetScout Systems' Balance Sheet?

According to the last reported balance sheet, NetScout Systems had liabilities of US$383.2m due within 12 months, and liabilities of US$316.2m due beyond 12 months. Offsetting these obligations, it had cash of US$384.6m as well as receivables valued at US$108.3m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$206.5m.

Given NetScout Systems has a market capitalization of US$2.04b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, NetScout Systems boasts net cash, so it's fair to say it does not have a heavy debt load!

In addition to that, we're happy to report that NetScout Systems has boosted its EBIT by 56%, thus reducing the spectre of future debt repayments. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine NetScout Systems's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While NetScout Systems has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, NetScout Systems actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

Although NetScout Systems's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$284.6m. And it impressed us with free cash flow of US$146m, being 321% of its EBIT. So we don't think NetScout Systems's use of debt is risky. Over time, share prices tend to follow earnings per share, so if you're interested in NetScout Systems, you may well want to click here to check an interactive graph of its earnings per share history.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if NetScout Systems might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:NTCT

NetScout Systems

Provides service assurance and cybersecurity solutions to protect digital business services against disruptions in the United States, Europe, Asia, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on Myseum ·

The Future of Social Sharing Is Private and People Are Ready

Fair Value:US$7.9577.1% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on ASML Holding ·

EU#3 - From Philips Management Buyout to Europe’s Biggest Company

Fair Value:€1.31k7.1% undervalued

26 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

YI

yiannisz on Booking Holdings ·

Booking Holdings: Why Ground-Level Travel Trends Still Favor the Platform Giants

Fair Value:US$5.47k8.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CO

composite32 on Shell ·

A fully integrated LNG business seems to be ignored by the market.

Fair Value:UK£36.122.6% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

BL

BlackGoat on Palantir Technologies ·

Palantir: Redefining Enterprise Software for the AI Era

Fair Value:US$107.0237.0% overvalued

194 followersusers have followed this narrative

6 commentsusers have commented on this narrative

1 likeusers have liked this narrative

AN

andre_santos on Microsoft ·

Microsoft - A Fundamental and Historical Valuation

Fair Value:US$437.171.6% undervalued

17 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

UN

unknown on Merck ·

The Oncology Anchor: Why Merck’s 46% Discount Defies the Keytruda Cliff

Fair Value:US$201.5645.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3324.4% undervalued

71 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0224.5% undervalued

1047 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Amazon.com ·

AMZN: Acceleration In Cloud And AI Will Drive Margin Expansion Ahead

Fair Value:US$295.6119.1% undervalued

1342 followersusers have followed this narrative

5 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

JA

jayhcee on Motorcar Parts of America ·

MPAA often has inventory and core-related timing issues. While this quarter’s problems may ease, similar issues have recurred historically and can persist for several quarters. It's not a one-off, it's a structural part of their business. Core returns are simply estimates: How many customers will actually return the original part; how quickly they'll do so; how many are useable; what they're worth, etc. MPAA predicts X sales in a quarter and Y core returns and its reserves, inventory values, etc. are based on that. If they expect a 90% core return rate and only 80% come back it doesn't change cash but they have to write down inventory and increase cost of goods sold which impacts EPS. They've also cited inventory buildup at key customers multiple times in the past. The assumption the latest backlog will all shift into future quarters this year with no impact on pricing, etc. seems more like wishful thinking. Retailer X was slated to buy $10m in parts this quarter but finds they have a lot more inventory on hand than they anticipated so they pushed the order. Realistically there are likely to be SKU cuts, reduction in safety stock on others, etc. Assuming that all $10m will come in this year plus the regular replenishment seems pretty unrealistic. MPAA also has a shaky track record when it comes to new lines and the supposed impact on business. If you look at the EV testing solutions hype back around 2020 that was supposed to diversify them beyond traditional reman and be a higher margin business that would grow with EV adoption. But it has never turned into a material contributor. The debt reduction and stock buy backs are meaningful but IMHO this narrative takes a very optimistic view of things.

0

|0

US

User on Discovery Silver ·

The problem with your reasoning is, that 37 Moz are AgEq. If you read the FS, you'll find out that annual silver production is more around 14-15 Moz. But at the time of the FS, that 37 Moz AgEq was a number that came of a formula (which is specified in the FS), being a mix of four metals: Ag, Au, Pb and Zc. But now, beginning of 2026, the spotprices of silver and gold have risen so much in comparison to Pb and Zc prices, that you need to recalculate the AgEq number of 37 Moz according to the recent prices. This will result in the fact that silver and gold hold more value in that mix of four metals, and thus dragg the 37 Moz AgEQ number down to somewhere around 18 Moz AgEq. The more valuable silver and gold become, the lower the AgEq number will get, but it'll never get under the yearly average production of silver, which should be somewhere between 14-15 Moz Ag in the first four years. So in short, with this in mind, your fair value is rather around CA$ 50, even with silver at 300 usd an ounce. But a more prudent stockprice forecast is around CA$ 20 and hopefully going toward CA$ 30. So DSV is a top stock, because it's producing actual gold every quarter. But don't put your hopes too high.

0

|0